On The Line With BlueVine After a Big Year

March 13, 2017 Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

BlueVine’s success comes at a time when some in the online lending space have lost their luster. Lifshitz feels his company, however, is positioned well. “The time of exuberance has disappeared,” Lifshitz says. “Investors are looking to create value.”

Part of what makes them different is that they not only factor invoices, but they also provide lines of credit to prime and near-prime customers. Factoring is still a bigger percentage of their overall business, Lifshitz says, but he asserts that their credit line segment is growing at a faster clip. And he insists that they are working on other products too, not just loans. It sounds like the beginnings of a bank, I tell him, while making references to SoFi and their ability to live on the threshold of banking without actually currently being one.

“People have been saying that PayPal would become a bank forever but they haven’t become one,” he points out.

Still, running a company as big as his does require prudent decisions. “We are very mindful of how we manage capital,” he says. I ask if he thinks his business model protects them from an economic downturn. “It doesn’t protect it,” he asserts. Instead, he explains, his model gives him the ability to make adjustments rapidly. Since BlueVine’s capital is typically repaid in a matter of months, they can react to economic changes quickly.

Big name backers aren’t afraid to show that they believe in this either since they have been funded by Lightspeed Venture Partners, 83NORTH, Correlation Ventures, Menlo Ventures, Rakuten Fintech Fund and other private investors. A recent announcement by BlueVine says that they are on track to fund approximately $500 million to small businesses in 2017.

In Canada, Alternative Business Finance Industry Similar, Yet Different

March 8, 2017 David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

“We don’t view ourselves as directly competing with banks,” Gens says, suggesting that his target market is less than prime. It’s a point that his counterparts in the US have made often. But there’s a slight difference with that approach in their market, he adds. “Most Canadian consumers are prime.” And unlike the US, the banks are not necessarily portrayed as the enemy in Canada where five major ones dominate the market.

“It’s exceptionally difficult for an alternative small business lender to build a brand,” said Jeff Mitelman, CEO of Montreal-based Thinking Capital, on a panel at the LendIt Conference. Despite that, his company has funded half a billion dollars to 15,000 unique businesses over the last 10 years. A panelist besides him half-joked however, that there is such an inherent conservatism with Canadian small business owners that some don’t even want to grow and are content with running lifestyle businesses.

But of the deals that are getting done, they’re often acquired through direct marketing. “The ISO market is not like it is in the US,” Gens says. “There’s just a handful of them.” Where there are ISOs though, competitive pressures usually follow. He says that they’re competing on at least 50% of the deals they work on, in part because of these ISOs. Stacking is happening in Canada too, he admits. “It’s not as crazy as it is in the states,” he contends. “Philosophically, it doesn’t align with our business.”

Some deals in Canada are actually being facilitated by US ISOs, he acknowledges, before clarifying that they should be aware that they will get paid in Canadian dollars, which at present are worth about a three quarters of an American dollar. They are in a different country after all.

Gens and others like Bruce Marshall, vice president of British Columbia-based Company Capital, agree that OnDeck’s push into Canada has been good for the entire industry. Six months ago, Marshall said, “We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising. These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails.”

Over time, they believe alternatives will become more mainstream. For Gens, part of that is about doing right by the customer. “We pride ourselves on being very transparent,” he says. There are no hidden fees with their products and they can make things easy like use APIs to access a merchant’s bank statement history, provided an applicant wants to do it that way. “More than 50% of merchants are still submitting bank statements,” he says. That trend is still pretty much true in the US as well. “There’s a much lower incidence of fraud in Canada,” he asserts. It’s a nation of small businesses he’s content to serve.

How Banks Are Coming Back to SME Lending (Summary)

March 6, 2017

The banks are no longer sitting on the sidelines of small business lending. At LendIt on Monday, a panel featuring representatives from two of the biggest banks in the country, reminded young upstarts that they intended to be the primary capital sources for small businesses.

Unlike JPMorgan Chase, which partnered with OnDeck, Bank of America (BoA) decided to build the technology to deliver loans easily and quickly on their own. BoA SVP Nadeem Tufail said that reputational risk had held them back from partnering with a platform back when they were considering it years ago. “We couldn’t make that leap,” he explained, citing factors like cost, which they saw as simply being too high on some platforms to feel comfortable with.

But that doesn’t mean that the opportunity has passed them by. “A Bank of America customer can get funded in 48 hours,” Tufail proclaimed, while adding that a business that doesn’t bank with them can get a loan from them in about 7 days. The bank is also now doing fully automated approvals on a very small scale with a sliver of their best clientele to test the concept.

Meanwhile, Julie Chen Kimmerling, Senior Manager at Chase, made it a point to say that they were also really worried about things like reputational risk but that they found OnDeck to be a perfect fit. The maturity of their management team and platform really impressed them, she said. Still, Chase governs how the loans are underwritten and keeps the customers on their balance sheet. So they haven’t exactly handed the keys over to OnDeck but obviously trust their brand to be affiliated.

BoA recognized that some of their customers were telling them that they shouldn’t have to submit all these documents when the bank should already have access to their financial histories, particularly their cash flow. Tufail said that this was one of the most important factors in their underwriting. “Does the business have cash flow?” he said. “Does the business have liquidity?” The bank should already be able to evaluate these metrics.

“We certainly have an advantage with transactional level data,” Chase’s Kimmerling said of banks doing loan underwriting. And Chase is no amateur in this market. Kimmerling said that her bank had provided $24 billion of credit to US small businesses last year alone, a figure prominently displayed in their last earnings report.

To boot, both banks retain brick & mortar presences around the country, an advantage for small business customers, who they say are pretty likely to visit a branch.

The banks it seems are coming back. Lendio CEO Brock Blake moderated the panel.

Quotes and paraphrases were derived from the panel. The summary is my own analysis of it.

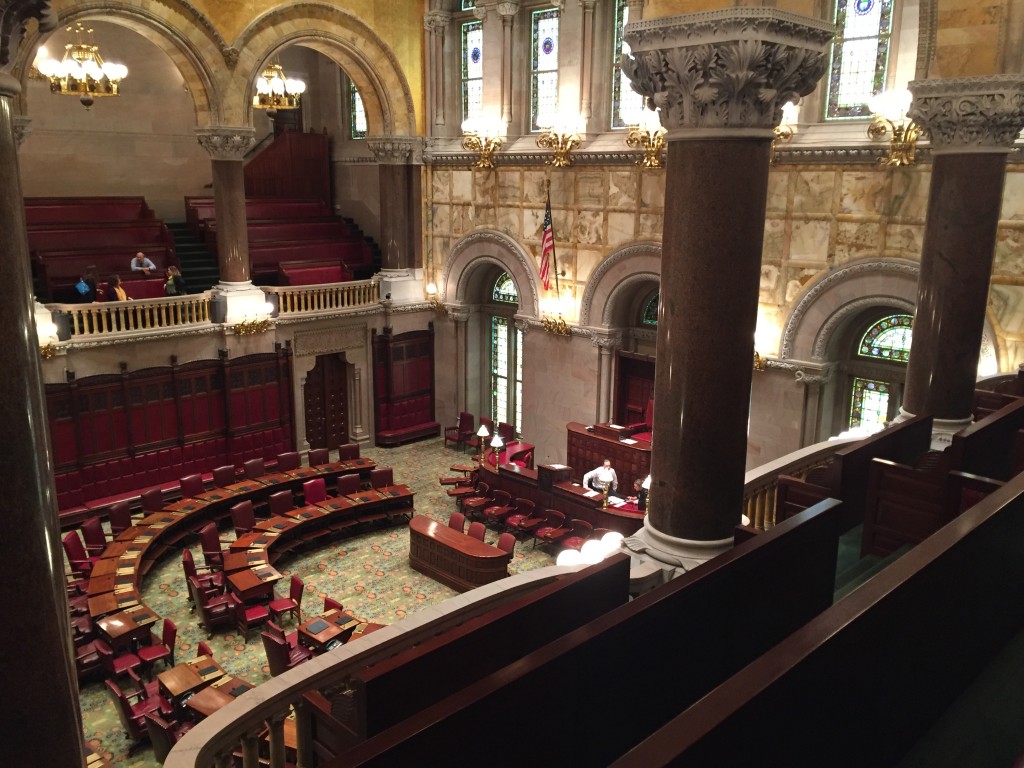

With Clock Ticking, Members of the Commercial Finance Coalition Journeyed to the New York State Capitol

March 5, 2017 With less than a month to go until New York State’s budget deadline, members of the Commercial Finance Coalition (CFC) traveled to Albany, NY last week to address a vague and confusing licensure proposal put forth by Governor Cuomo. According to the CFC, nobody from the New York Department of Financial Services, the governor’s office or the state legislature had contacted any of their members prior to putting the language in the budget that they suspect could lead to catastrophic consequences. So on very short notice, they packed their bags and went up to Albany to tell their story to as many legislators as they could.

With less than a month to go until New York State’s budget deadline, members of the Commercial Finance Coalition (CFC) traveled to Albany, NY last week to address a vague and confusing licensure proposal put forth by Governor Cuomo. According to the CFC, nobody from the New York Department of Financial Services, the governor’s office or the state legislature had contacted any of their members prior to putting the language in the budget that they suspect could lead to catastrophic consequences. So on very short notice, they packed their bags and went up to Albany to tell their story to as many legislators as they could.

“It could destroy the industry if the worst comes to fruition,” declared Robert Cook, a partner at Hudson Cook LLP, who was speaking in reference to the proposal. The industry not only employs thousands of people in New York State but also provides much-needed capital to small businesses there. The CFC says that their members injected more than $50 million into New York businesses just last year alone.

Several law firms who have written about the proposal have used words like could, may and likely to explain what will happen, in part because it seems as though no one’s really sure. CFC members worry that the proper research hasn’t been done, especially when there hasn’t been any engagement with them. “They should allow all the stakeholders to have their voices heard,” said Dan Gans, CFC’s executive director.

As the clock ticked down, the CFC’s two-day effort in the capitol building played out like a scene from a movie.

Are you aware of Part EE of the TED Bill?

This is what we do…

No, nobody from the Department of Financial Services has even talked to us

No, we’re not kidding

And on it went…

Gans says the CFC is looking for additional companies in the small business financing industry to support their efforts. He’ll be at the LendIt Conference. “I would be happy to meet with anyone interested in joining the CFC and helping us fight this misguided policy that is also attending,” he said. He can be contacted at dgans@polariswdc.com.

The budget deadline in New York State is March 31st.

Catching Up With Marketplace Lending – A Timeline

February 20, 2017This is the expanded update to the timeline of events taking place in the industry.

12/16 Chicago-based Argon Credit filed for bankruptcy

12/20 Bizfi announced that it had surpassed $2 billion in originations since inception

1/4 Strategic Funding integrated US operations of Capify

1/9 Two US Senators protested the OCC’s plans to create a limited fintech charter

1/11 Funding Circle announced a new $100 million equity round led by Accel

1/12 Marketplace Lending Association announced 11 new members

1/16

- The WSJ broke a story revealing that CAN Capital had breached its covenants with its big-bank creditors, laid off about 250 staffers, hired a restructuring firm for assistance in negotiating with creditors, and hired Jefferies Group for advice on strategic alternatives

- NY proposed broad changes to its lender licensing laws

1/17

- OnDeck announced a partnership with Wex, a provider of corporate and small business payment solutions

- New York Department of Financial Services protested the OCC’s plans to create a limited fintech charter

1/18 Credible raised $10 million in a Series B round from investors that included Ron Suber, the president of Prosper Marketplace.

1/19

- LendIt announced finalists of its first ever industry awards

- Sean Murray of AltFinanceDaily selected as a finalist for Best Journalist Coverage

1/20

- Fifth Third announced a partnership with QED Investors to advance fintech strategy

- President Trump issued an executive order freezing all new regulations

1/25 loanDepot surpassed $100 billion in loans

1/26 LendingRobot launched a marketplace lending hedge fund

1/30 Prosper Marketplace’s EVP of capital markets, Eric Thaller, departed from the company

2/1 Prosper Marketplace appointed new CFO, Usama Ashraf

2/4 OnDeck announced departure of COO James Hobson

2/8

- Breakout Capital announced a $25 million credit facility

- Lendio announced that it had facilitated $240 million in funding last year

2/13 OnDeck announced a partnership with payroll company Wave

2/14 Lending Club reported a $146 million loss for the year and an increase in bank funding

2/16

- OnDeck reported a $86 million loss for the year, layoffs

- The DC circuit decided to rehear the PHH v CFPB case

AltFinanceDaily Begins 2017 With Thickest Magazine Issue Ever

February 8, 2017 Forty-eight pages. That’s how thick AltFinanceDaily’s January/February 2017 edition is. As the wider industry heads to the LendIt Conference in NYC next month, we decided it was only fitting to feature the city that never sleeps on the cover.

Forty-eight pages. That’s how thick AltFinanceDaily’s January/February 2017 edition is. As the wider industry heads to the LendIt Conference in NYC next month, we decided it was only fitting to feature the city that never sleeps on the cover.

This issue delves into Equity crowdfunding, the story behind the LendIt Conference, and what it’s like to actually be a merchant getting a business loan from one of today’s fintech lenders. There’s more of course, so if you’re not already subscribed, you’ll want to make sure to do that now so that you receive this and future issues FREE.

AltFinanceDaily’s chief editor Sean Murray is a LendIt awards finalist for best journalist coverage. And while there are already 30 pre-selected judges who will decide the outcome, we would like to thank everyone that has supported us and made our publication possible.

In the meantime friends, stay fresh, stay fintech, stay AltFinanceDaily. The future of finance depends on it.

We’ll see you at the Javits Center for LendIt on March 6th and 7th. If you join the Small Business Lending track, you’ll actually be able to grab a copy of this issue at the conference.

Marketplace Lending Association Announces 11 New Members

January 12, 2017

WASHINGTON, Jan. 12, 2017 /PRNewswire/ — The Marketplace Lending Association (MLA) today announced the addition of eleven new companies to the Association. The new members join as the MLA works to expand its presence in Washington. The MLA was formed in 2016 by founding members Funding Circle, Lending Club, and Prosper Marketplace with the goal of promoting a transparent, efficient and customer-friendly financial system.

New Members include: Affirm, Upstart, CommonBond, Avant, PeerStreet, Marlette Funding, Sharestates, Able, and StreetShares. New Associate Members of the MLA include dv01 and LendIt.

This expansion represents a new chapter for the MLA, as it extends the group beyond consumer and small business lending to include platforms focused on student loan refinancing and real estate, as well as greater diversity of funding models, including lending platforms that hold loans on balance sheet.

“On behalf of the founding members, I welcome these new members to the Association and I look forward to working with them to advance our mutual public goals both in Washington and in state capitols around the country,” said Nathaniel Hoopes, executive director of the MLA. “As MLA member companies continue to innovate and create new opportunities for borrowers and investors, the MLA will play an important role in sharing data and insights that help educate policy makers on the benefits that these companies bring to consumers, businesses, and our financial system.”

To provide policymakers with a general overview of its 2017 agenda, the Association also today sent letters to the incoming Trump Administration and to the leaders of the 115th Congress.

ABOUT MLA

MLA, a professional trade association, was formed in 2016. The goals of the Association are to promote a transparent, efficient, and customer-friendly financial system by supporting the responsible growth of marketplace lending, fostering innovation in financial technology, and encouraging sound public policy at the state and federal level. To be eligible to join the association MLA companies must abide by the highest standards of business conduct in providing credit and services to consumers and businesses.

For more information about MLA, its members and its membership standards, visit the MLA website at www.marketplacelendingassociation.org.

Media Contacts:

Nathaniel Hoopes – Executive Director

Phone: (202) 660 1825

nat.hoopes@marketplacelendingassociation.org

My Marketplace Lending 2017 Projections

January 8, 2017 LendIt co-founder Peter Renton has projected that there won’t be any new industry IPOs this year. While I don’t know if I’d say he’s wrong (a year is a long time), one thing that has changed since 2014 is a shift away from the “tech” label. When OnDeck went public, they positioned themselves as a technology company. Today, they more closely identify themselves as a non-bank commercial lender. Lending Club too was a “tech company.” Now they might be more appropriately characterized as an online consumer lender, especially since their competitors are traditional financial institutions like Discover Bank and Goldman Sachs. So the public markets in 2017 may not be ready for a tech company that can lend but they may be ready for a lending company that has tech. The difference is real.

LendIt co-founder Peter Renton has projected that there won’t be any new industry IPOs this year. While I don’t know if I’d say he’s wrong (a year is a long time), one thing that has changed since 2014 is a shift away from the “tech” label. When OnDeck went public, they positioned themselves as a technology company. Today, they more closely identify themselves as a non-bank commercial lender. Lending Club too was a “tech company.” Now they might be more appropriately characterized as an online consumer lender, especially since their competitors are traditional financial institutions like Discover Bank and Goldman Sachs. So the public markets in 2017 may not be ready for a tech company that can lend but they may be ready for a lending company that has tech. The difference is real.

On regulation, while a Trump presidency may mean that federal regulatory threats will subside, my projection is that the judiciary system will instead play a prominent role in 2017. Whether it’s state courts or federal courts, expect the rules of engagement in marketplace lending or merchant cash advance to become more clear than ever before.

I think it would be easy to predict consolidation in 2017, so more than that, I believe some companies will just wind down and others who arrived too late to the game will just move on to something else. That’s not necessarily a pessimistic outlook since this will give the more serious players a chance to flex their muscles and continue strong growth. This is a natural cycle in any industry that experiences a rapid growth phase.

There will be at least one black swan event. We don’t know what we don’t know.

Lastly, if you want to come up with your own predictions you should attend the 2017 LendIt Conference this March in NYC as it’s the best opportunity to take the temperature and size up the future. I have been to the last three annual LendIt USA conferences and in my opinion each has set the tone for the rest of the year.

You can get 15% off the registration price with Promo Code: AltFinanceDaily17USA.