Competition Steps Up in Canadian Small Business Lending Market

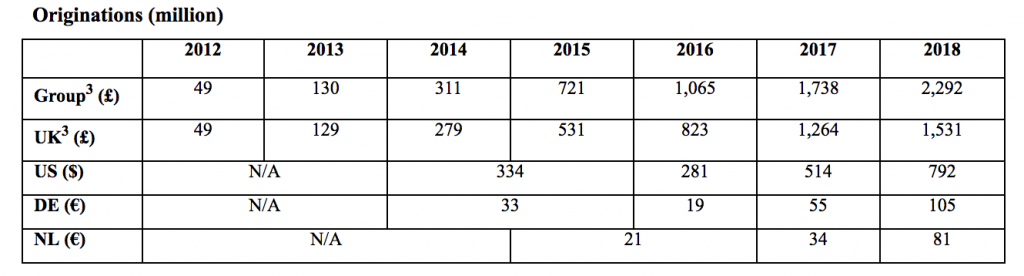

March 11, 2019 Last week’s announcement by Funding Circle that it will establish an operation in Canada later this year is part of a trend of large non-Canadian funders entering or expanding into the Canadian market, according to Adam Benaroch, President of CanaCap, a small business funder based in Montreal.

Last week’s announcement by Funding Circle that it will establish an operation in Canada later this year is part of a trend of large non-Canadian funders entering or expanding into the Canadian market, according to Adam Benaroch, President of CanaCap, a small business funder based in Montreal.

Funding Circle started in the UK and expanded outwards to the US, Germany, and The Netherlands, but the UK still comprises of more than 60% of their global origination volume. Their foray into Canada is a good thing for small business owners and lenders, according to Paul Pitcher, founder and CEO of SharpShooter, a funder based in Toronto.

“I see it as win-win,” Pitcher said.

He said that a win for Canadian small business owners is a win for SharpShooter because it means more potential merchant clients. Pitcher said that he loves OnDeck, a rival, is in Canada, in part because OnDeck’s marketing has helped educate Canadian merchants about alternative lending products.

Similarly, Benaroch said he thinks that big companies entering the Canadian market will affect CanaCap positively. For instance, Benaroch said that CanaCap hopes to capture companies that get turned down from OnDeck. And perhaps CanaCap can also capture merchants that are declined by Funding Circle.

Funding Circle’s loan originations by country by year

Funding Circle’s loan originations by country by year

Benaroch noted that not all outside funding companies have succeeded in Canada, often because they never established a physical presence there. But Funding Circle will be opening a physical office in Toronto.

“We have been evaluating options for expansion over the last year,” said Tom Eilon, who will be Managing Director of Funding Circle Canada. “Canada’s stable, growing economy coupled with good access to credit data and a progressive regulatory environment, made it the obvious choice. The most important factor [in coming to Canada] though was the clear need for additional funding options among Canadian SMEs.”

Funding Circle’s announcement comes on the heels of OnDeck’s December 2018 acquisition of Evolocity Financial Group, a small business funder based in Montreal. While OnDeck started operating in Canada as early as 2015, CanaCap’s Adam Benaroch said that the acquisition of Evolocity is a significant step for OnDeck because Evolocity has an ISO channel in Canada. That runs counter to Funding Circle’s model of mainly going direct to merchant, at least in the US.

Common Mistakes Commercial Tenants Make

March 8, 2019 AltFinanceDaily recently heard a live presentation given by Dale Willerton, “The Lease Coach.” Willerton is an expert in helping commercial retail tenants to find and negationate spaces. But much of his advice applies to commercial office tenants as well. Below are some common mistakes he urges tenants to avoid:

AltFinanceDaily recently heard a live presentation given by Dale Willerton, “The Lease Coach.” Willerton is an expert in helping commercial retail tenants to find and negationate spaces. But much of his advice applies to commercial office tenants as well. Below are some common mistakes he urges tenants to avoid:

Not Looking at Multiple Spaces Simultaneously

You want the landlords pursuing you, not the other way around. Therefore, Willerton said that you want to see multiple spaces at once so that you have options and bargaining power. Particularly if you don’t have much time, you don’t want to be at the mercy of one landlord.

Making the First Offer

Let the landlord make the first offer, Willerton says. If you like a space, tell the broker or the landlord, “Why don’t you send me a proposal.” Otherwise, if you make the first offer, you could end up offering more than what the landlord was willing to accept.

Overpaying for Space

Commercial rent is often based on square footage. So if the space you’re looking at has an unusual configuration, or even if it doesn’t, measure it independently to make sure that you’re paying the correct amount. Even if you are already in the space, if you measure the space and see that you actually have less space than what you’re paying for, you can ask for money back from the landlord. Or at least a rent reduction moving forward.

Telegraphing Your Feelings/Intentions

Don’t let a landlord know that you really like their space or that you really want to renew a lease. It gives them leverage. They now know that you really want what they have and that gives them more negotiating power.

Not Walking Away from a Bad Deal

Like deals that include certain personal guarantees. Some tenants require a personal guarantee and others only ask for it. Find out which and avoid personal guarantees when possible.

Looking Too Successful

If the landlord sees that you’re now driving a Porsche to work, or that your 17-year-old daughter has her own Mercedes, he or she may assume that your business is doing very well and may increase your rent when it comes time for a lease renewal. You may, in fact, be doing well. Or you may just appear to be doing well and then get hurt by a rent increase. This doesn’t mean you shouldn’t drive a Porsche if you can afford it – just to fool your landlord. It’s just something to be aware of.

Not Doing Your Homework

Just as you would do your research on a merchant before funding them, research the building and the landlord. Try to find out how long previous tenants have stayed in the building. Why did the previous tenant leave? Are they expanding, or did they have a bad experience with the building or the landlord? Is the building up for sale? If a building changes ownership, that can impact tenants down the road.

Also, Be Mindful of Commercial Agents’ Motives

Willerton said he doesn’t believe that commercial agents are bad or are working against the tenant at all. But he said that if the agent is getting paid on commission by the landlord, it’s important to be mindful that their ultimate “boss” is the landlord and not you.

The Art of Moving The Deal – When it becomes too high risk for you

February 27, 2019 OakNorth, a small and medium sized business lender and online bank, has mastered a strategy to avoid merchants from defaulting 100% of the time, according to a story published in Quartz. The strategy: tell the merchants at risk of defaulting to refinance their loans at a competitor.

OakNorth, a small and medium sized business lender and online bank, has mastered a strategy to avoid merchants from defaulting 100% of the time, according to a story published in Quartz. The strategy: tell the merchants at risk of defaulting to refinance their loans at a competitor.

“We’ve said [to merchants], ‘Go renegotiate with another bank and refinance,’” OakNorth co-founder Joel Perlman said at the Finovate Europe conference in London on February 14, according to the Quartz story. “And they’ve gone and refinanced and then a few months later they’ve gone into default.”

Perlman’s phrasing may sound a little harsh, but the practice of moving at-risk merchants to another funder is really not uncommon. In fact, it seems like a fairly common and well-understood concept.

CEO of Accord Business Funding Adam Beebe said that brokers will contact Accord when their merchant is up for renewal. And if Accord knows it can’t continue to fund the merchant – either because it has missed payments or because it has become overburdened with other debt – the broker will shop that undesirable merchant elsewhere.

The merchant goes to a new funder and Accord is pleased to be rid of the merchant and not have it default on Accord’s balance sheet. Beebe notes, however, that the new funder is made aware of the merchant’s financial situation and is able to handle the higher risk. Transparency, he says, is important, particularly in a scenario like this.

Similarly, Heather Francis, CEO of Elevate Funding, said that she is more than happy for an ISO to move a stacking and defaulting merchant away from Elevate, as long as Elevate gets paid. Elevate only funds first position and Francis said they make it very clear to merchants that stacking (taking on additional funding from other sources before satisfying an existing contract) is not allowed.

“If a merchant is stacking, that’s not someone we want to work with,” Francis said. “And if the [new] funder understands the high risk, then is fine.”

As long as nothing is being hidden from the new funder, then it seems this practice is just an element of how funding works.

From the broker side, Rob Addison, Managing Member of Sentra Funding, an ISO, said that when a funder knows it will not be renewing one of his merchants, they will ask him to take the merchant away.

Addison said that some funders are so eager to get rid of defaulting merchants that they will offer deals like reducing the merchant’s balance just to get the merchant away from them.

It may not sound nice to jettison a defaulting merchant, but if a funder can avoid a merchant defaulting on its dime, then in many cases, it will.

“We try to move a financially distressed merchant from from, say, an MCA to a longer term loan,” Addison said. “If they haven’t been stacked, they have options. If they have, it’s harder. But if they have something, like commercial property or equipment, there’s usually a [a funder] willing to step in.”

Deal Flow in the Heartland — From Mississippi and Beyond

February 23, 2019

The political, cultural and economic abyss that separates the heartland from the coasts seems to grow deeper and wider with each passing day, and trying to reconcile the disparities can feel nearly hopeless. But differences among geographic locations aren’t nearly so well-defined or as troubling in the alternative small-business funding industry. What’s more, business opportunities can arise when localities differ.

The political, cultural and economic abyss that separates the heartland from the coasts seems to grow deeper and wider with each passing day, and trying to reconcile the disparities can feel nearly hopeless. But differences among geographic locations aren’t nearly so well-defined or as troubling in the alternative small-business funding industry. What’s more, business opportunities can arise when localities differ.

First the lay of the land: Members of the alt finance community agree that funders and brokers are concentrated in just a few geographic locales—Greater New York City, Southern California and South Florida. Those three areas probably generate more than 75 percent of the industry’s volume, according to Jared Weitz, CEO of United Capital Source and one of three co-chairs of the broker council recently formed by the Small Business Finance Association (SBFA).

Sorting out how the industry differs in various regions can prove challenging. The Internet is erasing regional quirks and alleviating the need for physical proximity, says Steve Denis, SBFA executive director. What’s more, every ISO and funder develops a slightly different way of doing business regardless of location, he notes.

However, to a great degree it’s a matter of tweaking a single general outline for navigating the industry no matter where the office or client is based. That’s partially because many members of the industry conduct business in every state or nearly every state.

That said, old-fashioned, small-town ethics can sometimes seem closer to the surface in shops operating far from the coasts. “We’re focused on the values of our organization—like doing what we say we’re going to do, maintains Tim Mages, chief financial officer at Expansion Capital Group, a funder and broker based in Sioux Falls, S.D. “Some of that maybe comes from the Midwest culture or upbringing.”

Outside the major population centers, the industry occasionally seems a little more “laid-back.” In a light-hearted example of a relaxed heartland approach to the alt funding business, Lance Stevens, an attorney who’s a co-founder of Brandon, Miss.-based TransMark Funding, claims he can underwrite a deal while driving his golf cart and listening to Bon Jovi—all while maintaining his under 5 handicap.

Everything can seem a little more slow in the heartland, where people have time to stop and say hello to strangers, says Weitz. “Some folks are like, ‘Hey, my mailbox is three miles from my house, I check my mail once a week. I do not email. I do not fax,’ ” he observes. “It’s a nice change.”

Interactions are often more informal between the coasts. “Being in the Midwest we don’t use a lot of the lingo and terminology from this space, such as ‘stacking,’” says Austin Moss, a managing partner at Strategic Capital in Overland Park, Kan. That lack of jargon may be good or bad, he admits, but instead the staff speaks in a more general, even “holistic,” financial language.

Then there’s the occasional need for the human touch in the heartland. Deals there are sometimes sealed in person, with an office-park conference room substituting for the community bank building on the town square where merchant used to take out loans. “It’s not a widespread trend, but a handful of the ISOs we do business with actually do face-to-face solicitation,” says Mike Ballases, CEO of Houston-based Accord Business Funding.

In line with that mini-trend, an ISO based in Southern California operates a Texas office that specializes in face-to-face encounters, according to Aldo Castro, Accord’s former vice president of sales and marketing. “It’s rather meaningful here,” he says of using the practice in Texas. “You get on the road and shake a hand. They put a face to a name.”

The process can work in reverse, too. A few of the larger local companies seeking funding from Strategic Capital make the journey to the broker-funder’s Overland Park, Kan., offices, Moss says. Bankers who serve as referral partners also like the opportunity to meet in person, he observes.

The personal encounters often strike Moss as “refreshing,” he admits. That’s because the vast majority of the company’s deals occur online and by phone and fax—all without ever seeing the client in person.

Although the desire for personal contact arises from time to time, most heartland deals don’t hinge upon it. “It’s not a big number, but we see it,” Ballases says of face-to-face meetings. “Could it be the wave of the future? Absolutely not.”

Moreover, for some in the industry, the need for face-to-face discussions barely registers. It’s just not about meeting in person, according to Mages. Instead, he cites the importance of other factors. “Speed, convenience and service are the key differentiators, and that’s all driven by data and analytics,” he declares. Partnerships also drive the company’s business, he notes.

Luck outweighs geography, too, in Mages’ view. “It’s more an issue of right place, right time,” he contends. Deals occur primarily when funders manage to attract business owners’ attention at exactly the time when capital’s needed, he contends.

Besides, lots of people tend to think in wide-ranging ways these days instead of in narrow, provincial modes, Mages continues. At Expansion Capital Group, he notes, executives have differing points of view because they come from commercial banking, investment banking, the Small Business Administration lending program and the credit card industry.

Besides, lots of people tend to think in wide-ranging ways these days instead of in narrow, provincial modes, Mages continues. At Expansion Capital Group, he notes, executives have differing points of view because they come from commercial banking, investment banking, the Small Business Administration lending program and the credit card industry.

At the same time, people tend to take an increasingly cosmopolitan approach to their jobs, according to Mages. He notes that executives at his company maintain contacts across the continent, often forged in earlier chapters of their careers.

Meanwhile, well-trained employees can use a phone call to gather the details they need and establish a consultative relationship without a thought for geography or the need for face-to-face meetings, Mages says.

However, geography can indeed play a role at least once in a while. In a few cases merchants prefer a funder with an address across town or at least in the home state. Sometimes business owners and referral partners choose local brokers or funders simply because their names sound familiar.

Strategic Capital, for example, does more business at home than anywhere else, Moss says. The company’s headquarters is in the portion of greater Kansas City that spills over from Missouri into the state of Kansas, making the location convenient to a major population center.

But despite the massive size of greater Kansas City, Strategic Capital remains the only alternative small-business funding option in the area—there just aren’t any other local providers, Moss says. It’s not like New York, where banks and merchants can choose from among many brokers and funders, he says.

That trend toward being the only game in town or one of just a few can hold true for most companies in the heartland, Moss maintains. A broker or funder based in Denver, for example, would probably have higher volume there than anywhere else, he notes.

Several reasons explain that geographic bias, Moss continues. “The employees live there and have contacts, and we’re part of the local associations and chambers,” he notes. “We work with just about all the banks in the area, and everyone knows who we are.” The company also handles local government bonds and local construction projects, he says.

Mages offers a different perspective. Only a few small-business owners in South Dakota choose Expansion Capital Group because they prefer dealing with a Midwestern company or because they’ve seen local press coverage or heard Expansion’s recruiting ads on the radio, he maintains.

Hometown, home state or regional preferences aside, executives at Accord emphasize the importance of the small-town approach of knowing their customers as well possible. For Ballases—the Accord chairman who started the company with Adam Beebe, who now serves as CEO—that means combining personal and impersonal approaches to underwriting.

Ballases views funders and brokers as falling into three categories. Some choose a personal, hands-on approach and don’t rely upon algorithms. A second category emphasizes automation. A third blends the personal and the automated. His organization falls into the latter, he says

For Accord, the personal comes into play because of what Ballases has learned in his decades in the banking business. He knows margins and growth rates in his applicants’ industries, and those factors aren’t often incorporated into algorithms, he says.

In fact, commercial banks have failed to learn to evaluate small businesses on their true merits, Ballases continues. Banks tend to underwrite small businesses, which he defines as those in need of $100,000 or less, by using a “skinnyed-down” version of how they underwrite big companies, which they base on general financial information. Instead, he counts on discipline, data and his 50 years of experience in commercial banking to evaluate a merchant on an individual basis.

At another company, TransMark Funding, Stevens and his partner draw upon legal and small-business experience to evaluate potential customers’ creditworthiness. “That causes us to focus on an applicant’s business model and their sustainability, which may boil down to personalities,” Stevens says. Transmark combines those factors with “a little bit of credit metrics” to come to decisions on applications.

The company’s mix of objective and subjective reasoning differs starkly from the thought process at most coastal funders, Stevens says. While his company gives most of the weight to the subjective and just a bit to the objective, big-city competitors tend to do the exact opposite, he says.

Of the last five MCA deals that Transmark funded, the merchants averaged 12 checks returned for insufficient funds per month, Stevens says, noting that he can make that statement “with a straight face.” Sometimes it’s been as high as 35 NSF checks per month for successful applicants. “Those people would not even get into the parking lot of a bank and would not get through the door of any MCA funder who’s using any sort of reasonable metrics,” he adds.

An anecdote helps explain the thinking. Suppose a restaurant has been operating for several years in a town of 50,000 and has amassed 2,200 “likes” on its Facebook page, Stevens suggests. “I’m in,” he exclaims, noting that it would take compellingly negative numbers to convince him that the business won’t survive if he helps it obtains capital to improve its positioning in its market.

The vignette illustrates that a business can do well in the community despite the merchant’s financial difficulties, Stevens says. However, the story doesn’t mean Facebook becomes the only determining factor, he continues. Positive factors for success include good location and marketing, he notes.

The principals at many companies funded by TransMark have credit scores in the low 500’s, Stevens continues. “That’s tough,” he says, “because they’re going to have a lot of history of not living up to their financial obligations.” But if someone with that credit score has personally guaranteed a lease on a storefront for the next two years, they may be unlikely to abandon the business. A big bank might look upon that merchant as insufficiently nimble because of the lease, but TransMark takes the opposite view, he says.

Even if a store, restaurant or contractor is “circling the drain” and about to shut down, TransMark may simply believe the owner has the character to make the business work. “Given our minute default rate, we’re right most of the time,” Stevens maintains, adding that banks see applicants as customers, and TransMark sees them as partners.

The business model requires peering into the future to see how the merchants will look after using perhaps $25,000 in capital to make improvements and while dealing with 18 percent holdback for the next six months, Stevens observes. “If they look strong, I need to fund them,” he says of the company’s prognostications.

To find ISOs who appreciate the TransMark model, the company seeks out purveyors of credit card merchant services, Stevens says. They encounter those merchant-services providers at trade shows and through “some general poking around,” he notes.

The merchant-services people often have long-standing relationships with merchants and thus can feed information into the TransMark way of viewing deals. “Tell me what it looks like when you walk into their store at 11 a.m.,” Stevens says to illustrate the kind of conversation he has with ISOs. “How is their signage?”

Besides understanding clients, it also pays to understand markets, and proximity can help with the latter, according to Ballases and Castro in Houston. “We have an affinity for Texas,” Castro says.

Many of the businesses based in Texas are vendors to people—like mechanics who fix cars or restaurants that feed people—not vendors to businesses, Ballases notes. Vendors who cater to people are better candidates for merchant cash advances than business-to-business companies are, he maintains.

“It’s just a huge state,” Castro declares. “We’ve got a thousand new residents moving to Texas every day.” Nearly 10 percent of the nation’s small businesses operate in The Lone Star State, he notes.

“There’s a convergence of the population growth, a low tax rate, low regulations, low cost of running a small business relative to national levels, and a great small-business environment,” Castro says of the Texas scene. “In addition, the healthcare industry is exploding here, and there are the ancillary businesses to healthcare.”

Meanwhile, the state’s Hispanic entrepreneurs remain under-served by alt funding ISOs, which presents a great untapped opportunity, Castro maintains. Funders who cater to those Hispanic merchants will find them loyal, he predicts. In Texas alone, Hispanic consumers spend half a billion dollars annually, he says.

To capitalize on that burgeoning market, Accord has assembled a team that can help Anglo ISOs bridge the cultural and linguistic gap, Castro says. “We do that every day,” he maintains. “We’re jumping on the phone with merchants and helping them get the funding they need to support the growth of their operations.” Those conversations with merchants do not put Accord in competition with ISOs, Castro notes. Accord does not maintain an inside sales staff and does all of its business through ISOs, he says.

Only a few of those ISOs are based in Texas, according to Ballases. Most of Accord’s ISOs operate from offices in the Northeast, with many in the other common geographic spots of South Florida and Southern California, he says. So that makes Accord a national company despite its emphasis on Texas, Ballases says.

Accord’s experience at home, combined with nationwide contacts in the industry, have convinced the company’s leadership that too many brokers remain unaware of the opportunities in Texas.

That’s why Accord is producing ads, videos, infographics, blogs and social media posts to alert those coastal ISOs to opportunities in Texas. The company even offers a tab called “FundTEX” on its website. “We’re getting the word out,” Castro says of the company’s effort to publicize his state.

Besides operating in areas sometimes overlooked on the coasts, heartland brokers and funders sometimes have to reinvent the industry almost from scratch. Brokers can find themselves teaching the business to potential investors outside the Big Three geographic locations, Moss says. In New York, investors already know the industry and use that familiarity to evaluate brokers, he says.

Brokers and funders also have to deal with the heartland’s lack of workers with industry experience. As the lone company in the market, Strategic Capital, for example, can’t find many prospective employees with previous jobs in the business, Moss notes. “There is no OnDeck or Yellowstone or RapidAdvance down the street to provide a talent pool for hiring,” he says.

That’s good and bad, Moss maintains. New hires don’t require re-training to lose habits that don’t fit the Strategic Capital way of working. But it’s difficult to find underwriters, accountants and other prospective employees with the right background. It doesn’t work to put new salespeople on straight commission because the “ramp-up” period takes longer with employees unfamiliar with the industry, he says.

The lack of local experience sometimes prompts brokers in the heartland to tap the Big Three areas for talent. Expansion Capital Group, for example, has a business development director in New York who came from another ISO, Mages says. Besides cultivating relationships in NYC, the business development expert makes frequent trips to Southern California and South Florida.

Meanwhile, members of the industry who tire of the rapid pace on the coasts might want to consider moving inland to fill the vacant jobs, sources suggest. After all, the heartland has its advantages, according to Moss. “Most people here have houses, and the cost of living is lower than in places like New York,” he says. A spacious five-bedroom house in Kansas City might cost less than a cramped apartment in New York, he notes.

To commute to the company’s suburban office, his typical employee jumps into a car in a climate controlled attached garage, cruises for half an hour or so on roads relatively free of traffic and parks in the lot a few steps outside his office building. It’s less stressful than crowding into a subway car, he notes.

The hinterland’s not as culturally barren as some might believe, Moss continues. The public hears “Kansas City” and they think of tornadoes, cows and the Wizard of Oz, he says. But the reality includes a downtown replete with skyscrapers and pro sports, not to mention lots of tech, healthcare and aerospace companies. “It’s like a mini-Chicago,” he notes.

But a retreat from the coasts may not be in the offing. Ballases expects that the majority of ISOs will continue to concentrate on the East Coast and West Coast because that’s where population growth remains strongest and thus provides the most opportunities. “It’s a numbers game,” he observes.

How Should a Funder Market?

February 20, 2019 Whether it’s marketing to ISOs or for direct leads, funders have different marketing techniques that suit their size and business philosophy.

Whether it’s marketing to ISOs or for direct leads, funders have different marketing techniques that suit their size and business philosophy.

Credibly, a New York-based company of 160 employees, works with LendingTree and uses Google and Facebook for leads. But Director of Marketing and Strategic Partnerships Jeffrey Bumbales said that advertising on large pay-per-click channels may not be the right move every funder.

“If you’re unsure as to whether [Google or Facebook] are worth pursuing, lead generators are a great benchmark. If your average cost per lead is more expensive than the market price, you’re better off allocating your spend towards the lead generators and other channels.”

Credibly has used LinkedIn for marketing, but Bumbales acknowledged that the platform can be very expensive. They have used Sponsored InMail, which sends direct messages to targeted business owners. Bumbales said this can be very effective, but it requires you to have at least one person managing the responses, which can be very time intensive.

Bumbales also emphasized the importance of diversifying lead sources such that you never have more than one-third of your marketing spend devoted to one source.

Heather Francis, CEO of Elevate Funding, never devotes more than one-third of her marketing in any one area. That’s because she doesn’t really do any marketing. Yup. Elevate, a funder of about 20 employees in Gainesville, FL, gets by just fine without marketing.

“It’s all word of mouth and networking,” Francis said.

Francis says she loves it when an ISO will say “I keep seeing your [company] name on merchant bank statements,” meaning that when files get circulated, the ISO keeps seeing that merchants are being debited by Elevate.

Francis has taken the approach of letting others approach her company. Kind of like dating.

“We want to work with people who want to work with us,” Francis said. “And in this business, everything is reputational based.”

If there’s anyone who knows anything about marketing, it’s Jennie Villano, Vice President Of Business Development at Kalamata Capital Group.

Villano uses LinkedIn to market to ISOs, posting friendly videos of herself speaking directly to the ISO community on an almost daily basis.

Last year, Villano started a cooking show video series on her LinkedIn page called “Cooking with Kalamata,” in reference to her company’s name. In each video, she invites a different guest to cook something with her in an informal home kitchen setting.

“Cooking has nothing to do with lending, but it doesn’t matter,” Villano told the audience on a marketing panel at last year’s Broker Fair.

The cooking shows allow potential clients to see her in a casual, non-business environment so that even if she hasn’t met many of her LinkedIn contacts, they feel like she’s a personal friend.

“And people want to do business with their friends,” she said.

Tips For Trade Show Success

February 14, 2019

Conference season will soon kick off, but many attendees are at a loss at how to score big at these events. Without a doubt, trade shows and conferences offer participants a prime opportunity to boost brand exposure, make professional connections and increase sales.

But there’s also a lot of behind-the-scenes work required to turn these events into successful business endeavors. While the playbook won’t be the same for every company, here are some tried-and-true tips to help attendees get the most out of conferences.

Start by determining which conferences to attend. With dozens to choose from, it’s not realistic from a budget, time or value perspective to hit every conference, says Jim Larkin, who manages events for OnDeck. Companies should select conferences based on which ones make the most sense for their goals and objectives. Not all conferences will offer the same benefits to every company or industry professional, frequent conference attendees say.

Ideally, management teams should meet early in the year to weigh the pros and cons of each conference, against the backdrop of the company’s budget. Some factors to consider include where and when the conference is being held, which of your competitors, prospects and customers are likely to attend and how many employees it makes sense to send, if any. “Budgets drive everything and you want to be smart with spending money,” says Janene Machado, Director of Events for AltFinanceDaily, whose flagship conference, Broker Fair, is scheduled for May 6 in New York. “You need to be strategic about why you are attending a particular conference,” she says.

It’s essential to plan ahead for each conference to make the most out of the event. This includes carefully combing through the agenda, scheduling meetings ahead of time and getting acquainted with the physical layout of the event space. If more than one company representative is attending, it’s also important to coordinate their activities in advance to avoid duplicating efforts and to maximize productivity.

“You have to make your own luck at these conferences,” Larkin says.

Most events have an online or mobile agenda and networking portal that are open to participants at least a few weeks beforehand. Bookmark the sessions you would like to attend, build your wish-list of people you would like to meet and start requesting meetings as soon as possible, says Peter Renton, co- founder and co-chairman of LendIt Fintech, which has an upcoming conference scheduled for April 8 and 9 in San Francisco. “Last year we helped to enable nearly 2,100 meetings at our USA event, and most of those meetings were organized through our networking portal,” Renton says.

Don’t delay when it comes to setting up advance appointments because schedules can fill up quickly, says Monique Ruff-Bell, event director for Money20/20 USA, which will take place in Las Vegas from Oct. 27 through Oct. 30. “Identifying the right contacts beforehand, reaching out and establishing what you’d like to achieve in a short meeting will make your time much more productive,” she says.

It’s fine for attendees to leave some time in their schedule for impromptu meetings as well; just be sure to fill those slots, says Ken Peng, head of business development and marketing at Elevate Funding. “No one should ever be asking, ‘what are we doing next?’ You should know,” he says.

It’s also a good idea to plan ahead for a dedicated meeting space so you’ll have a convenient, comfortable and quiet space to conduct meetings, seasoned conference attendees say. This can be especially important at big conferences where thousands congregate. For those who don’t want, or can’t afford, to pay for a meeting room, it’s a good idea to find a quiet restaurant or coffee shop outside the busy convention center area where you can have quiet, uninterrupted, productive conversations in a relaxed environment, says Larkin of OnDeck. Don’t choose the heavily frequented coffee shop next to the hotel where meetings are sure to be disrupted by heavy foot traffic, he says. “Get away from the noise, the hustle, the chaos. Quiet is king.”

Conferences can be expensive, so it’s important to make the right decisions with the available budget. For instance, companies don’t have to miss out on promotional opportunities just because the highest level of sponsorship is out of reach for their budget. Instead, look for creative ways to make an impact without breaking the bank, says Stephanie Schlesinger, director of marketing for LEND360.

Schlesinger suggests that would-be sponsors have an open conversation with conference organizers about what they can afford to spend and what they hope to reap in return for their marketing dollars. She offers the examples of companies that have sponsored popcorn breaks, pens and pads of paper, badges, lanyards and other marketing materials. “There could be opportunities to do something very unique. By brainstorming together we can think of outside-the-box opportunities to really make an impact for your brand,” she says.

Another cost consideration is where to stay. Though it can be tempting to save a few bucks by bunking off-site, that’s not always the most prudent decision, frequent conference attendees say.

“Time is really valuable at these shows and events. If you’re staying off-site you have to battle everybody for the cab line, and the increased expense of commuting can offset any cost savings,” says Sheri Chin, chief marketing officer at BFS Capital. Also, staying on-site “gives you more flexibility when unscheduled things come up,” she says.

If staying on premises isn’t an option, conference attendees should make extra efforts to spend considerable time in the bar or lobby of the conference site, says Jeffrey Bumbales, marketing director at Credibly. People will come in and go and it’s an easy way to start conversations, he says.

Conferences typically consume a lot of energy, so Eden Amirav, chief executive and co-founder of Lending Express, recommends participants try to catch people well before they are running on empty. As the conference goes on, it becomes harder to engage people because they also get drained, he says. Typically conference doors open a few hours before the first sessions begin, and this can be an especially effective time to network, Amirav says.

Arriving early also allows participants to find their way around. Ruff-Bell of Money20/20 USA recommends participants walk through the entire event space upon arrival to get their bearings. “Many of these large conferences can be overwhelming, and knowing where to go will help with your time management,” she says.

Bumbales of Credibly also recommends conference attendees pack their schedule tightly—even though it might mean activities extend late into the evening. Instead of calling it quits at 6 p.m. he recommends conference attendees plow through and host evening meetings over dinner or drinks. Even though a participant may be tired, it’s best not to miss these important networking opportunities, he says.

The proper conference mindset includes knowing there’s a good chance sleep won’t be plentiful. To accommodate, Bumbales tries to ensure he’s well-rested before a conference. He also makes sure to pack protein bars and non-perishable snacks for replacement meals as needed throughout the conference in case he needs to eat on the go. The goal is to hit the ground running and be able to focus entirely on conference-related business, he says.

Although numerous social opportunities abound at conferences, not everyone takes advantage. Certainly not everyone is as comfortable approaching strangers. But it’s important for conference- goers to try to break out of their shell whenever possible, industry professionals say. When he first started going to conferences, Gary Lockwood, vice president of business development at 6th Avenue Capital, says he found it difficult to strike up conversations with strangers because it took him out of his “comfort zone.” But he forced himself to make the extra effort, and it has served him well. He says that some of the best connections he’s made have come from these chance meetings at breakfast, lunch or during random breaks.

Although attendees don’t always stay on-site for meals, Peng of Elevate Funding recommends people stick around during these times, if possible. He finds these meals a good opportunity to chat with others in a comfortable setting as opposed to the more strained conversations that can happen when someone approaches him at an exhibitor booth. These informal conversations offer a better chance to build a rapport with someone and learn—in a non- pressured environment—about what the other person does, he says.

Although attendees don’t always stay on-site for meals, Peng of Elevate Funding recommends people stick around during these times, if possible. He finds these meals a good opportunity to chat with others in a comfortable setting as opposed to the more strained conversations that can happen when someone approaches him at an exhibitor booth. These informal conversations offer a better chance to build a rapport with someone and learn—in a non- pressured environment—about what the other person does, he says.

Bumbales of Credibly says elevator time offers another opportunity for chance meetings that can turn into business opportunities. Most times, he prefers to take the stairs, but not at conferences. Elevators can be great for short, yet productive conversations. He likes to position himself next to the elevator buttons, which gives him an opening to break the ice. He says he’s had a few business opportunities arise as a result of elevator conversations.

It’s also important not to monopolize anyone’s time says Machado of AltFinanceDaily. Everyone is there to meet as many people as possible, so she recommends keeping conversations quick, meaningful and relevant.

It’s also important not to monopolize anyone’s time says Machado of AltFinanceDaily. Everyone is there to meet as many people as possible, so she recommends keeping conversations quick, meaningful and relevant.

When he’s talking to someone for the first time, Lockwood of 6th Avenue Capital tries to listen more than he speaks. “I want to listen a little more than I talk in the beginning so I can tailor the conversation to what they need.”

While not every exchange will be fruitful, it’s important to recognize that any conversation could lead to future business; even a commercial real estate broker who has no present connection to merchant cash advance can be a potential partner or resource at some point, Lockwood says.

It’s also a good idea to keep your business cards handy at all times. Bumbales says he’s been in several situations when people don’t have them available, which makes exchanging information more awkward. “It’s a lot less awkward to exchange business cards then it is to ask for someone’s cell phone number,” Bumbales says.

Because each day is so jammed- packed with information, it’s a good idea to take notes so you don’t lose track of important details, says Ruff-Bell of Money20/20 USA. Each person will have his own system, but effective note-taking becomes important for recapping the event back in the office and for sending post-event follow-ups to new contacts. “At the end of each day, go through your notes and clean them up, ensuring you’ll understand the key points and important details weeks later,” she says.

Some conference participants fall short when it comes to following up with new connections they’ve made, but this can be a grave mistake. Follow-up emails are most effective when they are personal, says Peng of Elevate Funding. He recommends attendees jot down a few notes on the business card of each person they meet to jog their memory later on about their conversation. Then, weave details of the conversation into the follow-up email, so the correspondence won’t seem cold, generic or canned, he says.

Remember, conference-goers will be meeting hundreds of other people at the conference, Ruff- Bell says. “Ensure your follow-up is prompt, effective, and most importantly, memorable,” she says

Even though the setting is social, conference attendees need to be mindful about maintaining proper decorum at all times. This is a seemingly obvious rule of thumb that people sometimes forget, conference participants say.

“You’re there for work first, play second,” Peng says.

Professionalism also dictates that attendees and exhibitors should be where they are supposed to be at appropriate times. Peng recalls a conference he attended last year where one of the exhibitors left its booth unmanned for most of the conference. There’s no way to know where an interaction at these booths can lead in terms of new business or face-time with existing clients.

“It’s not doing the company any favors” by passing up the opportunity, he says.

With Interest Rates Up, OnDeck’s Cost of Funds Comes Way Down

February 12, 2019 OnDeck’s cost of funds dropped significantly in 2018, according to their last quarterly report. The rate was 5.6% in Q4, compared to the 6.8% it started off at in Q1.

OnDeck’s cost of funds dropped significantly in 2018, according to their last quarterly report. The rate was 5.6% in Q4, compared to the 6.8% it started off at in Q1.

During the earnings call, OnDeck CEO Noah Breslow said, “We improved the terms and structures of our credit facilities and increased the number and quality of our funding providers, adding new banks and life insurance companies.”

That’s all before OnDeck even closed on an $85 million revolving credit facility with a lender group consisting of four banks earlier this month. The rate on that came in at 1 month LIBOR (currently around 2.5%) + 3.00%.

OnDeck’s loan yield in Q4 was the highest its been in the last 2 years at 36.6%.

The company enjoyed record earnings for Q4 2018 ($14 million) and full year 2018 ($27.7 million). They also had record origination volume of $658 million, a 2% increase from Q3 and a 21% increase from Q4 2017. Their sales and marketing expense for acquiring new customers remained flat compared to last quarter.

New Jersey MCA & Business Loan Disclosure Bill Update (S2262)

February 6, 2019 Bill S2262 in the New Jersey State Senate mandating disclosures on MCA and business loan contracts, was amended last week. In its current form, the bill, if it became law, would require MCA providers to disclose:

Bill S2262 in the New Jersey State Senate mandating disclosures on MCA and business loan contracts, was amended last week. In its current form, the bill, if it became law, would require MCA providers to disclose:

- the total dollar costs to be charged to a small business concern, assuming the small business concern delivers all purchased receivables to providers at the time they are generated or at a mutually agreed upon time, and all required fees and charges that are paid by the small business concern and that cannot be avoided by the small business concern;

- the amount financed, which shall mean the advance amount less any prepaid finance charges; and

- for a cash advance that calculates repayment costs dependent on the small business concern’s future receivables, the estimated annual percentage rate, provided as a range, with at least three different repayment times provided and a narrative explanation of how each rate was derived. Any estimated annual percentage rate is to be calculated using a projected sales volume that is based on the small business concern’s average historical sales or the sales projections relied on by the provider in underwriting the cash advance; or

- for a cash advance that calculates repayment costs as a fixed payment, the annual percentage rate, expressed as a nominal yearly rate, inclusive of any fees and finance charges.

Brokers would also be required to provide uniform fee disclosures to both the small business owner and lender or MCA funding provider in a document separate from the funding contract before a small business consummates a loan or MCA transaction.

Previously, the bill defined merchant cash advances as loans. The latest draft updated the definition to mean a financing option that allows a small business concern to sell all or a portion of its future sales collections or other future revenues in exchange for an immediate payment. It refers to this as an asset-based transaction.

You can follow the bill’s updates and read the latest drafts here.

S2262 was originally introduced 11 months ago in March 2018.

{kind=link}