Loan Brokers or Self Origination? Here’s What Experts Say

February 22, 2016 Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

But a year on, as the dust has settled, we asked industry veterans what it means to remain successful in this business and what is the key to sustainability — is it in going for the ISO/broker channel to find deals or originating your own.

Here’s what they had to say

Don’t Break the Broker

Tom Abramov of MFS Global voted for the ISO/broker channel and said that that’s how the company strictly does deals, working with brokers who have a track record as a part of their recruitment system. The six year old company that started as an broker shop now focuses only on funding with products that are a mix of merchant cash advances and lines of credit.

“We don’t look at FICO scores or SIC codes, we only look at cash flows of businesses,” said Abramov. “I want to see if I give a someone a dollar whether they can turn it into two.”

Abramov added that his firm offers brokers 20 percent commission and their default rates are sub 5 percent.

The advantages of scoring deals through a broker channel can be alluring. It involves no overhead, no staff that needs compensation, motivation and incentives, and makes use of the existing broker-merchant relationships.

Jordan Feinstein of NuLook Capital said that his firm works with brokers exclusively and the model has helped them respond to merchants faster. “We do not have a sales team speaking to merchants directly, that’s in conflict with our model,” said Feinstein. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” he said.

Building a Hybrid Model

There are some others who want to make the best of both the models and work with brokers while originating and funding their own deals. Forward Financing which uses a hybrid model has strategic partnerships with some brokers while still originating their own deals. “We have a hybrid model because our goal is to have a program for any type of business and work with companies across the spectrum of risk,” said Justin Bakes, CEO of Forward Financing. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said.

The Original Origination

While the allure of a lean business is certainly attractive, there are some who are in the industry to build a bigger business and create value by making it robust — Jared Weitz of United Capital Source is one of them. “There is a big market for both analytical process as well as sales process. It’s important to go after your strength,” said Jared Weitz, founder and CEO of United Capital Source. “When you originate and fund your own deals, you’re in a rewarding position and in control of how merchants get treated.”

Industry Trends

Speaking of the industry in general, these experts agreed that the business was undergoing a change with new entrants coming in and experimenting with better services and technologies.

“Last year was the year of brokers but we are still missing the education with merchants. Some brokers are interested while some are not,” said Abramov.

“I notice a clear difference between the old and the new in terms of technology and pricing model,” said Bakes.

“New funders are coming in with different products and terms with increased competition in the ISO market,” said Feinstein.

“Marketing is getting more expensive and only the ones who can afford to pay can play,” said Weitz.

AltFinanceDaily Nov/Dec Teaser

December 1, 2015The November/December issue of AltFinanceDaily Magazine should go out in the mail at the end of this week. In the meantime, can you guess who is on the front cover of this issue?! Here’s your clue:

Jared Weitz, the CEO of United Capital Source, was on the cover of the previous September/October issue.

Alternative Lending Becoming Less Alternative

August 23, 2015 Alternative funders are looking a little more like bankers these days, but that’s not to say they’re developing a taste for pinstriped three-piece suits and pocket watches on gold chains. They’re promoting bank loans, applying for California lending licenses and contemplating the unlikely possibility that one day they’ll obtain their own bank charters.

Alternative funders are looking a little more like bankers these days, but that’s not to say they’re developing a taste for pinstriped three-piece suits and pocket watches on gold chains. They’re promoting bank loans, applying for California lending licenses and contemplating the unlikely possibility that one day they’ll obtain their own bank charters.

“It’s what everybody’s talking about,” said Isaac Stern, CEO of Yellowstone Capital LLC, a New York- based funder. “If it’s not in their current plans, it’s in their longer-term plans over the next three to five years.”

Funders promote bank loans to drive down the cost of capital, sell a wider variety of products, offer longer terms and bask in the prestige of a bank’s approval, said Jared Weitz, CEO of United Capital Source.

Loans allow for much more customization than is possible with merchant cash advances, noted Glenn Goldman, CEO of Credibly, which was called RetailCapital until a little less than a year ago. The name changed as the company began offering loans in addition to it original advance business. It’s now working with three banks.

While the terms don’t vary much with advances, borrowers can pay back loans daily, weekly, semi-monthly or monthly, Goldman said. Loans can also include lines of credit that borrowers draw down only when they choose. Interest rates on loans can vary, too, he said, and loans can come due after differing periods of time.

Besides that flexibility, loans also offer familiarity among merchants and sales partners – unlike the sometimes baffling advances, Goldman said, adding that “everybody knows what a loan is, right?”

Loans have so many advantages over advances that Credibly expects its loan business to grow more quickly than its advance business, said Goldman, who was formerly CEO of CAN Capital.

Those advantages are also encouraging other advance companies to form partnerships with banks to provide merchants with loans that aren’t subject to state commercial usury laws, said Robert Cook, a partner at Hudson Cook LLC, a Hanover, Md.-based financial services law firm.

The advance company markets the loan to the customer, the bank makes the loan, and the advance company buys it back and services it at the rate the bank is allowed under federal law, Cook said. The bank doesn’t lose any capital, it takes on virtually no risk and it profits by collecting a few days’ interest or a fee, he noted.

Where the bank’s located can make a big difference. A bank based in New York, for example, can charge only 25 percent interest no matter where the customer resides, while New Jersey allows banks to collect unlimited interest anywhere in the country, Cook said.

But the partnerships funders are forming with banks could face a threat. The United States Court of Appeals for the Second Circuit ruled in May in Madden v. Midland Funding LLC that a non-bank that buys a loan cannot charge interest set where the bank is located but must instead charge interest according to the laws of the state where the consumer is located, Cook noted. That could mean a lower rate.

In Cook’s view the case was poorly argued, the decision was wrong and the ruling may be reversed, “but it has to trouble someone who is thinking about starting up a bank partnership,” he said.

The court was asked whether the rules that apply to a national bank also apply to the non-bank that bought the loan, Cook maintained. That’s not the question, he asserted. The argument should have been that the idea of “valid when made” should take precedence. It states that a transaction that’s not usurious when it’s made doesn’t become usurious if a party takes action later – like reassigning the note, Cook said.

Meanwhile, offering bank loans isn’t the only way alternative funders are coming to resemble banks. Some are obtaining what’s formally called a California Finance Lenders License that enables them to make loans in that state.

California began requiring the license in response to lawsuits over the cost of advances. The state has published a licensee rulebook that’s about the size of an old-school New York phone book – the kind kids sat on to reach the dining room table, according to Yellowstone’s Stern, who completed the licensing process three years ago.

Getting the license took 15 or 16 months and required lots of help from the legal team at Hudson Cook, Stern said. The state investigated his back- ground and fingerprinted him. The cost, including lawyers’ fees came to about $60,000, he recalled.

“Man, it was like pulling teeth to get that license,” Stern said. Keeping it’s not easy, either. “We guard that thing fiercely,” he maintained. “They’ll take away your license if you even sneeze the wrong way.”

The hassles have paid off, though, because Yellowstone now deals directly with California customers instead of sharing the profits with other companies licensed to operate there. What’s more, companies that don’t have licenses are sending business Yellowstone’s way.

The hassles have paid off, though, because Yellowstone now deals directly with California customers instead of sharing the profits with other companies licensed to operate there. What’s more, companies that don’t have licenses are sending business Yellowstone’s way.

Retaining the profits from loans is also prompting some funders to contemplate applying for their own bank charters. But Cook, the attorney from Hudson Cook, sees little or no chance of that happening.

Federal bank regulators are reluctant to grant charters to mono-line banks – institutions that perform only one financial-services function, Cook said. “It’s risky to put all your eggs into one basket,” he maintained.

Regulations make forming or acquiring a bank so difficult for businesses that want to make small loans at high rates, Cook said. “If that’s going to be their business plan, they’re not going to get a bank.” A state charter requires the approval of the Federal Deposit Insurance Corp., which isn’t likely, he noted.

Utah industrial banks and Utah industrial loan companies are insured by the Federal Deposit Insurance Corp. but aren’t considered bank holding companies, Cook said. However, that’s a regulatory loophole that may have closed and thus may no longer offer a way of becoming a bank, he noted.

Clearly, the complications surrounding bank loans, lending licenses and bank charters mean that becoming more bank-like requires more than a pinstriped suit.

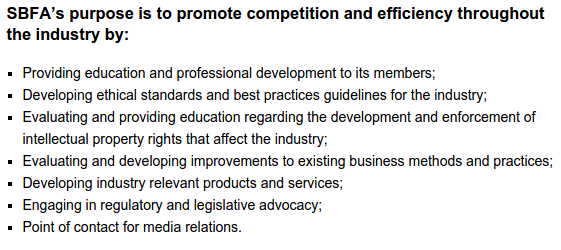

Is NAMAA Reborn? Meet the Small Business Finance Association

April 14, 2015Almost seven years ago exactly, the North American Merchant Advance Association announced their presence. As of today, they are now officially the Small Business Finance Association (SBFA). Back then, a release dated April 15, 2008 stated:

The North American Merchant Advance Association, Inc. (NAMAA) has recently been created to represent merchant cash advance providers and to promote competition and efficiency throughout the merchant advance industry. NAMAA’s members will have the opportunity to share industry education and professional development, ethical standards and best practices guidelines, the development of industry relevant products and services, and the engagement in regulatory and legislative advocacy.

Of the ten original members, a handful are no longer operating. NAMAA’s membership in 2008 arguably encompassed the entirety of the merchant cash advance industry sans AdvanceMe (now named CAN Capital). Today, the SBFA website currently lists seventeen members. The organization has clearly grown but it pales in comparison to the size of the industry in 2015.

Internal data indicates that there are well over one hundred direct providers of merchant cash advance. Several hundred more are ISOs/brokers that co-invest in merchant cash advance transactions (Strategic Funding Source has had more than 200). And there are more than one thousand ISO/brokers that resell the product nationwide.

On this basis alone, less than two percent of industry providers and resellers are members of the trade organization. Granted, the seventeen member companies likely make up at least 15% of the industry’s funding volume. Member company Merchant Cash and Capital for example, announced just last month that they had funded $1 billion since inception.

Some have viewed the organization’s membership as overly exclusive and resistant to change. A seasoned veteran of an ISO that wished to remain anonymous said prior to the organization’s announced changes that, “NAMAA served a purpose for a long time but as the industry has changed, they have not.”

Ironically, Goldin’s statement in today’s release couldn’t be any more well timed. “With the alternative financing industry growing exponentially into a multi-billion dollar industry, we felt it was time for the trade association to evolve with it and open itself up to all types of small business alternative financing providers hence the name change to Small Business Finance Association,” he said.

The shift clearly acknowledges the true dynamic of the industry’s growth, that it’s not all merchant cash advance anymore.

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

But with lenders added to the mix of potential constitutents, is the SBFA a little light? The SBFA will now represent less than 1% of the companies selling or reselling merchant cash advances and business loans. In growing membership however, patience may perhaps be a virtue.

Jared Weitz, CEO of United Capital Source, said, “NAMAA is a beneficial association in the industry and should be choosy with who they let in.” As a broker, his company has historically not been eligible for membership.

Similarly, Chad Otar, Managing Partner of Excel Capital Management, whose company has also not been historically eligible for membership, said, “The aim of NAMAA is to help out our audience to understand and remember the information we stand for as funders and ISOs.”

Otar’s point belies a troubling trend, that many players in this industry disagree about what it is they stand for.

In a AltFinanceDaily Magazine article, titled, Stacking: Is it Tortious Interference?, Robert Cook, Cathy Brennan, and Kate Fisher of Hudson Cook, LLP delved into the industry’s most polarizing debate, the practice of entering into a cash advance transaction or loan knowing that the merchant has one or more open cash advances or loans with a competitor. They wrote:

On one side are companies that only originate first-position deals. These companies generally include a clause in their contracts prohibiting the merchant from obtaining another merchant cash advance or loan until the company receives all of the future receivables it has purchased or is fully repaid. First-position companies view stacking as a threat to recovery of money advanced or loaned to merchants. On the other side are companies that routinely offer second or third-position deals. These companies argue that merchants with adequate cash flow to support additional advances should be free to obtain them.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Lawyers at Hudson Cook, LLP echoed the same. “In the last several months, at least two first position companies have sued their stacking competitors, claiming that stacking constitutes tortious interference with contractual relations,” they wrote.

The lawsuits come on the heels of the International Factoring Association (IFA) ban on merchant cash advance companies, citing tortious interference as the main driver.

After meeting with board members from both associations, the decision was made to deny membership to merchant cash advance businesses. This decision was based on numerous complaints and increased scrutiny that could negatively impact the factoring industry. By distancing ourselves from the merchant cash advance industry, we hope to diminish the chance of potential legislation.

-Commercial Factor July/August 2014

With several merchant cash advance companies left high and dry by the IFA, a potential leadership void has been created.

“As every industry evolves and shapes itself, some sort of governance and guidance is always needed,” said Otar. “This guidance is something that NAMAA holds itself responsible for,” he argued.

“The question is, can they reestablish themselves as a powerful voice that demands respect?” asked an industry veteran on the condition of anonymity.

Goldin assured me that the updated version of the organization’s best practices guide will be a public document.

Industry brokers like Otar are eager to comply with an established code of conduct and play any role they can in its creation. “Most of the business driven industry-wide is brought in through various ISO channels, which are the ones responsible in presenting the product offered by the funders to the end client,” he said.

That enthusiasm may be resonating with the SBFA. Goldin communicated that they are working towards different types of memberships, hinting at the possibility that brokers might one day be extended an invitation to join.

“We are exploring different levels of membership / pricing,” Goldin wrote in an email.

For the right price, they will likely find a lot of eager applicants.

Year of the Broker

April 4, 2015 Many of the newcomers are fleeing hard times in the mortgage or payday loan businesses. Others are abandoning jobs selling insurance, car warranties or search-engine optimization.

Many of the newcomers are fleeing hard times in the mortgage or payday loan businesses. Others are abandoning jobs selling insurance, car warranties or search-engine optimization.

“You have wandering souls trying to find their place in this industry, whether it be as a company or on their own,” said Amanda Kingsley, CEO of Sendto, a Florida-based company that assists new brokers.

Though exact counts appear difficult to obtain, Kingsley professed amazement at the volume of new entrants. “I’m swamped,” she said. “It’s crazy.”

Some of the new brokers discovered alternative financing in December, when OnDeck Capital’s initial public stock offering raised $200 million and valued the company at $1.3 billion. The Lending Club IPO that raised $1 billion the same month also raised public awareness of alternative loans.

Mesmerized with those whopping figures, salespeople from other businesses began committing themselves to a new career in alternative finance. In a business with virtually no barriers to entry, it’s easy to get started. To call themselves brokers, they just need a phone, someplace to sit and a list of leads they can buy online.

Virtually all of the entrants are pursuing dreams of lucrative paydays. Many even expect to make a fast buck with minimum effort.

If only it were that simple. Too often, the untutored new players are making mistakes simply because they don’t know any better, industry veterans maintained.

“A lot of people think you can just walk in and be successful,” said the sales manager of an established New York-based brokerage who asked for anonymity. “They don’t know what it takes to run a company. They don’t know what it takes to get a deal done.”

Worst of all – either unknowingly or with evil intent – new brokers are stacking deals. In other words, inexperienced salespeople pile second or third loans or advances on top of original positions. It’s an approach that clearly violates the industry’s standards, observers agreed.

In fact, virtually all contracts for a first loan or advance prohibit the merchant from taking on another similar obligation, noted Paul Rianda, an Irvine, Calif.-based attorney who specializes in payments and financing.

“I can’t remember one agreement I’ve seen that didn’t have that provision in it,” Rianda said.

Violating that stipulation could provide grounds for a lawsuit, and litigation is underway, according to David Goldin, president and CEO of New York-based AmeriMerchant and president of the North American Merchant Advance Association (NAMAA).

Bigger funders would sue smaller funders because the latter appear more likely to take on riskier, more problematic multiple-position deals, said Jared Weitz, CEO at United Capital Source LLC, a New York-based broker.

Plaintiffs have a case to make because stacking harms the broker and funder of the first position by increasing the risk that the merchant won’t meet the resulting financial obligations, Weitz said. “The guys going out 18 and 24 months to make this a more bankable product are being hurt by the people coming in and stacking those three-month high-rate loans,” he noted.

Deducting fees for more than one advance also impedes cash flow, adding another risk factor, Weitz said.

To further complicate matters, the company offering the second or even third deal sometimes moves the merchant’s transaction services to another processor, Rianda said. That forces the firms that made the first advance to approach the new processor to stake a claim to card receipts, he noted.

So the companies with the original deal suffer from the effects of stacking, but the practice’s shortcomings will haunt the stackers, too, observers maintained.

“It’s not a model that’s going to allow them to succeed,” a broker who asked to remain anonymous said of stackers’ long-term prospects.

Many hardly give a thought to staying power, according to Weitz. “A lot of people entering this space think it’s about fast money and not longevity,” he said.

Longevity requires that brokers build relationships with merchants, a process stacking undermines because too much credit can drive merchants out of business or merely prop up merchants already doomed to fail, sources said.

Yet stacking has become so widespread that it constitutes a business plan for some brokerage shops, said a broker who asked that his name and company not appear in the article.

It can begin when brokers buy lists of Uniform Commercial Code filings to find out what merchants have already taken out term loans or advances, said Zach Ramirez, vice president of sales and operations at Orange, Calif.- based Core Financial Inc.

The brokers then contact those merchants, many of whom are already over-extended financially, to offer additional credit or advances, Ramirez said.

Inexperienced brokers often resort to stacking because they don’t know how to generate leads that can bring alternative lending vehicles to merchants who weren’t aware of them.

Referrals from accountants or other business owners who deal with merchants can provide some of those greenfield prospects, Ramirez noted.

And leads aren’t the only area of cluelessness among newcomers, a broker who requested anonymity maintained.

And leads aren’t the only area of cluelessness among newcomers, a broker who requested anonymity maintained.

“They don’t know why a bank declines a deal or approves a deal,” he said. “They don’t know what’s the basis for a good deal.”

To teach new brokers those basics of alternative business financing, the industry should establish standard policies and technology, according to Kingsley.

A credential, perhaps something similar to the Certified Payments Professional designation created by the Electronic Transactions Association, sources said. To earn the credential, candidates would pass an exam to show they’ve mastered the basics of the business, they proposed.

NAMAA is considering such a credential, said Goldin, the trade group’s president. It’s the kind of self-regulation that could forestall federal oversight, industry sources agreed.

But that might not matter, according to Tom McGovern, a vice president at Cypress Associates LLC, a New York-based advisory firm that raises capital for alternative lenders and merchant cash advance companies.

After all, McGovern noted, Barney Frank, former Democratic U.S. representative from Massachusetts and co-author of the Dodd-Frank Wall Street Reform and Consumer Protection Act, has gone on record as saying that piece of legislation focuses on consumers and does not govern business-to-business dealings like loans or advances to merchants.

That lack of regulation over B2B deals seems likely to continue, “especially in the world we’re in now with a Republican Congress,” said a broker who asked to remain nameless.

However, some members of the industry would welcome federal regulation as a way of barring incompetent or unscrupulous brokers. An agency patterned after the Financial Industry Regulatory Authority, know as FINRA, could do the job, suggested a broker who requested anonymity.

Whether a government regulator or an industry- supported association should police the market, problems could remain stubbornly in place, some said.

Many doubt an association could build the consensus required for united action on some issues – stacking in particular.

For one thing, cleaning up the business could reduce profits for brokerages that profit from stacking, noted a broker who asked that his name not appear in the article.

“Everybody wants to make money,” he said. “Everybody’s out for themselves.”

Another barrier to agreement arises because some brokerages fear cooperation could expose their trade secrets, said Sendto’s Kingsley.

Moreover, unscrupulous brokers want to keep their employees uninformed of the industry’s potential for big profits, Kingsley said. That way they suppress compensation for an underclass of prequalifiers who work the early stages of deals, she noted.

Prequalifiers earn from $150 to $500 a week, depending upon the location, and don’t qualify for benefits like health insurance, Kingsley said. Once they realize what a tiny portion of the profits they’re receiving, brokers terminate the prequalifiers and many go on to become brokers themselves, she observed.

Closers who take over from prequalifiers to wrap up the sale can earn up to 50% or occasionally even 60% of a brokerage house’s commission – if the closer originates the deal and sees it through to completion unassisted, Kingsley said.

Eventually, closers realize they could keep all of the commission if they strike out on their own and become brokers, she noted.

In a way, the progression from prequalifier to broker or closer represents a market correction. And many seasoned industry participants believe market forces will also work out other problems the influx of new brokers is causing.

A large number of the new brokers simply won’t last long because they don’t understand the industry, they’re stacking deals and they’re signing up merchants that won’t stay in business.

Meanwhile, funders are beginning to perform background checks on brokers to make sure they’re dealing with reputable people, sources said.

Some funders protect themselves by simply declining to do business with new brokers, according to observers.

And many new brokers are learning the industry with the help of experienced brokerages that act as mentors and conduits and call themselves super brokers, super ISOs, broker consultants or syndicators.

“So what I’m saying is, ‘Guys, let’s not compete. Let’s grow parallel together,’ ” Weitz said of United Capital Source’s relationships with new brokers. The company began working with new brokers in October 2014.

In such relationships new brokers get advice from the more seasoned brokers. The older brokers can also provide the newcomers with services that include accounting, marketing and reporting, he said.

New brokers can also benefit from the customer relationship management platform that United Capital Source developed, Weitz said.

The new brokers also capitalize on the older brokers’ relationships with funders. Established brokers have earned better rates and terms because of reputation and volume, Weitz noted. Companies like his also know which lenders work more quickly and thus capture more deals, he added.

Older brokers can also steer new brokers away from newer funders that offer shorter terms and demand higher rates, Weitz said. Of the 30 to 40 companies that call themselves funders, only eight or 10 deserve the name, he contended.

The less-respectable funders place only a small amount of money in a few deals, he said.

Newer brokers become aware of their need for help from more experienced brokers when they see how many sales they’re failing to close, Weitz said.

The new brokers also come to realize that the puzzle of running a brokerage office has a lot more pieces than they may have thought, said Kingsley.

The new brokers also come to realize that the puzzle of running a brokerage office has a lot more pieces than they may have thought, said Kingsley.

The percentage of the commission that the older broker charges can vary, according to Weitz.

“If someone needs a lot of hand holding and a lot more resources, they would get a different structure,” he said.

While Weitz said his company plans to acquire only about 10% of its volume through new brokers, Sendto specializes in helping newcomers. Sendto’s Kingsley described the company as “a turnkey solution that provides training and placement of deals. It’s for new brokers or sales offices that do not have what they need to be part of this industry.”

There’s room for entrants because not all merchants know about alternative business financing, said McGovern.

The market can even seem like it doesn’t have enough brokers in the estimation of experienced players skillful enough to find the many merchants who haven’t been introduced to the industry, said Ramirez of Core Financial.

And the big banks don’t really want the business because the deals aren’t big enough to interest them, McGovern said.

But the potential profits look promising to outsiders disillusioned with sales jobs in other industries.

Some experienced brokers even prefer to hire salespeople from outside the alternative financing industry, noted Kingsley. That way, they avoid employees who have picked up bad habits at other brokerage houses, she said.

Long-time members of the industry sometimes enjoy belittling new entrants who can seem clueless about the business they’re trying to master, noted Ramirez of Core Financial. But he recalled the time not so long ago that he himself had a lot to learn.

And regardless of how unsophisticated they may seem, new players have a role, McGovern said.

“They are performing a service,” he maintained. “They’re like the missionaries of the industry going out to untapped areas of the market – of which there are many – and drumming up business.”

To Kingsley, brokers in general – old and new – are beginning to earn the respect they deserve.

“A lot of people are afraid of the word ‘broker,’ ” she said. “I feel that 2015 is the year of the broker, and people should embrace what a broker can actually do. It’s a great thing.”

Industry Fun Leads to Charity Funds

January 15, 20142013’s alternative business financing fantasy football competition came to a close near the end of the regular NFL season. There were some tough matchups and upsets, but two Florida based companies pulled through to win it all. The league raised a total of $9,000 from its participants and as per the rules, must be donated in equal halves to non-profit organizations selected by the two winners.

Financial Advantage Group selected the Spring of Tampa Bay, a noble choice since their mission is to prevent domestic violence, protect victims and promote change in lives, families and communities. DailyFunder, the trustee of the competition reached out to the organization late last month and made the donation in a low-key manner as per their request. They did express their gratitude to Scott Williams of Financial Advantage Group on their facebook page however:

Business Financial Services selected Wounded Warrior Project. They wrote their own post about the organization and why they are proud to support that cause on their website here: http://www.businessfinancialservices.com/blog/fantasy-football-for-charity/

Wounded Warrior Project accepted their donation with some pizazz, holding a giant check for a photo-op at the organization’s Jacksonville, FL office.

—-

I personally would like to thank Heather Francis of Merchant Cash Group for being a great competition co-host this year as well all of the participants that contributed funds to make these donations possible:

- Merchant Cash Group

- Benchmark Merchant Solutions

- Yellowstone Capital

- Raharney Capital

- Strategic Funding Source

- Sure Payment Solutions

- Pearl Capital

- United Capital Source

- NVMS

- Entrust Merchant Solutions

- Financial Advantage Group

- Snap Advances

- Business Financial Services

- Integrity Payment Systems

- DailyFunder

- Capital Stack

I’m already looking forward to next season!

Merchant Cash Advance Industry is Busy at Work

May 16, 2013 After what was one of the wildest two weeks in Merchant (MCA) history, the game-changing news finally subsided, but no one is taking a deep breath. Instead, everyone is busy working their butts off trying to help small businesses grow.

After what was one of the wildest two weeks in Merchant (MCA) history, the game-changing news finally subsided, but no one is taking a deep breath. Instead, everyone is busy working their butts off trying to help small businesses grow.

UPDATE 5/16: RapidAdvance has acquired the operating assets of ProMAC. First Instance of consolidation that we’ve been predicting would happen this year. See news release detailing the acquisition HERE.

There is just loads of capital available right now and the technology is catching up quick to support the mass deployment of it. A writer for the American Banker believes that the MCA industry is even beginning to threaten community banks.

Many community bankers would be open to using online applications and other technological tools to make faster loan decisions, says Trey Maust, co-president and chief executive at the $121 million-asset Lewis & Clark Bank in Oregon City, Ore. But most community banks use a business model that requires more hands-on interaction with borrowers, he says.

Hands-on is another term for driving back and forth to the bank for appointments, having the bankers visit your business, all the while they try to sign you up for other bank products, like checking accounts that incur a monthly fee.

Who’s at Work

We know some of the major industry players but it’s interesting to see who else is doing significantly large volume. Pearl Capital recently reported funding $7 million in a single month and United Capital source came in at a tad shy of $4 million in just this past April. These are firms you may have heard of already, but they’re now sitting at the big kids table.

What the Generals are Saying

If you haven’t been paying attention to the DailyFunder.com forum, 4 Chief Executives have contributed to the site in a very meaningful way by sharing their thoughts on the MCA industry at large. This is the kind of wisdom you would normally get in bits and pieces through occasional citation in the Green Sheet or other publications, but the full monty has materialized in the very exclusive CEO Corner. Some key highlights from what they’ve shared so far:

Excerpts from Jeremy Brown, CEO of RapidAdvance:

Those of us that have been in this business for 5 years or more – Rapid started in 2005 – are excited at the positive press we get today vs. several years ago and how we are becoming embraced and accepted as a mainstream product. More PE firms, banks, and others want to invest in or lend to the industry. Those groups have always been intrigued by the returns in this industry but the conversations are different today.One thing I think will be different next year are fewer deals offered over 12 months in payback period. When you look at the data over an extended period of time, 18 month term loans don’t make sense for the merchants that are funded. It’s not the most efficient use of funds, limits the ability for the merchant to renew and the longer term deals are far riskier. (See: Year in Review and What Next Year May Bring)

Isn’t that the point of a 6 month MCA – to meet a current need and have the merchant be able to draw again in 4-6 months for the next capital need? That is the problem with the 15 – 24 month deals that are being offered to merchants today. Our industry is based on providing working capital to merchants. By its very definition, working capital is less than 12 months. Longer term deals are permanent capital, even when they are repaid over 15-24 months.it was no surprise when the economy tanked in late 2008 that the merchants in our portfolios at that time took a major hit to sales and therefore the funding companies losses increased by 50% or more on their outstanding portfolios. So what happens when the next recession – big or small – hits and funders have portfolios out to 24 months? It doesn’t take an MBA from Harvard to figure out that answer. (See: Working Capital or Permanent Capital

Haven’t gotten into the industry myself in 2006, I can totally validate the complete 180 in press coverage. I’ve put all my energy into MCA and it’s gratifying to finally hear the praises so many years later.

Excerpts from Steve Sheinbaum, CEO of Merchant Cash and Capital:

The industry already services hundreds of thousands of small business merchants with cash advances for growth and other purposes based upon monthly credit card receipts. For years this has been the basic model of operation. But, what about the substantial number of businesses that require quick and easy access to capital who don’t accept credit cards or don’t produce enough in monthly credit card receipts to qualify under the normal MCA guidelines? Tens of thousands of businesses could use the capital infusions the industry provides daily but either don’t think they’ll qualify or, because of our lack of creativity, the industry hasn’t produced a means of addressing their needs. These businesses would make great customers but because of the rigid requirements we have in place to protect our livelihoods we’ve left money on the proverbial table.That’s not the case anymore. (See: Creativity in the C-Suite…Another way to Fund!)

In regards to advances on gross revenue instead of just credit card payments, he’s absolutely right.

Excerpts from Andy Reiser, CEO of Strategic Funding Source:

the most important part of any deal is the people. We rely heavily on the relationships we have with the client and most importantly with our ISO partners and ISO syndicate partners who invest side by side with us. Valuing these relationships is far more important than relying solely on the numbers and how sophisticated our technology is.Over our 8 year history, we have noticed that the performance of a deal has more to do with the relationship we have with our ISO partner and ISO syndicate partner, then with the deal itself. We have all kinds of tools available to help us analyze the potential success of a deal – FICO scores, due diligence checklists, signed affidavits, warranties and representations, scoring models, algorithms, etc. And yet, some of the ugliest deals on paper have been some of our best performers, while some of the most attractive deals on paper have been nothing but trouble. (See: Business and Baseball Fantasies)

During my time as a head underwriter, I witnessed the exact same thing. Solid referral partners had solid performing clients even if they didn’t look so good on paper. Likewise, the shakier resellers had clients that underperformed across the board, including the deals that looked cleanest.

Excerpts from Craig Hecker, CEO of Rapid Capital Funding

As each MCA company grows and creates a positive reputation, we all grow as an industry…together. But as our popularity grows, however, so does our competition. We already know that Amazon, eBay, and Google are stepping into the market, and AMEX is looking to expand their short term financing portfolio. These big business industry leaders will help build our brand of finance and benefit our portfolios, but I also think it is fundamental that we market ourselves as the alternative to big business finance and identify ourselves with the small business owner. (See: Small Business and How MCA Can Bridge the Gap to Success

We’ve got some big names in the industry now, whether they are financing the merchants directly or backing the funders that do the financing. I agree that you need not be intimidated by competing against these established brand names. Positioning yourself as the funder next door, people that have walked a mile in the merchant’s shoes (literally) can actually be a strong advantage.

What’s Next?

We’re pretty confident there will be more big headlines in the near future but for now we can’t confirm or say anything. DailyFunder.com is also lining up additional industry captains to participate in the CEO Corner and I’m sure there will be plenty of nuggets for us all to dissect. They’re probably the best source of MCA information that you can possibly get.

Stay tuned.

– Merchant Processing Resource

../../

MPR.mobi on iPhone, iPad, and Android

Fantasy Football Championship Begins Tomorrow

December 19, 2012 The MCA Industry Fantasy football league is finally drawing to a close. If you somehow missed the action this season, twelve companies came together to compete for a grand prize donation to a charity of their choice. Each company, in addition to several non-participants pledged funds to the prize. A total of $7,100 was raised!!!

The MCA Industry Fantasy football league is finally drawing to a close. If you somehow missed the action this season, twelve companies came together to compete for a grand prize donation to a charity of their choice. Each company, in addition to several non-participants pledged funds to the prize. A total of $7,100 was raised!!!

In a winner-take-all format, the two teams competing in the championship this week are:

TakeCharge Capital – Newington, CT

Sure Payment Solutions – New York, NY

A winner will be declared next week. A big thanks to everyone that contributed. 100% of the funds will be donated to the winning team’s charity selection.

- Rapid Capital Funding – $1,000!

- Raharney Capital – $500

- Financial Advantage Group – $500

- Merchant Cash Group – $500

- Sure Payment Solutions – $500

- Meridian Leads – $500

- Merchant Cash and Capital – $500

- NVMS – $500

- United Capital Source – $500

- RapidAdvance – $500

- Capital Stack – $500

- Swift Capital – $250

- Strategic Funding Source – $250

- Entrust Merchant Funding – $250

- Paramount Merchant Funding – $250

- TakeCharge Capital – $100

– Merchant Processing Resource

../../