How Funders Survived PPP and a Year of Covid

May 4, 2021 A year into the pandemic and from the AltFinanceDaily office in Brooklyn, it looks like the world is opening up again.

A year into the pandemic and from the AltFinanceDaily office in Brooklyn, it looks like the world is opening up again.

After a year of Zoom and LinkedIn networking, those in the industry lucky or talented enough to have survived can still complain without restraint about big government lockdowns and misguided legislation. Competing with Uncle Sam’s deep PPP pockets have slowed deals down, and with a new fund opening this week for restaurants, it might be more of the same.

But two funders said that though there is an initial slowdown when a new stimulus is rolled out, the programs have still been vital for business– and if firms kept up with contacts, the business could be booming even after the pandemic.

CEO David Leibowitz of San Diego-based Mulligan Funding said that his firm survived the worst of the shutdown. That was due in no small part to government programs that kept merchants in business.

“People forget where we were sitting in April, May last year, 20 million people filed for unemployment. The segments of the market that we serve in general don’t have more than 30 days of cash on hand at any time,” Leibowitz said. “There’s no chance that our market survives that without the level of government support that they’ve been given.”

Sure, there’s a dampening effect at first, but there wouldn’t be B2B without businesses to fund. Leibowitz said he thinks the macroeconomic effects of printing money will have consequences in the long term, but it’s the lesser of two evils.

Matthew Washington, the well-known CRO of PIRS Capital, has also been vocal about PPP. Like Liebowitz, he said it has its pros and cons, creating a slowdown and demand for capital in one stroke. In his experience, because the stimulus was limited to payroll and rent, merchants were hungry for other products.

“They’re only able to allocate it for certain things, payroll, and hiring people, right,” Washington said. “Our funding allows them to be able to use capital for other opportunities, like buying supplies, buying inventory. Although it’s kind of been somewhat slow, they need to have other working capital needs to be provided for.”

Washington also said some merchants used their PPP funds as low-interest loans, paying off and refinancing advances. PIRS has succeeded through the pandemic due to its relationship-based model.

“It’s all about keeping in touch with your merchants during this time, having a big pulse with the people you do business with,” Washington said. “We’re really a lean and mean company, we kind of have the community bank approach to this space; we’re more relationship-based.”

PIRS had only paused for 60 days and was lucky enough to be set up with recurring merchant partners that turned out to be essential businesses.

“We were very blessed; a lot of our portfolio was operating during the shutdown,” Washington said. “Our portfolio did very well for the circumstance.”

That was how they survived, a lot of good faith and hard work, but pinches of luck as well. Leibowitz said that contrary to popular belief, many good people lost their business during the pandemic. It wasn’t just bad actors and funders with terrible underwriting.

“In March, we had customers who, for reasons totally beyond their control, couldn’t pay. And we weren’t sure in March, how long that would go on for, we weren’t sure how bad it would get,” Leibowitz said. “If you’d asked me in March, April, were we going to survive this thing. There’s no way I would have been able to give you a confident answer.”

Some with public securitizations, well-run businesses, dropped out and disappeared. Leibowitz said Mulligan was able to keep every employee on staff and got through the “sh*t show.” In part, it was with help from competitors who specialized in PPP funding that Leibowitz said his firm was still going strong.

“So I think for all of its shortcomings, I have a world of respect for the SBA and the program. I think of Brock and guys at Lendio, I think of the guys at BlueVine and Kabbage, who really have done a truly extraordinary job of distributing that product to our target market,” Leibowitz said. “And I’m sitting here today, unquestionably, enjoying the benefit.”

So PPP helped, despite the slowdowns, in the short term, and Liebowitz said in the long term, the government overspending might get hairy. But with talk about the world opening back up, with bars open down the block for the first time in a year, what does Washington think about the near future?

The world just isn’t going to stop; it’s just evolving with the new temp of what’s going on; I think there’s a lot of positive things on the horizon for our business,” Washington said. “Once the vaccine rates, and everyone’s ‘cured’ how are they not going to open up.”

At Least One Firm is Leaving New York before Disclosure Law Lands

April 29, 2021 New York MCA firms are in the dark. In January, the governor delayed implementation of the APR disclosure bill until 2022. But the bill leaves it to the Department of Financial Services (DFS) to finalize how it will all work and not everyone is confident the outcome will be positive for business in New York State.

New York MCA firms are in the dark. In January, the governor delayed implementation of the APR disclosure bill until 2022. But the bill leaves it to the Department of Financial Services (DFS) to finalize how it will all work and not everyone is confident the outcome will be positive for business in New York State.

For example, Greenwich Capital, a small business funding company, has decided to move from Manhattan to Hoboken, NJ in preparation for the law. They anticipate that the cost of compliance will be high enough to warrant a trip on the PATH starting now rather than when it may be too late to contemplate later.

“There’s a lot of ambiguity, and our five-year lease was up,” Rich Gipstein, General Counsel at Greenwich Capital, said. “We’ll be moving to Hoboken for the time being and see what’s going on with this law. But in the meantime, it’s a lot cheaper for us.”

Based on vague wording language like double-dipping, Gipstein said there is no clear way to tell who or what the law aims to regulate. At least for his firm, it’s better to sit this one out.

“I think there’s quite a lot left open, and it’s intended to be broad,” Gipstein said. “There won’t necessarily be much time to know what the law means until it’s effective. I think there will probably be some lead time, but likely not quite enough for most businesses in the industry to adapt.”

For example: when does a deal become a “specific offer” and come under the purview of the law? In an industry where deals are won through cold calling, social media blitzes, and emails, when would it become necessary to disclose an APR? In a DM on LinkedIn? Rich said it is unclear what a “provider” is, whether it be funders, brokers, or ISOs. In the bill, a provider is required to make commercial financing disclosure clear and let a recipient know at the time of the “specific offer” the all-inclusive rates of a product. Without clarity, it’s hard to predict what the cost of compliance will be.

For example: when does a deal become a “specific offer” and come under the purview of the law? In an industry where deals are won through cold calling, social media blitzes, and emails, when would it become necessary to disclose an APR? In a DM on LinkedIn? Rich said it is unclear what a “provider” is, whether it be funders, brokers, or ISOs. In the bill, a provider is required to make commercial financing disclosure clear and let a recipient know at the time of the “specific offer” the all-inclusive rates of a product. Without clarity, it’s hard to predict what the cost of compliance will be.

“I think, from my reading of it and from my understanding of New York’s position, it would seem that they are trying to regulate both funders and brokers under the same regulation,” Gipstein said. “I think it’s possible that the legislature intentionally left some things vague for DFS to fill in. The law basically says, ‘there’ll be regulations that will make this make sense.'”

Gipstein said it’s common for politicians to leave it to the regulators to finish the job, after all, the DFS has its nose to the grindstone in the day-to-day. But when a law affects an entire industry like this, Gipstein said it is uncommon for changes to be left until the last moment.

“It’s more than just disclosure requirements; this is not similar to what California did,” Gipstein said. “The law also dictates how to calculate the projected sales volume. You’re required to either use the historical method, in which you must always use the same number of months leading up to the deal, or you can opt-out and use your own projection. But if you use your own projection, that opens you up to disclose the results of all your deals to the government… It’s almost like an annual audit.”

The historic method doesn’t really work, Rich said when the industry comprises atypical merchants who wouldn’t be looking for funding if traditional methods could predict their sales volume. When it comes to self-declaring and letting the government poke around: Gipstein said the way a funder evaluates deals is proprietary. It’s what sets them apart; it’s the value proposition.

Greenwich Capital isn’t alone in their assessment. The Small Business Finance Association (SBFA), a trade group comprised of similar financial companies, has also been vocal about the law’s perceived shortcomings.

Greenwich Capital isn’t alone in their assessment. The Small Business Finance Association (SBFA), a trade group comprised of similar financial companies, has also been vocal about the law’s perceived shortcomings.

“You have a group of companies that are pushing these types of disclosures, for no reason other than their own self-interest,” said Steve Denis, executive director of the SBFA, back in October. “We’re fine with disclosure, we are all for transparency, but it needs to be done in a way that we believe is meaningful to small business owners.”

Denis had further said that those firms taking credit for writing the laws are the same companies that will end up suffering under the strict tolerance of an APR rule.

“The companies pushing this, the trade associations pushing it, they like to take credit for writing the bill in California and writing the bill in New York: I don’t even think they’ve read it,” Denis said at the time. “It’s going to subject their own members to potentially millions if not hundreds of millions of dollars in potential liability [fines.]”

When the DFS finalizes the terms, it will likely make dealing with disclosure too costly to remain in New York State, Gipstein said.

Gipstein said we’ll have to wait and see if NY-based brokers will have to go through extra compliance even if their funders or merchants are out of state. The worst-fear scenario is a possibility that after New Years’ 2022, out-of-state funders will stop working with NY brokers entirely, just because they live in NY. Merchants in the state, subject to the law, may find commercial finance a barren marketplace.

“We’ve got a lot of different things to manage as we grow, and one of the things we don’t want to do is create is a large compliance department,” Gipstein said. “It’s just cheaper for us, after doing a cost-benefit analysis, to move to a different state. We’re probably not going to be a New York funder by 2022.”

Selling Finance Door-to-Door During Covid

April 9, 2021 This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

“We just went back into lockdown. The whole province, everything just shut down,” CEO Patrick Labreche said. “We were getting 20 to 30 new cases a day, and then it jumped to like 200 a day.”

Meanwhile, 110 miles down south at AltFinanceDaily, de Blasio announced NYC public beaches would be opening up by Memorial Day. Because of the wide range of government shutdowns this past year, Labreche said it is hard to admit to some that his business is booming.

“I was having a conversation with a guy who does payment processing, he makes residuals on his customers, and so his book of business was not making any money right now; he’s hurting,” Labreche said. “So it’s kind of hard to tell a guy like that that we’re flourishing, and maybe you should come work with us.”

Labreche said that the processor was actually going to work with Canadian Financial. Success this past year came from leveraging the interpersonal skills that make an excellent door-to-door salesperson thrive, Labreche said.

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

With a team of salespeople connected through weekly department meetings and messaging groups to keep the energy up, the deals kept rolling in throughout covid. Labreche said his firm is set apart from a good portion of Canadian alt finance: they offer a smorgasbord of financial products directly to the borrower instead of using lead generators.

While most fintechs think all business owners want a one-button final product, Labreche attests to the opposite- his firm sends out salespeople to make sure businesses know they have a rep to rely on.

“I have nothing bad to say about aggregators; that’s their business model, not ours,” Labreche said. “Our business model is going into a business that didn’t even know that the solution was available. When you’re looking online, you’re looking for a solution that you already know is available.”

Labreche favors traditional finance. His firm offers MCAs and other alternative forms of funding but said those are mostly band-aid solutions and he regularly sees MCA deals taking advantage of merchants. For example, Labreche said he walked into an ESCO gas station last month, and through talking to the owner, discovered an opportunity. The owner had taken an MCA from a big Canadian firm but was confused about the cost of capital- he thought he was paying 17%, but Labreche read a recent statement and discovered the rate was really 50%.

“Right there and then he was like, ‘oh my God, that’s crazy I didn’t know,’ he was misled, and it’s like that across the board. So I ended up getting him a quarter-million dollars at four and a half percent on a term loan,” Labreche said. “Nobody’s ever walked into his business or called him, offering him traditional money. We feel like there’s a huge underserved, undereducated market.”

This week, walk-ins have become less of a possibility, with a lockdown banning all non-essential travel. Still, business development manager Julian Hulan looked forward to when things would open back up. He had masked up and gone out on sales calls throughout the year when the government wasn’t in shutdown mode. Recently he traveled to 20 car dealerships to offer financing in a two-day period and said he found merchants excited to see him in person instead of over email.

“They were like ‘oh, I can actually sit down and talk to this guy?’ and that’s when they eat it up,” Hulan said. “They know because they’ve already made that connection face to face, they can call me directly. We don’t do this whole 1-800 Number. You’re going to call me directly and if I don’t answer, you leave me a voicemail, I call you back, it’s that personal relationship between me and that client.”

Why Funders Are Investing in Real Estate As Their Side Hustle of Choice

January 25, 2021

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

At that point, Ribeiro’s fledgling company still wasn’t generating much revenue. “I thought, ‘Man, I just can’t get a lot of loans done right now. I only have three or four employees.’ That’s how I got into the real estate industry.” Twelve years later and at the height of a global pandemic, Ribeiro is simultaneously running two thriving ventures —US Business Funding, and a portfolio of hundreds of rental properties he now owns.

At a time when fintech startups and other industry innovators are looking for investors, alternative lending execs like Ribeiro are instead choosing to put their money in real estate to beef up their investment portfolios. Although some execs shy away from talking publicly about their real estate dealings, citing the fact that they don’t want too much exposure, the consensus is that there’s a lot of money to be made in buying, selling and renting property – if you know what you’re doing.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

To Ribeiro, real estate offers a few major advantages: It’s a tangible asset. You can leverage it as it appreciates in value. Deductions make it so you pay very little in taxes. And it offers significant cash flow. “It’s the best investment you can make,” he says.

What makes real estate an especially good fit for alternative lending and fintech execs is that they possess the skills, resources and financial literacy to succeed at it.

“Real estate is a long-term gain,” Ribeiro says. “The industry we’re in is a cash-flow cow. People who are doing well are printing money. But what can you do with that money? You can put it in the stock market, but you won’t control much. Then you pay capital gains on it.”

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

“If you’re a cash advance guy and COVID happened, then you’re not doing very well,” he says. “If you diversified your assets by doing real estate and cash advance, you’re able to weather these downturns a lot more easily than you would otherwise.”

Rianda has not yet counseled any of his own cash advance clients on real estate matters. But based on his insights from working with both areas, he says real estate would be a logical move for MCA executives, and he’s seen some of his clients in the bankcard industry buy up properties.

“One of my clients had a portfolio of merchants and sold it for a few million, then flipped over to real estate. So it’s a means (to an end),” Rianda says.

‘Snowball effect’

Ribeiro has relied on a simple strategy to steadily build his portfolio of residential properties: Buy. Fix. Leverage. Repeat.

“I feel like the portfolio is doubling every couple of years. It’s just a snowball effect,” he says.

After Ribeiro buys a home, he waits about six months before he has it appraised and fixes it up in the meantime.

“If you go to the bank within the first six months of purchasing it, they’re going to give you the actual market value of whatever you purchased the house for,” he says. “If you wait six months, they’ll reappraise the home and give its true market value, which could be another 40, 50 or 60 percent. And so now you’re going to have a lot more equity in the house, and you’re going to get a lot more money when you leverage that home to go buy the next one.”

Ribeiro says he sees lots of people making the mistake of buying a home, and then going to the bank a week or two later for a loan.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Depreciation refers to one of the key tax benefits of real estate. Since owning a rental property is technically a type of business because it generates income, the property is considered a business asset. The IRS allows you to deduct the cost of acquiring that asset – the property – over the span of its useful life. For residential properties, the IRS sets a standard depreciation period of 27.5 years.

So if you buy a $100,000 property with a $20,000 land value, $80,000 of the asset is considered depreciable. Over the course of 27.5 years, you can take an annual deduction of just over $2,900 a year.

The trick, Ribeiro says, is to stick to lower-priced properties with an 80/20 home-to-land value. Most of his properties are single- and multifamily homes between southern California and Las Vegas.

Like Ribeiro, Rianda’s investor clients concentrate on one geographic area to find the best properties. “They look at the area for a long time, understand the area,” he says. “In my neighborhood, three blocks can make a 50 percent difference in the price of a house. You need to focus on a particular geographic area and do a lot of transactions in it.”

Small portfolio, big impact

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

“For me, it’s just a really good second income stream and a way to have a secure return of 4.5% to 6.5% a year,” he says.

Growing up, Weitz got a feel for real estate by watching his uncles invest in multifamily properties. At one point, Weitz’s uncle owned 15 different multifamily homes, and Weitz would help do the maintenance on them.

Eight years ago, Weitz invested in his first two-family home and has fixed and flipped eight properties since then. He currently owns two two-family homes and invests primarily in multifamily homes in Long Island, Brooklyn and Queens. Over the next five years, he plans to pick up at least two more four- or eight-family properties. Working with a small portfolio of residences in his home state has allowed Weitz to have full control over managing his properties and to turn a good profit.

“I think for me, it just offers more liquidity,” he says. “It’s an asset I can sell and liquidate at any time. That’s really important for me.”

Ideally, Weitz would like for his investment to build generational wealth that he can pass down to his son. With many people in the U.S. unable to qualify for mortgages, Weitz sees real estate investing as an opportunity to help the economy by giving renters a place to live and put down roots. “Depending on the neighborhood, you can put yourself in a situation where you have good renters for 20 to 30 years. They want to raise their families and have their kids grow up there,” he says.

Litigation among the pitfalls

Even though Ribeiro has had success with his business model, he cautions that there’s considerable risk involved with real estate.

“I love the industry. It’s a passion. It’s beyond my wildest dreams of the size of the portfolio and how well it performs,” he says. “But don’t think it’s all cupcakes and unicorns. There’s a lot to the madness. That’s why not everyone can replicate the model.”

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

As an attorney, Rianda says his real estate clients call on him not just for the purchase of the property, but for various issues that occur during the ownership period.

Here’s one scenario: A property owner has a tenant who isn’t paying rent, so the property owner sues the tenant. But while the lawsuit proceedings are under way, the tenant declares bankruptcy, which puts a stall on further litigation.

“There are people who understand the system and can make it difficult for you to get them out (of the property),” Rianda says, adding that it’s important to have legal counsel readily available. “You need someone who has really done this a lot and knows how the system works to get that person out of the rental property as quickly as possible.”

To minimize liability, Ribeiro has divided his properties into about 10 different business entities – each with a separate umbrella insurance policy.

Rianda sees his own real estate investor clients follow this strategy by grouping multiple homes under the name of an LLC. “If you personally own all these various assets, there’s the potential that if something catastrophic happened at one, it could bleed into all your other properties and potentially put them at risk,” he says.

Dual careers

Ribeiro’s real estate investments and finance company both serve as full-time occupations for him. Some years, he’ll focus more on one area than on the other, depending on market conditions. He spent more time on real estate between 2008 and 2013; then his business needs flip-flopped when real estate prices started going back up. This past year, he’s directed more attention to the finance company because of COVID, which necessitated some operational changes and a need to help clients who had been trying to get PPP loans. But he’s also started investing in commercial real estate, which has taken a hit because of companies forgoing office space to save overhead costs while employees work remotely.

Ribeiro expects to start seeing more mortgage defaults on lower-level homes in 2021 and 2022, after forbearance periods are over. And he’s been leveraging his assets to start buying more properties around the second quarter of the new year. “I think it will be a good time to start buying heavy again,” he says.

An attractive investment vehicle

With the pandemic weakening business portfolios, secondary investment options might sound like just what the doctor ordered.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

“As time goes on, I’m starting to see my clients go back into their lending,” Rianda says.

Even as clients start to recoup their business, Rianda sees the wisdom in other investments and says cash advance executives are well suited for real estate. “It’s just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” Rianda says. “It’s something I find that people who are doing well in their business do, regardless of what business they’re in. So cash advance guys are just following the things people have done for years.”

Ribeiro cautions that people who get into real estate should look at it as a 10-year investment minimum, and not just a two- or three-month stint.

“It’s not a lottery ticket, and it’s not an overnight race,” Ribeiro says. “This is a long-term gain. But it’s a very lucrative gain from a cash-flow perspective and a tax perspective. I don’t think there’s a more attractive vehicle than real estate.”

Immigrating From Cuba With “Nothing in my pockets,” to a CEO Funding $12 Million a Month

December 15, 2020 “Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

“Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

Ebanks started what would become Spartan Capital shortly after seeing an ad calling for startup investors in an industry Ebanks had never heard of, called Merchant Cash Advance.

It was around 2016. Ebanks was up late in the NYU university library, putting himself through an MBA while working as a reactor operator at the Indian Point nuclear power plant in Westchester.

Despite the job security Ebanks enjoyed, he said he wasn’t happy with his career, wasn’t getting the satisfaction he wanted. He had already made it a long way— starting before the millennium as a Cuban immigrant, immigrating to the Dominican Republic in 1998 and then Florida in 2002 with empty pockets. Shortly after arriving, Ebanks enlisted.

“I spent some time in the army; I wanted to put in some time,” Ebanks said. “I said: ‘I’m a new immigrant, what’s the best thing that I could do to reward these opportunities?’ To serve in the army, give the country a couple years, and payback in advance for this opportunity that I knew I was going to have.”

Ebanks said he learned early on to take every opportunity seriously. He served for two years and then became an engineer and contractor for the army, working on the Patriot Missile defense system. He went through college at NJIT, graduating in 2009, and following in his father’s footsteps to become an electrical engineer.

After working with South Jerseys PSE&G, Ebanks took the opportunity to work full time shifts at the the nuclear power plant, and by 2016 he was pursuing an MBA and looking for ways to grow what he called “my empire.” Used to investing in small businesses already, discovering MCA fit right within his world.

“I’ve always been active, throughout my professional career I had businesses in real estate, I owned several businesses such as laundromats, a lot of retail cell phone stores and things like that,” Ebanks said. “So at one or two am in the morning, I’m working on how to build my empire. I was on Craigslist looking for opportunities, seeing what’s out there, and somebody wanted an investment, to partner up and start a company in a new industry.”

He took a meeting and learned a ton. Although he did not end up going into business with that person, he was hooked on the concept.

“I looked at that ad, and $10,000 later, we had a company,” Ebanks said.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

“I did some research, opened an office in New Jersey, secured a manager to run the operation, and we started brokering deals and learning about syndication.”

He worked with SFS Capital, now called Kapitus. He fell in love with the immediate gratification feedback of making deals, seeing returns on account receivables, and watching renewals come in. The business grew, but things were not always a straight climb to success.

“There was a point where things were not going well and I had to start a new company, find new parters and investors with a funding direct-only focus, and moved into my basement- my wife was unhappy with that. I started hiring people, processors, underwriters, and ISO managers in my basement,” Ebanks said. “At one point, she said, ‘Okay, this is enough. Ten strangers are coming into my house every day, you’ve got to get an office,’ so we secured an office in New York. And that’s when things took off in 2017.”

At that point, Ebanks had shifted his business model from securing deals to funding them all his own, using capital he raised. Ebanks said that being a broker partnered with Kapitus was great, but he wanted to grow and run his business entirely. The best way to do that was through ISO management, Ebanks said. Ebanks let the direct sales team phase out and he hired ISO managers, learning the ISO business as he went.

“So fast forward now: We have over five ISO managers, and we’re funding about $12 million a month,” Ebanks said. “It’s been a phenomenal journey and the most rewarding thing I’ve ever done in my life; I’m not shy to share how exciting every day is to me, and how other than my family and my kids and God, this is the most important thing my life.”

For brokers looking to get started in the industry, Ebanks has this advice to share: Don’t settle.

“Don’t settle, look for growth, and invest your money,” Ebanks said. “I always invested everything I could, 95%, every penny on the business. It matters especially at the beginning, the more you invest, don’t let it sit.”

That investment should go toward your business, your staff, and hiring. Ebanks said the more you invest, the bigger the bag, the more your firm would grow, and your employees will grow with you. Helping employees will mean they will eventually leave, but in Ebanks’ experience treating employees right creates partners.

“Some of them now are partners, and the employee-employer relationship is always more partnership,” Ebanks said. “Some of them own their own companies now, and we help each other out. If they have a big deal, they say: ‘Frank do you want to take $50,000 out of this deal?’ I say yea I trust you. I’ve known you for years.”

Now that he’s on track to grow with recurring customers, seeing some merchants come back to renew twenty times since 2016, Ebanks sees a possible bright future for Spartan Capital: becoming a chartered online bank.

“It is an alternative lending space but to offer the best products to people,” Ebanks said. “I think at the end of the day, and we need all the resources we can get, the next chapter is to apply and secure an online bank charter, it’s the future of the fintech industry.

“Why do people like doing business with us versus a bank? Some of them can do business with banks, but they choose to use us because they have direct access to us after 6 pm, they could call us Saturday, they can call us on a Sunday,” Ebanks said. “A great relationship that they can never get from a bank. I want to bring what we do in MCA to the banking industry to serve people that want banking products, but I want to give them that MCA experience.”

When The Music Stopped: How The Pandemic Threatened the History and Culture of Austin, Texas

November 15, 2020

In April of this year, Threadgill’s – a legendary Austin music venue and beer joint that, in the 1960s, famously launched the career of blues singer Janis Joplin — turned off the lights and pulled the plug on its sound stage.

A converted gasoline station, Threadgill’s had been a rollicking music scene since 1933 when musician and bootlegger Kenneth Threadgill secured the first liquor license in Texas after Prohibition. His juke box was crammed with Jimmie Rodgers songs and Threadgill himself famously sang and yodeled Rodgers’ tunes.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

“The first time I went to Threadgill’s was in the fall of 1968, when I was a freshman at UT,” recalls Perry Raybuck, a songwriter-folksinger and retired government worker who, as a member of the Southwest Regional Folk Alliance, played the stage in 2018. “It was the beginning of an education for me,” he adds. “I had been a Beatles and rock n’ roll kid and it opened me up to different music styles. I became a convert.”

In 1981, Threadgill’s was taken over by another acclaimed club owner, Eddie Wilson, who previously had been the proprietor of the Armadillo, a fabled music venue. Wilson began to actually pay musicians – Threadgill had compensated them mainly with free cold beer – and installed a circular stage.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

“Live music,” says Laura Huffman, chief executive at the Austin Chamber of Commerce, “is why people come here. It is a central component of Austin’s cultural and economic life.”

Omar Lozano, director of music marketing for Visit Austin, the city’s main tourism organization, says: “We have close to 250 places in the greater Austin region where you can hear live-music, although it’s closer to 50-70 on any given night. During South by Southwest, no stone is left unturned — everything becomes a stage: parking garages, grocery stores, housing co-ops. There are also four or five stages at the Airport, which helps liven up the mood.”

But that identity is being put to the test. So far this year, Austin has lost a raft of live music venues. Among those joining Threadgill’s in honky-tonk heaven since the pandemic struck are Barracuda, Plush, Scratchhouse, Shady Grove, and Botticelli, all of which provided niche audiences to both established musicians and up-and-coming acts.

The roller-coaster ride of government mandated shutdowns followed by a limited re-opening in the spring and another shutdown since July fourth is making life miserable and untenable for both club owners and already hardpressed musicians and artists, says Marcia Ball, a piano player and blues singer.

Ball, who was named by the Texas Legislature as “2018 Texas State Musician” and whose musical style was once described by the Boston Globe as “mixing Louisiana swamp rock and smoldering Texas blues,” told AltFinanceDaily: “There was already a limited amount of opportunity for musicians to perform and monetize their work in Austin, so it has always been necessary to travel to make a living. But we still depend on a thriving local scene, and we’re losing that when key venues like Threadgill’s disappear.”

Adds Graham Williams, a prominent Texas promoter of touring bands: “These venues and bars are vital to the music ecosystem. Local bands and cover bands need hangouts, even if people are not buying tickets. They’re places to play every night of week.”

While unheralded outside the Austin scene, the local music joints were often a port-of-call for out-of-town promoters and nightclub owners checking out Austin talent – “most notably Barracuda (which) had super-popular acts and was like a hipster garage venue,” says promoter Williams. “A lot of touring bands played there on their way up.”

A July study by the Hobby School of Public Affairs at the University of Houston found that the city’s live music industry is in desperate straits. Sixty-two percent of live music spots and 55% of the bar-and-restaurant businesses reported to researchers that that they can endure for no more than four months, making them the most vulnerable of 16 industries surveyed.

And the situation has become “even more ominous” since the report was published, explains Mark P. Jones, a political scientist at Rice University in Houston and a lead researcher on the Hobby study. “That survey finished polling two hours before all bars and restaurants closed back down,” he says. “Everything people were saying was when bars were at 50% capacity. That’s a best-case scenario.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

“He knocked down the rent a little bit,” Severin says of his landlord, but the situation is dire. “We just had a fifth venue, Re bar, close at the end of August,” he says. “It was a punch in the gut. This could be me.”

The Bitter End in Greenwich Village is also keeping its head above water despite not opening its doors since March. The nightclub has a storied past: owner Paul Rizzo recounts that it is where pop singer Neil Diamond got his start and where “everyone from Curtis Mayfield to Randy Newman” has performed since its opening in 1961. But the club is silent now since the pandemic overwhelmed the city’s hospitals and made New York the epicenter of sickness and suffering during the spring. So far the club is getting help from a landlord’s forbearance and loyal musicians.

Peter Yarrow (the “Peter” in the bygone trio Peter, Paul and Mary), donated a streamed concert to patrons who contributed to a fundraiser that raised more than $50,000. And grateful local musicians also put on a benefit directing people to a Go Fund Me page on the Internet that raised another $16,000. “We’re a major venue for local musicians,” Rizzo says. “We should pull through.”

It’s in their self-interest for artists to do whatever they can to keep the doors open at a club like The Bitter End. “These days because of the last two decades of declining record sales — live music is the bread and butter of a musician’s income,” says journalist Edna Gundersen, a recently retired, 28-year-veteran of USA Today. “That’s true whether it’s a local entertainer or an international superstar.” (Gundersen earned the reputation as Bob Dylan’s favorite journalist; it was she who scored his only interview after he won the Nobel Prize for literature in 2018, publishing his eccentric musings in the The Telegraph of London and breaking the news that he would indeed accept the prize.)

“Touring has been crushed,” Gundersen adds, “and festivals have been canceled. So people doing the circuit and clubs are gone for all intents and purposes. Streaming — while initially up — is down because people aren’t listening to music in the gym or in their cars. Physical record sales are also down because people aren’t going to stores. All of this is just killing musicians.”

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

Hoping to win attention and assistance for their plight from the federal government — “We’re the first to close and the last to reopen,” Severin says — live-music entrepreneurs like himself and Rizzo and more than 2,800 club-owners and promoters across the country have banded together to form the National Independent Venue Association.

Their membership includes independent proprietors (no corporate members allowed) of saloons, cabarets and concert halls as well as theaters, opera houses and auditoriums from every state plus the District of Columbia. To help plead their case with Congress, the organization hired powerhouse law firm Akin Gump Strauss Hauer & Feld, the largest Washington, D.C. lobbying firm by revenue.

NIVA also blanketed Congressional offices with two million letters, e mails and correspondence generated from hordes of fans and performers. Among the many scriveners are a slew of boldface names: Mavis Staples, Lady Gaga, Willie Nelson, Billy Joel, Earth Wind & Fire, and Leon Bridges. Comedians Jerry Seinfeld, Jay Leno and Jeff Foxworthy have also penned notes to lawmakers championing NIVA’s cause.

Their message: without federal funding, 90% of independent stages will go under over the next few months. “The heartbreak of watching venues close is that once a building is boarded up, it’s not going to be a music venue any more,” warns Audrey Fix Schaefer, communications director at NIVA. “They operate on thin business margins to begin with and they’re too hard to develop.” For touring acts, each city stage is “an integral part of the music ecosystem,” Schaefer explains. “When artists finally do get back on the tour bus, they might have to skip the next five cities and go on to the sixth.”

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

The legislation would provide grants up to $12 million for live entertainment venues to defray most business expenses incurred since March, including payroll and employees’ health insurance, rent, utilities, mortgage, personal protection equipment, and payments to independent contractors.

NIVA’s chief argument for the legislation is coldly economic rather than sentimentally cultural. The organization cites a 2008 study by the University of Chicago that spending by music patrons produces a “multiplier effect” for the broader economy. For every dollar spent by a concert-goer at a live performance, the Chicago study determined, $12 in downstream economic activity occurs.

Explains Scott Plusquellec, nightlife business advocate for the City of Seattle: “You buy a ticket to a show and the direct economic impact of that purchase is that it pays the artist, bartender and the club itself as well as the band, advertisers, and promoters. The indirect economic impact,” he adds, “is that after you bought the ticket, you went to a barber shop or a hair salon to look good that night. You might also have dinner, go to a bar for a drink and tip the bartender. That’s the whole the idea of a ‘multiplier.’”

In Austin, that economic logic is an article of faith with city burghers, asserts Lozano of Visit Austin, who reports that live music in the capital city is roughly a $2 billion industry. To promote live music, the tourism bureau sponsors such endeavors as “Hire an Austin Musician.” That program, Lozano says, “sends musicians around the U.S. to represent us during marketing season.” In another promotional campaign, Visit Austin arranged for singer-songwriter Julian Acosta to play a gig at travel agents’ offices in London when Norwegian Air inaugurated direct flights between London and Austin in 2018. “The U.K. is one of our best markets,” he reports.

Even so, efforts by the business community and the City of Austin have failed to stanch much of the industry’s bleeding. According to its website, the city has disbursed $23.7 million in loans and grants to small businesses and individuals, but slightly less than $1 million of that has gone to live-music and performance venues, entertainment and nightlife, and live-music production and studios.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

The Continental Club on South Congress – a key fixture in the hip “SoCo” strip just over the Colorado River from downtown – appeared to do best. It picked up $79,919 from two programs: $40,000 in the CARES-backed small business grants program, and $34,919 from the city’s Creative Space Disaster Relief Program. Other clubs receiving $40,000 in the small business grants program included Stubbs, The Belmont, Cheer Up Charlies and the White Horse. (For a full list go to: http://www.austintexas.gov/edims/document.cfm?id=347299)

Joe Ables, owner of the Saxon Pub, a major Austin venue for jazz – blues singer Ball hailed it as one of several important Austin clubs “that sustains creative endeavor, especially for songwriters” – was vexed that his grant application was denied by the city “with no explanation.” Ables also voiced dissatisfaction that the city paid the Better Business Bureau a 5% administration fee to handle $1.14 million in relief funds, including determining which applicants were approved. “What would they know about live music,” he says.

Even for clubs that received city largesse, it hasn’t been nearly enough to sustain them. The North Door, which got $15,240, closed for good on September 11 (an ominous day — the anniversary of the attacks on the World Trade Center and the Pentagon.)

Meanwhile, enough clubs and venues were left out in the cold that club owner Stephen Sternschein could tell AltFinanceDaily just before the slide show was released: “I’ve heard talk of a $21 million grant program but most people I know haven’t seen a dollar of that.”

Sternschein is managing partner of Heard Presents, an independent promoter and operator of a triad of downtown clubs that includes the spacious Empire Garage, which features hip hop and urban jazz, and has space for 1000 music-goers. A member of NIVA, Sternschein describes efforts by both the state and local governments as “woefully inadequate.” Says he: “People are looking to the federal government for answers.”

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

“You can go out to dinner in Waco,” he observes, referring to the mid sized Texas city between Austin and Dallas best known as home to Baylor University and its “Bears” football team, fervent Baptist religiosity, and unremarkable night life. “Music brings in revenue to Austin and to Texas that wouldn’t otherwise come here.”

In addition, Jones says, the large presence of “artists, creative types, and freelancers” helps make Austin a strong selling point for “brain industries” to attract talent from the East and West Coasts. “It supports the technology industry by making it easier to recruit employees to live there,” he says. “Austin is an alternative to Silicon Valley. People who are progressive might be hesitant to come to conservative, red-state Texas from California but they’ll come to Austin because it’s culturally cool.”

Austin, which embraces the slogan “Keep Austin Weird,” is on the verge of becoming just like every place else in Texas. Should it relinquish its flavor and charm, it could discourage many of the assorted business groups and professionals from keeping Austin on their dance card as a popular destination for meetings, conferences and get-away trips.

Howard Freidman, managing director at Bluechip Jets, a broker of private luxury aircraft, had an earlier career as a technology industry executive. Partly drawn by his previous experiences with the city, Freidman moved to Austin earlier this year. “It had the same coolness and weirdness of New Orleans — but also with the professionalism of a tech city,” he says.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

Many of the technology firms – including such needy companies as Samsung, Intel, Rackspace, Facebook, and Apple – have each received tax breaks, grants and subsidies worth tens of millions of dollars from a variety of local jurisdictions. Not only have the city of Austin and Travis Country been beneficent, but adjacent county governments and the state of Texas have provided abundant support. A 2014 study by the Workers Defense Project, in collaboration with UT’s Lyndon B. Johnson School of Public Affairs, reported that the state of Texas showers big business with $1.9 billion annually in state benefits. Most recently, officials with Travis County and a local school district granted Tesla more than $60 million in tax rebates to build a massive “gigafactory” southeast of town near Austin-Bergstrom International Airport.

To house the burgeoning cohort of “knowledge workers,” there are condominium conversions, tear-downs, high-rises and other forms of frenetic real estate development which, in their train, bring higher property taxes, steeper rents, and unaffordable housing.

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

The drop-off in live music and the belt-tightening by musicians is causing third-party pain for people like veteran Austin journalist and publicist Lynne Margolis, whose national credits include stories for Rolling Stone online, and radio spots for NPR. “The public relations aspect of my work has dropped away because artists can’t afford to pay,” she says, “and music journalism is falling by the wayside. It’s hard not to feel to like a double dinosaur.”

Led by bars, restaurants and music venues, on many days the solemn departure of small establishments has the business news sections of Austin newspapers reading more like the obituary page. One hardy survivor is Giddy Ups – a throwback honky-tonk on the town’s outskirts that advertises itself as “the biggest little stage in Austin” – promising “just about everything,” says owner Nancy Morgan, including “country, blues, rock, bluegrass, and soul.” For the past 20 years Giddy Ups has developed a devoted following of musicians and patrons while fending off hyper modernity.

“It has an untouched, back-to-the-seventies, cosmic cowboy vibe,” says local musician Ethan Ford, a guitarist and bass player whose trio, The Slyfoot Family, has graced its stage. “It’s a time capsule,” Ford adds.

Morgan declined to disclose her annual receipts but in 2019, she reports paying out $188,000 in wages to employees, $72,000 to musicians, and $185,000 in combined sales taxes to the city of Austin and to the state. Despite her status as a taxpayer, employer and entrepreneur, she has received no state aid and is disqualified from receiving city pandemic assistance programs, meager as they may be, because she’s located in an extra-territorial jurisdiction.“

Nancy still bartends most nights and does all of the booking,” says Ford. “Her knowledge of the Austin music scene could fill a couple of books. I know a decent fistful of Austin venue owners and she’s about the only one that hasn’t given up, been forced out, or just retired. She’s a dynamo.”

Unless the cavalry arrives for Morgan and other holdouts, though, their musical days may be numbered.

Editors Note: Threadgill’s didn’t make it. The venue “has closed for good, the property has sold, and the building will eventually be torn down,” according to information disseminated for its Last Call Music Series. Its November 1st grand finale show featured Gary P. Nunn, Dale Watson, Whitney Rose, William Beckman, and Jamie Lin Wilson.

The building will be replaced with apartments.

New Jersey Legalizes Recreational Marijuana

November 4, 2020One chill result from the 2020 election was the legalization of recreational marijuana in New Jersey for adult use. In a 2-1 victory, Option One on New Jersey ballots passed, paving the way for a regulated environment for recreational use, possession, and cultivation in the Garden State.

4:20 PM.

Time to legalize it. pic.twitter.com/157WC7qgof

— Governor Phil Murphy (@GovMurphy) October 28, 2020

Before the vote, Gov. Murphy showed support

We did it, New Jersey!

Public Question #1 to legalize adult-use marijuana passed overwhelmingly tonight, a huge step forward for racial and social justice and our economy. Thank you to @NJCAN2020 and all the advocates for standing on the right side of history.

— Phil Murphy (@PhilMurphyNJ) November 4, 2020

The amendment was billed as not only a chance to increase tax revenue but as civil rights reform. Advocates argued that prohibition laws disproportionately harmed minority communities.

The change was initially put before the legislature in 2017 but failed to pass by 2019. A bipartisan supermajority put the choice up to the public referendum. Appearing in Willingboro on Tuesday, long time advocate of legalization, Gov. Phil Murphy, spoke on voting day in last-minute support.

“I got to supporting it first and foremost due to social justice,” Murphy said. “We inherited when I became governor the largest white, nonwhite gap of persons incarcerated in America, and the biggest contributor to that was low-end drug offenses.”

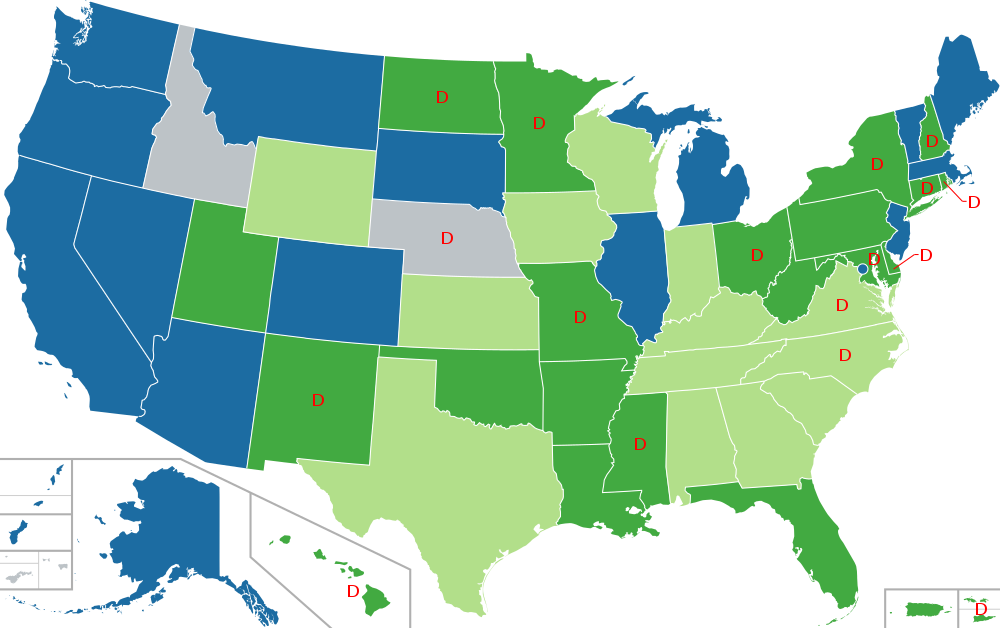

New Jersey was one of four states with legalization on the ballot, and all succeeded, bringing adult use to Arizona, Montana, and South Dakota as well. After Tuesday, more than 111 million Americans- a third of the country live in a state where recreational marijuana is legal.

Image SourceKEY

Blue = Legal

Dark Green = Legal for medical use

Light Green = Legal for medical use – limited THC content

Grey = Prohibited for any use

D = Decriminalized

Cannabis legalization advocates, like Doctors For Cannabis Regulation (DFCR), saw the day as a significant victory for industry and social progress. Dr. David Nathan founded DFCR in 2015, where he serves as president of the board. Dr. Nathan stood up and spoke out against the prohibition of marijuana 11 years ago and said he was one of the first accredited mainstream physicians to do so.

“I’m not a medical cannabis physician, I’m a psychiatrist who sees how much damage cannabis prohibition does compared to the drug itself,” Dr. Nathan said. “I’ve really been given the platform to speak up, but at the same time, it was hard to get colleagues to speak up on an issue.”

After working for NJ United for Marijuana Reform, Dr. Nathan founded DFCR to create an organization to facilitate physicians who wanted to get involved at a national level. The success of Tuesday’s vote demonstrates how far legal cannabis advocation has come, from a resounding no to a majority yes.

“A lot of doctors who understood cannabis prohibition as a tragedy and a mistake were concerned about what their peers would think about them if they spoke out,” Dr. Nathan said. “Now we’ve got a group of highly respected physicians organized and advocating strongly, not just for legalization but much more importantly for effective regulation.”

Dr. Nathan sees the NJ amendment as a significant chance for improvement in public health. Despite legalization, it is unclear how the new law will go into effect. Per the amendment, the state will create a regulatory framework and tax the sale of marijuana at 6.625%, but implementation is up for debate.

Legislators still have to agree on how a new Cannabis Regulatory Commission will function. The state will also have to choose how decriminalization, possession limits, growing limits work, and forgiveness of past marijuana crimes.

All of which will be figured out and are necessary to the fair implementation of the passage of the amendment, Dr. Nathan said.

But those changes may come fast. NJ, like many states, is hurting during the COVID recession. Last month New Jersey officials approved a budget that is set to borrow $4.5 billion from the Federal Reserve to plug pandemic-sized holes in state spending.

Basing estimates on Colorado’s experience after legalizing cannabis in 2014, the state legislature predicts NJ could see tax revenues of up to $126 million a year from recreational sales.

“According to the Colorado Department of Revenue, retail cannabis sales, excluding medical cannabis, totaled $1.2 billion in calendar year 2018,” The report said. “Assuming New Jersey experiences similar per capita sales of recreational cannabis as Colorado, total retail cannabis sales for New Jersey could reach $1.9 billion, yielding sales tax revenues of up to $125.6 million annually at the current 6.625 percent sales tax rate.”

With such high revenues, some suspect New Jersey to lead the way for other northeastern states; income will spur jealous neighboring Pennsylvania and New York to legalization in competition.

“If this gives both Pennsylvania and New York a push, that would be great,” Dr. Nathan said. “I do think it’s going to have an impact, now that there will be a state right in the middle of the Mid Atlantic that is going to have regulated sales.”

But even with tristate legalization, the cannabis industry faces a problem with funding.

Most firms in cannabis supply chains- from growers to dispensaries- are small businesses that suffer from a lack of access to bank funding. Because marijuana is an illegal Section 1 drug like Heroin on a federal level, banks and venture capitalists have their hands tied when it comes to credit. But with Tuesday’s victories for legalization, federal regulation is closure to changing.

“I think that each state that adopts, sends a stronger message to the federal government,” Dr. Nathan said. “The voters in those states are giving resounding victories to the notion that cannabis should be de-scheduled not rescheduled, and then regulated.”

deBanked has been following the SAFE Banking Act since it passed in the House last year, a piece of legislation that hopes to address cannabis banking problems by allowing legal pot firms to open banking deposit accounts.

The law was bundled into the HEROES act with the rest of business aid projects, stuck between the GOP-controlled Senate and the blue House since the summer. Depending on the Senate’s layout when ballots are fully counted, financial institutions that have left pot companies de-banked may be-danked.

Square, Stripe, Intuit, Shopify, Talked SMB Lending at LendIt Fintech 2020

October 8, 2020 The LendIt Fintech digital conference last week was a sign of the times. This year, millions of average businesses and consumers have had to go virtual: they had no choice. 2020 has been a year of struggle and survival, and a time of great fintech adoption.

The LendIt Fintech digital conference last week was a sign of the times. This year, millions of average businesses and consumers have had to go virtual: they had no choice. 2020 has been a year of struggle and survival, and a time of great fintech adoption.

Some firms have been more successful than others. Going full digital, LendIt introduced virtual networking at the conference- the first day alone saw 2,171 meetings. Zoom meetings and virtual greetings took the place of handshakes and elevator pitches that would regularly accompany the convention.

On day three, LendIt hosted a panel of SMB lending leaders from Stripe, Shopify, Square, and Quickbooks Capital. Bryan Lee, Senior Director of Financial Services for Salesforce, served as moderator and he focused the discussion on “How the leading fintech brands are adapting.”

THE PIVOT

Lee began the talk by asking Eddie Serrill, Business Lead from Stripe Capital, about how the industry has pivoted.

Serrill talked about how Stripe was powering online interactions and saw an influx of traditionally offline businesses switching over to their platforms. Stripe also saw an increased demand for online purchases and payment.

“We’ve been trying to find that right balance between supporting users that have been doing incredibly well,” Serrill said. “While trying to support our users who are seeing a bit of a setback.”

Stripe introduced a lending product in September of last year and now SMBs can borrow from Stripe and pay back by diverting a percentage of their sales, much like the other panelists’ companies offer.

Jessica Jiang, Head of Capital Markets at Square Capital, talked about how her firm adjusted. Square reacted to fill the niche of their underserved customers by introducing a main street lending fund, serving industries hard hit by the pandemic, Jiang said. Small buinesess that relied on in-person action like coffee shops and retail community businesses were given preferential lending options.

Product Lead at Shopify, Richard Shaw, said that this year his firm learned to be prepared for anything. Everything that Shopify was potentially going to do or planning on implementing in the coming years suddenly became a here-and-now necessity.

“We tore up our existing plans,” Shaw said. “It was like the commerce world of 2030 turned up in 2020. You need to do ten years of work, but you need to do it today.”

Shopify, the Canadian e-commerce giant has doubled in value this year. The firm launched Shopify Capital in the US and Canada in 2016 and has originated $1.2 billion in funding to small businesses since that time.

Luke Voiles, the VP of Intuits QuickBooks Capital, talked about how his team handled pandemic conservatively.

“Five years of digital shift has happened instantaneously due to COVID,” Voiles said. “Intuit is pretty recession-resistant in the sense that you have to do taxes, you have to do your accounting, and the shift to digital helps a lot.”

Business lending was different, Voiles said, as soon as his team saw COVID coming, they battened down the hatches, slowed lending, and pivoted to facilitating PPP.

PPP

Voiles said the craziest thing he has seen in his career was what Quickbooks did to deploy PPP aid.

Within about two weeks, almost 500 people from across Intuit came together to shift all the data they carried on customers to aid applications.

“We were uniquely positioned to help solve and deploy that capital,” Voiles said. “We have a payroll business where 1.4 billion business use us, we have a tax business where we have Schedule C tax filings, and we have a lending business. We were able to pivot and put the pieces together quickly.”

QuickBooks Capital deployed $1.2 billion to 31,000 business in a process that Voiles said was 90% automated. Now customers are awaiting other rounds of government aid.

Square’s Jiang said the initial shutdown weeks in March and April saw hundreds of Square team members working on PPP facilitation through the night and weekends. As the funds dried up those first two weeks, it was clear to Jiang the program was favoring larger firms and higher loan amounts, leaving out small businesses.

“That’s typical of investment bankers, but not very typical of tech,” Jiang said. “PPP is a perfect example of how small businesses are continuing to be underserved by banks.”

THE SHAKEOUT AND THE FUTURE

2020 has been a major shock to the lending marketplace. Voiles from Quickbooks said the amount of work it took to make it through the first wave was a significant shakeout.

“You’ve seen what’s happening with Kabbage and OnDeck and other transactions with people getting sold; there is a shakeout happening in the space,” Voiles said. “The bigger players will make it through and will continue to help small businesses get access to capital that they need.”

When asked about the future roadmap of QuickBooks Capital, Voiles said it wasn’t just about automating banking. Using Intuit’s resources to build an automated system is only half of the picture- the firm believes in an expert-driven platform. After the automated process, customers will be able to talk to an expert to review the data, and “check their work.” Voiles said Quickbooks wants to offer a service that is equivalent to the replacement of a CFO.

“These small businesses that have less than ten employees, they can’t afford to hire a pro,” Voiles said. “They need automated support to show them the dashboard and picture of what their business is.”

Pointing to Stripe’s online infrastructure, Serrill exemplified what successful lenders will offer next year: a platform that combines many needs of SMBs in one place.

“I think it’s really about linking all of this data, making it super intuitive and anticipating the need for their users, so they don’t need a team of business school grads to manage their finances,” Serrill said. “So they can get back to building the core of their business, not figuring out whether they have enough cash flow tomorrow.”

Jiang said the future of small business would be written in data, contactless payments, and digital banking. She sees consolidation in the Fintech space and has a positive outlook on bank-fintech partnerships.

The FDIC granted Square a conditional approval for the issuance of an Industrial Loan Company ILC in March this year. Jiang outlined plans on launching an online SMB lending and banking service next year called Square Financial Services if the conditional charter remains in place.

For Shopify’s future, Shaw was excited to look forward to the launching of Shopify balance- a cash flow management system, and Shopify installment payments. He reiterated that the success of Shopify’s lending division was due in part because making loans was not the entire business.

“Shopify Capital is one piece of a wider ecosystem,” Shaw said. “All these things together are more powerful than individual parts.”

{kind=link}