FIRE DRILL IN ILLINOIS: BUSINESS FUNDING COMPANIES TARGETED IN REPRESSIVE BILL

June 30, 2016* Update 6/30 AM: Sen. Jacqueline Collins, D-Chicago is expected to introduce a revised bill today.

** Update 6/30 PM: Reintroduction of the bill has been delayed while they wait for comments from additional parties

Bankers and non-bank commercial lenders – two groups that often disagree – are united in their opposition to financial regulation proposed in Illinois. Both contend that if the state’s Senate Bill 2865 becomes law it could choke the life out of small-business lending in the Land of Lincoln and might set a precedent for a nightmarish 50-state patchwork of rules and regulations.

Bankers and non-bank commercial lenders – two groups that often disagree – are united in their opposition to financial regulation proposed in Illinois. Both contend that if the state’s Senate Bill 2865 becomes law it could choke the life out of small-business lending in the Land of Lincoln and might set a precedent for a nightmarish 50-state patchwork of rules and regulations.

Foes say the measure was created to promote disclosure and regulate underwriting. They don’t argue with the need for transparency when it comes to stating loan terms, but they maintain that a provision of the bill that would cap loan payments at 50 percent of net profits would disrupt the market needlessly.

Opponents also regard the bill as an encroachment on free trade. “The government shouldn’t be picking winners or losers – the market should be,” said Steve Denis, executive director of the Small Business Finance Association, a trade group for alternative funders.

The states or the federal government may need to protect merchants from a few predatory lenders, but most lenders operate reputably and have a vested interest in helping clients succeed so they can pay back their obligations and become repeat customers, several members of the industry maintained.

“The ability to pay is really a non-issue,” noted Matt Patterson, CEO of Expansion Capital Group and an organizer of the Commercial Finance Coalition, another industry trade group. “I don’t make any money if a borrower doesn’t pay me back, so I don’t make loans where I think there is an inability to pay.”

Outsiders may find interest rates high for alternative loans, but companies providing the capital face high risk and have a short risk horizon, said Scott Talbott, senior vice president of government affairs for the Electronic Transactions Association, whose members include purveyors and recipients of alternative financing. Several other sources said the risks justify the rates.

Besides, a consensus seems to exist among industry leaders that most merchants – unlike many consumers – have the sophistication to make their own decisions on borrowing. Business owners are accustomed to dealing with large amounts of money, and they understand the need to keep investing in their enterprises, sources agreed.

In fact, no one has complained of any small-business lending problems in Illinois to state regulators, said Bryan Schneider, secretary of the Illinois Department of Financial and Professional Regulation and a member of Gov. Bruce Rauner’s cabinet.

Regulators should not indulge in creating solutions in search of problems, Sec. Schneider cautioned. “When you’re a hammer, the world looks like a nail,” he said, suggesting that regulators sometimes base their actions on anecdotal isolated incidents instead of reserving action to correct widespread problems.

But the proposed legislation could itself cause problems by placing entrepreneurs at risk, according to Rob Karr, president and CEO of the Illinois Retail Merchants Association, which has 400 members operating 20,000 stores. “It would stifle potential access to capital for small businesses,” he warned.

Quantifying the resulting damage would present a monumental task, but a shortage of capital would clearly burden merchants who need to bridge cash-flow problems, Karr said. Shortfalls can result, for example, when clothing stores need to buy apparel for the coming season or hardware stores place orders in the summer for snow blowers they’ll need in six to eight months, he said.

Restaurant owners and other merchants who rely on expensive equipment also need access to capital when there’s a breakdown or a need to expand to meet competition or take advantage of a market opportunity, Karr observed.

Capital for those purposes could dry up because just about anyone providing non-bank loans to small merchants could find themselves subject to the proposed legislation, including factoring companies, merchant cash advance companies, alternative lenders and non-bank commercial lenders, said the CFC’s Patterson.

Banks and credit unions are exempt, the bill says, but a page or two later it includes provisions written so broadly that it actually includes those institutions, said Ben Jackson, vice president of government relations at the Illinois Bankers Association.

Trade groups representing all of those financial institutions – including banks and non-banks – have joined small-business associations in working against passage SB 2865. “The most important thing is to make sure we’re coordinating with the other groups out there,” the SBFA’s Denis contended. “Actually, Illinois was good practice for the industry in how we’re going to go about dealing with attempts at regulation.”

Patterson of the CFC agreed that associations should coordinate their responses to proposed legislation. “We’ve tried to gather all the affected players in the space and have dialogue with them,” he maintained.

Even though that various associations reacting to the bill generally agreed on principles, their competing messages at first created a cacophony of proposals, according to some. “There was a lot of noise, and I think we’ll all learn from that,” Denis said. “The industry has to learn to speak with one voice to legislators.”

Citing the complexity of dealing with 50 states, 435 members of Congress and 100 senators, Denis said everyone with an interest in small-business lending must work together. “If we don’t, we lose,” he warned.

Many of the groups came together for the first time as they converged upon the Illinois capital of Springfield last month when the state’s Senate Committee on Financial Institutions convened a hearing on the bill. The committee allowed testimony at the hearing from three groups representing opponents. The groups huddled and chose Denis, Jackson and Martha Dreiling, OnDeck Capital Inc. vice president and head of operations.

City of Chicago Treasurer Kurt Summers was the only witness who testified in favor of the bill, according to Jackson. The idea of regulating non-bank commercial lenders in much the same way Illinois oversees lending to individuals arose in Summers’ office, said an aide to Illinois Sen. Jacqueline Collins, D-Chicago. Sen. Collins serves as chairperson of the Financial Institutions Committee and introduced to the bill in the senate.

Sen. Collins declined to be interviewed for this article, and Treasurer Summers and other officials in his of office did not respond to interview requests. However, published reports said Drew Beres, general counsel for Summers, has maintained that transparency, not underwriting, is the main goal. Talbott has met with Sen. Collins and said she’s interested primarily in transparency.

Support for the bill isn’t limited to the Chicago treasurer’s office. Some non-profit lending groups and think tanks back the proposed legislation, opponents agreed. The bill appeals to progressives attempting to shield the public from unsavory lending practices, they maintained.

Politicians may view their support of the bill as a way of burnishing their progressive credentials and establishing themselves as consumer advocates, said opponents of the legislation who requested anonymity. “It’s an important constituency,” one noted. “No one is against small business.”

After listening to testimony at the hearing, committee members voted to move the bill out of committee for further progress through the senate, Jackson said. Eight on the committee voted to move the bill forward, while two voted “present” and one was absent. But most of the senators on the committee said the legislation needs revision through amendments before it could become law, according to Jackson.

The legislative session was scheduled to end May 31. If the bill didn’t pass by then it could come up for consideration in a summer session if the General Assembly chooses to have one, Jackson said. If it does not pass during the summer, it could come to a vote during a two-week “veto session” in the fall or in an early January 2017 “lame duck session.” Unpassed legislation dies at that point and would have to be reintroduced in the regular session that begins later in January 2017, he noted.

Although time is becoming short for the proposed legislation, it’s a high-profile measure that could prompt action, particularly if amendments weaken the rule for underwriting, Jackson said. The Illinois General Assembly sometimes passes important legislation during lame duck sessions, he said, noting that a temporary increase in the state sales tax was enacted that way.

Whatever fate awaits SB 2865, some in the alternative funding business have suspected that the bill came about through an effort by banks to push non-banks out of the market. But cooperation among groups opposed to the proposed legislation appears to lay that notion to rest, according to several sources.

“I don’t get that impression,” Denis said of the allegation that bankers are colluding against alternative commercial lenders. “I think this shows banks and our industry can get together and share the same mission.”

Talbott of the ETA also counted himself among the disbelievers when it comes to conspiracy theories against alternative lenders. “I’d say that’s a misreading of the law and not the case,” he said. “Traditional banks oppose this because it would effectively reduce their options in the same space.”

The interests of banks and non-banks are beginning to coincide as the two sectors intertwine by forming coalitions, noted Jackson of the state bankers’ association. A number of sources cited mergers and partnerships that are occurring among the two types of institutions.

In one example, J.P. Morgan Chase & Co. is using OnDeck’s online technology to help make loans to small businesses. Meanwhile, in another example, SunTrust Banks Inc. has established an online lending division called LightStream.

At the same time, alternative funders who got their start with merchant cash advances and later added loans are contemplating what their world would be like if they turned their enterprises into businesses that more closely resembled banks.

At the same time, alternative funders who got their start with merchant cash advances and later added loans are contemplating what their world would be like if they turned their enterprises into businesses that more closely resembled banks.

And however the industries structure themselves, the need for small-business funding remains acute. Banks, non-banks and merchants agree that the Great Recession that began in 2007 and the regulation it spawned have discouraged banks from lending to small-businesses. The alternative small-business finance industry arose to fill the vacuum, sources said.

That demand draws attention and could lead to bouts of regulation. Although industry leaders say they’re not aware of legislation similar to Illinois SB 2865 pending in other states, they note that New York state legislators discussed small-business lending in April during a subject matter hearing. They also point out that California regulates commercial lending.

Many dread the potential for unintended results as a crazy quilt of regulation spreads across the nation with each state devising its own inconsistent or even conflicting standards. Keeping up with activity in 50 states – not to mention a few territories or protectorates – seems likely to prove daunting.

But mechanisms have been developed to ease the burden of tracking so many legislative and regulatory bodies. The CFC, for instance, employs a government relations team to monitor the states, Patterson said. The ETA combines software and people in the field to deal with the monitoring challenge.

And regulation at the state level can make sense because officials there live “close to the ground,” and thus have a better feel for how rules affect state residents than federal regulators could develop, Sec. Schneider said.

Easier accessibility can also keep make regulators more responsive than federal regulators, according to Sec. Schneider. “It’s easier to get ahold of me than (Director) Richard Cordray at the Consumer Financial Protection Bureau,” he said.

Also, state regulators don’t want to take a provincial view of commerce, Sec. Schneider noted. “As wonderful as Illinois is, we want to do business nationwide,” he joked.

State regulators should do a better job of coordinating among themselves, Sec. Schneider conceded, adding that they are making the attempt. Efforts are underway through the Conference of State Bank Supervisors, a trade association for officials, he said.

At the moment, state legislatures and federal regulators have small-business lending “squarely on their agenda,” the ETA’s Talbott observed. The U.S. Congress isn’t paying close attention to the industry right now because they’re preoccupied with the elections and the presidential nominating conventions, he said.

The goal in Illinois and elsewhere remains to encourage legislators to adopt a “go-slow approach” that affords enough time to understand how the industry operates and what proposed laws or regulations would do to change that, said Talbott.

At any rate, the industry should unite in a proactive effort to explain the business to legislators, according to Denis. “We need to work with them so that they understand how we fund small businesses,” he said. “That’s the way we can all win.”

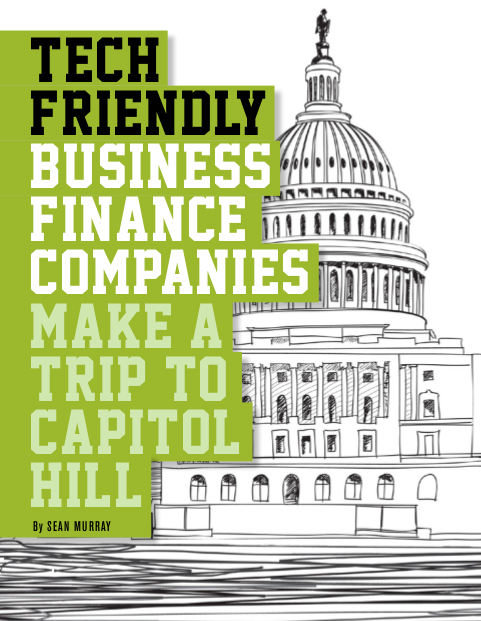

Business Finance Companies Visit Capitol Hill

June 17, 2016 Scores of companies providing working capital to small businesses descended on Capitol Hill in early May to educate policymakers about the benefits they provide to the economy. Among them was the Coalition for Responsible Business Finance (CRBF), the Electronic Transactions Association (ETA) and the Commercial Finance Coalition (CFC).

Scores of companies providing working capital to small businesses descended on Capitol Hill in early May to educate policymakers about the benefits they provide to the economy. Among them was the Coalition for Responsible Business Finance (CRBF), the Electronic Transactions Association (ETA) and the Commercial Finance Coalition (CFC).

The inability of banks to satisfy the demands of small businesses is not new, nor is it a problem purely borne out of the recession, data indicates. That’s partially why the Small Business Administration (SBA) exists, according to a 2014 report co-authored by former SBA Administrator Karen Mills.

“If the market will give a small business a loan, there is no need for taxpayer support,” the report states. “However, there are small businesses for which the bank would like to make a loan but that business may not meet the bank’s standard credit criteria.” That occurs so often that the SBA actually had to temporarily suspend guarantees last year because they had reached their limit.

“The SBA has a portfolio of over $100 billion of loans that lenders would not make without credit support,” according to Mills’ report. If that number looks big, it’s because it’s comprised mainly of loans to the larger end of the small business spectrum. Smaller businesses or businesses with smaller needs anyway, continue to be underserved. The average 7(a) loan guaranteed by the SBA in fiscal year 2015 for example was $371,628. Compare that to the $20,000 – $35,000 average deal size reported by some members of the CFC.

“Small firms were hit harder than large firms during the crisis, with the smallest firms hit the hardest,” Mills’ report states, but it adds that small businesses have been responsible for adding two out of every three net new jobs since 2010.

Tom Sullivan, who leads the CRBF, emphasized to AltFinanceDaily that job creation plays a crucial role in what their organization represents and stressed that it was very important to get the input of small business owners when policymakers consider new regulations.

The CFC meanwhile, estimates that aggregate funding between its members have preserved at least 1 million jobs. And OnDeck, who was on the Hill with the ETA, announced late last year that their first $3 billion in loans have generated an estimated $11 billion in US economic impact and actually created 74,000 jobs.

While the schedules and agendas of each group were different, the CFC reportedly met with nearly two-dozen House and Senate members or their staff in a single day.

Online Small Business Lending Task Force Initiated by the ETA

April 30, 2016 The Electronic Transactions Association (ETA) is now advocating on behalf of online small business lenders.

The Electronic Transactions Association (ETA) is now advocating on behalf of online small business lenders.

Though you might not have suspected it last week at Transact16, the ETA very much plans to involve themselves in the affairs of marketplace lending. That might not have been obvious from a Bloomberg article that reported that OnDeck, Kabbage and PayPal were forming a splinter organization as an “extension” of the ETA known as the Online Small Business Lending Task Force. Referred to as a new initiative in the announcement, the group’s mission is described as striving to “prevent hasty or overly restrictive regulations.”

But the group’s named lobbyist, Scott Talbott, is also the ETA’s lobbyist. And the three lenders named, were already members of the ETA. When Talbott was asked by AltFinanceDaily to clarify the relationship between the “task force” and the ETA, he said that the two weren’t separate. The “ETA organized its members to lobby on the issue. It’s what we do every day,” he wrote.

The “task force” merely highlights members in the trade group that share a common interest.

Formed in 1990 and comprising of over 550 companies across 7 countries, the ETA has served the payments industry well. OnDeck, Kabbage and PayPal therefore find themselves in good company and led by advocates with well-established government relationships.

Along with the ETA, the online small business lending industry has found support from the Marketplace Lending Association, the Small Business Finance Association, the Commercial Finance Coalition and the Coalition for Responsible Business Finance.

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”

Nine Organizations Submit Joint Response to Bizarre Illinois Small Business Lending Bill

April 16, 2016

A bill introduced in the Illinois State Senate to “protect” small businesses from lenders is causing small businesses themselves to scratch their heads. The bill would effectively outlaw nonbank business lending, which would render those declined by a bank, restricted from accessing capital through other means.

“As we all recall what happened in 2007-2008 in the housing market, so many people went under due to these predatory lending practices. So I’m happy we’re being proactive instead of reactive with this issue,” said Illinois State Senator Emil Jones.

That proactive approach is to scorch the earth, which is creating staunch pushback from within the small business community. A letter co-signed by the following nine organizations was submitted last week to Jacqueline Collins, the Senator who introduced the bill:

- Coalition of Responsible Business Finance

- Electronic Transactions Association

- Illinois NFIB

- Illinois Retail Merchants Association

- Equipment Leasing and Finance Association

- Small Business & Entrepreneurship Council

- Small Business Investors Alliance

- National Small Business Association

- Illinois Chamber of Commerce

Dear Chair. Collins:

The undersigned organizations, companies, and coalitions who have business in Illinois and throughout the country are writing to express our concerns with SB 2865, the Small Business Lending Act.

We all share your goal of helping small businesses. However, we believe that the prescriptive underwriting standards, complex regulatory mandates, and expansion of civil and criminal liability will prevent small businesses from getting the capital they need to grow and benefit their communities and the state of Illinois.

We respectfully ask the Committee to study the issue of access to capital for small business in Illinois through a transparent process that involves the direct input from small businesses prior to moving forward with SB 2865.

We are hopeful that a deliberative, inclusive, and public process could produce a report that will assist your Committee and the Illinois legislature. Among the questions a study committee could try and answer are: what methods of transparency and disclosure by alternative lenders and finance companies would make it easier for responsible small business borrowing; should non-profit lenders be exempt from alternative lending and finance requirements; and how does the securitization and sale of alternative loans benefit small business lending?

Of course, there are many additional issues that small business stakeholders will identify through a study committee in an effort to assist your Committee prior to any legislative action on SB 2865. We stand ready to assist you in that effort and we appreciate the consideration of our views.

Conflicting information has come out of the Senate since a hearing was held about it on the morning of April 12th. Fox reports that it is heading to the Senate floor for discussion with the expectation of some modifications, while those that were there say that it has been put on hold until early 2017 since it’s a presidential election year.

SCORCHED EARTH – Controversial Bill Could Eliminate Marketplace Lending, Merchant Cash Advance and Nonbank Business Loans in Illinois (and starve small businesses in the process)

April 9, 2016

The State of Illinois wants to make it a Class A misdemeanor for providing small businesses with quick, easy working capital.

The world’s strangest bill, dubbed the Small Business Lending Act, could send marketplace lenders, nonbanks, and merchant cash advance companies to prison for up to 1 year if applicants don’t submit at the very least, their most recent six months bank statements, the previous year’s tax return, a current P&L, a current balance sheet, and an accounts receivable aging.

Loans in which the monthly payments exceed at least 50% of the business’s monthly net income would be illegal, which implies that any business that is either breaking even or running at a loss would be banned from obtaining a loan from alternative sources.

This is not an April Fools’ prank. Not even preemption granted under the National Bank Act or Federal Deposit Insurance Act is safe.

Introduced into the State Senate under the pretense that it would squash predatory lenders, the bill’s licensing and compliance proposal would also effectively outlaw marketplace lending and securitizations by making the sale of loans illegal unless it’s to a bank or another state-licensed party. Even merchant cash advances are referenced specifically but almost as an afterthought and defined in such a way that even traditional factoring companies may be in jeopardy.

No licensee or other person shall pledge, assign, hypothecate, or sell a small business loan entered into under this Act by a borrower except to another licensee under this Act, a licensee under the Sales Finance Agency Act, a bank, savings bank, community development financial institution, savings and loan association, or credit union created under the laws of this State or the United States, or to other persons or entities authorized by the Secretary in writing. Sales of such small business loans by licensees under this Act or other persons shall be made by agreement in writing and shall authorize the Secretary to examine the loan documents so hypothecated, pledged, or sold.

At a time when most fintech lenders are advocating for smart regulation, the State of Illinois apparently wants to end all nonbank commercial finance under $250,000 completely, with the exception of one organization (which we’ll get to shortly).

At a time when most fintech lenders are advocating for smart regulation, the State of Illinois apparently wants to end all nonbank commercial finance under $250,000 completely, with the exception of one organization (which we’ll get to shortly).

There are some exemptions granted under this proposal of course. Loans over $250,000 aren’t subject to it, nor are any loans made by Illinois-based banks or credit unions, that is unless they are acting as the agent for another party like say perhaps a marketplace lender.

Hidden inside is also an exemption for nonprofit lenders, a loophole left open for Accion Chicago, the nonprofit masterminds behind the bill who seem to want the entire state’s lending market all for themselves.

Illinois State Senator Jacqueline Collins Introduced This Bill

Senator Collins introduced the legislation as an amendment to Senate Bill 2865 on April 6th. A former journalist, she’s now the chairwoman of the Illinois Senate Financial Institutions Committee. Among her self-professed accolades is that she “has played a key role in addressing predatory lending and high foreclosure rates in Chicago through legislation that protects homebuyers and homeowners with subprime mortgages.” She lists the Mortgage Rescue Fraud Act, the landmark Sudan Divestment Act and the Payday Loan Reform Act among her major legislative accomplishments.

It’s no surprise then that sections of the bill are borrowed straight out of the Payday Loan Reform Act. Collins isn’t acting on her own however…

Chicago City Treasurer Kurt Summers

In January, Senator Collins joined Chicago City Treasurer Kurt Summers in a call for “new legislation to protect small business owners from misleading and dishonest predatory lenders.” In a closed-door hearing, the committee supposedly heard from business owners, advocates and elected officials on predatory lending.

“Chicago’s small business community deserves protection from the unchecked greed of predatory lenders,” Treasurer Summers said. “While access to capital is the number one concern of small business owners across the state, bank and commercial loans continue to decline, steering them to underhanded lenders. As we continue to urge banking partners to increase their local investment, this new, common-sense legislation would ensure transparency in lending that so often puts our entrepreneurs at risk.”

Of note is his use of the phrase “banking partners” since this bill has bankers all over it, as we’ll get into shortly. Summers represents the Chicago Mayor’s office and the Mayor’s office says they’ve launched this campaign thanks to partners like Accion Chicago.

Hon. Kurt Summers, Treasurer, City of Chicago from City Club of Chicago on Vimeo.

Accion Chicago and the Mayor’s Office

Last year, Mayor Rahm Emanuel announced a joint campaign with Accion Chicago to help small businesses avoid predatory lending.

Accion Chicago, ironically makes business loans themselves, having originated 535 loans totaling $4.8 million in 2014 with a maximum loan size of $100,000.

Who is Accion Chicago really?

The Small Business Lending Act virtually ensures that small business loans under $250,000 only be facilitated by banks and nonprofits. Isn’t it convenient then that Accion Chicago is not only a nonprofit, but also funded and staffed by banks?

According to their 2014 annual report, Citibank and JPMorgan Chase were two of their three largest supporters (the third was the US Treasury!). Below are some of the figures:

$100,000+

- Citibank

- JPMorgan Chase

$50,000 – $99,999

- Bank of America

$20,000 – $49,999

- Fifth Third Bank

- PNC Bank

- U.S. Bank

$5,000 – $19,999

- American Chartered Bank

- Alliant Credit Union

- BMO Harris Bank

- First Bank of Highland Park

- First Eagle Bank

- First Midwest Bank

- Ridgestone Bank

- State Bank of India

- The PrivateBank

- Wells Fargo Bank

About a dozen more banks gave less than $5,000.

JPMorgan Chase has also been a partner of the annual Taste of Accion fundraising event, and was the lead sponsor in 2014, a spot that costs $30,000. Benefactor sponsorships which cost $20,000 each were comprised of American Chartered Bank, Capital One, Northern Trust Company, and Wintrust Bank. And the lesser sponsorships? Again, mostly banks.

JPMorgan Chase has also been a partner of the annual Taste of Accion fundraising event, and was the lead sponsor in 2014, a spot that costs $30,000. Benefactor sponsorships which cost $20,000 each were comprised of American Chartered Bank, Capital One, Northern Trust Company, and Wintrust Bank. And the lesser sponsorships? Again, mostly banks.

You know who hasn’t donated to Accion Chicago? Marketplace lenders and merchant cash advance companies.

Accion Chicago raised only $1.4 million in 2014 from public support, the bulk of which came from banks or related traditional financial institutions. So is it just a coincidence that this predatory lending bill they’re supporting grants exemptions to all the banks from compliance?

Accion Chicago’s 2014 Board of Directors includes executives from:

- American Chartered Bank (chairman)

- First Eagle Bank

- JPMorgan Chase

- Ridgestone Bank

- MB Financial Bank

- Talmer Bank & trust

- Citibank

- First Midwest Bank

The 2014 committees were made up almost entirely of bank executives from:

- First Eagle Bank

- The PrivateBank

- Ridgestone Bank

- U.S. Bank

- JPMorgan Chase

- Forest Park National Bank & Trust Co.

- MB Financial Bank

- FirstMerit Bank

- Wintrust Bank

- Standard Bank & Trust Co.

- First Midwest Bank

- Wells Fargo Bank

- Seaway Bank & Trust Co.

- Metropolitan Capital Bank

- Evergreen Bank Group

- First Financial Bank

- PNC Bank

Thanks to the impartial work of these good citizens, they have discovered that small businesses should only be working with banks or nonprofits funded and staffed by banks and have craftily devised a bill to legislate all the alternatives out of existence.

If this was really about predatory lending, then they screwed up big time

All coincidences aside, some of the bill’s rules have nothing to do with protecting borrowers, like the required $500,000 surety bond to become licensed for example. Compare that to California’s $25,000 licensed lender surety bond. And the restriction on being able to sell or securitize a loan, how does that help small businesses?

These requirements and others suggest that it’s about preventing all alternatives from existing in the marketplace, rather than predatory alternatives. The losers would undoubtedly be small businesses and the Illinois job market. Senator Collins and Treasurer Summers, both of whom have a strong track record of empowering their constituents financially, may have underestimated or overlooked the likely negative consequences of this bill.

The nonbanks

Several nonbank trade groups are reportedly in the process of formulating a response.

The Commercial Finance Coalition for example, a nonprofit coalition of financial technology companies, told AltFinanceDaily that they are concerned about the impact this will have on the Illinois job market and will indeed have representatives on the ground in Illinois.

They also wanted to make known that they welcome support from marketplace lenders, nonbanks and merchant cash advance companies in these efforts and that interested parties should email Mary Donahue at mdonohue@commercialfinancecoalition.com

To contact Senator Jacqueline Collins who introduced the bill, call her at 217-782-1607.

Business Loan Brokers Encounter Hard Times

April 6, 2016 Feeling a little bearish about the business lending industry lately? If you’re a business loan broker, you’re not alone.

Feeling a little bearish about the business lending industry lately? If you’re a business loan broker, you’re not alone.

Marketing costs are going up while the response rates of marketing are generally going down. It’s a trend that’s lightly covered in the March/April issue of our magazine that has just been dropped in the mail. But there’s more to it. Several recent new broker shops have failed or are failing within just their first few months of operation. Employers have become more litigious with former employees, alleging violations of non-competes and/or non-solicit agreements, and at least one sales agent apparently went too far and was arrested in early February for backdooring deals.

The number of emails AltFinanceDaily has received about stolen commissions, rogue employees and general grievances has shot up in recent months, and on one industry forum, sales agents are now publicly voicing their frustrations. One thread that was aptly titled, Merchant cash advance crushed me, was posted by a discouraged broker. “I’ve been in this business for a year and I can say this is the hardest thing I’ve ever done from a business perspective,” he said. One user responded by saying, “fail rate is very high. Competition is crazy. If you can’t spend money on marketing, including a sizable outbound sales force, you are a dead duck.”

“The market has changed,” said Fundzio CEO Eddie Siegel to AltFinanceDaily in the previous issue. “The cost of capital has gotten a lot lower for the customer, and since there are more brokers in the marketplace they are willing to take a lesser amount just to get the deal to the finish line.”

“A lot of brokers are carpet bombing, they’re on the phone all day,” said Blindbid President Michael O’Hare. “I talked to one guy who said he makes 400 or 500 calls a day on a manual dial.”

In an environment of more calls, lower response rates and lower commissions, it’s no surprise that outrage over backdoored deals has overshadowed stacking as the industry’s most pressing issue.

Even funders have stepped up their legal pursuit of other funders through allegations of tortious interference. Whether such cases have merit is for the courts to decide, but they are a sign of the times that money is no longer raining from the sky. Lines are being drawn. In a market where everyone was once a winner, now there must be losers.

Even funders have stepped up their legal pursuit of other funders through allegations of tortious interference. Whether such cases have merit is for the courts to decide, but they are a sign of the times that money is no longer raining from the sky. Lines are being drawn. In a market where everyone was once a winner, now there must be losers.

Even the political atmosphere is changing. In just the last few months, the Small Business Finance Association has hired an executive director and two additional new advocacy groups were formed, the Commercial Finance Coalition and the Coalition for Responsible Business Finance.

“A few years ago, individual brokers could be making $20,000 or even $40,000 a month. Now those numbers are much more difficult to reach unless brokers have a unique lead generation method or their own money to participate in the deals,” said Zachary Ramirez, a vice president at World Business Lenders.

Of course, it’s not bad for everyone. In February, AltFinanceDaily featured a sales closer whose team collectively originated $47 million in deals last year. He’s not alone. Veteran players, particularly those that have been in the industry for nearly a decade acknowledge that they have first mover advantage over the newer entrants because their portfolios are so big or they have weathered the bumps and don’t get as frustrated by them.

Funders that know the pains brokers are going through are attempting to address it in their marketing, with some assuring their prospective partners that they have no inside sales force, and thus no way to steal a deal. For those with inside sales forces, they are relying on their well established reputations to do the talking.

Anonymous deal soliciting has been mostly outlawed on industry forums to curtail bad experiences, but they still happen on other mediums. One broker complained on LinkedIn this week that a lead generator based in the Philippines had allegedly pocketed his $2,500 upfront fee and then changed their phone number and disappeared. That lead generator is still advertising his wares through social media.

If that’s not a sign of the times, then I don’t know what is.

The Coalition for Responsible Business Finance Adds Yet Another Perspective on Small Business Lending Advocacy

March 29, 2016Is three a crowd? The Coalition for Responsible Business Finance (CRBF) seeks to improve small business finance.

As a new advocacy organization, the CRBF is dedicated to bolstering the credibility, reliability and security of the growing non-traditional small-business lending industry, they say. Spearheaded by Tom Sullivan, former Chief Counsel for Advocacy in the Small Business Administration, CRBF Advisory Board executives include representatives from the National Federation of Independent Business (NFIB), the National Small Business Association (NSBA), and the Small Business & Entrepreneurship Council (SBE Council).

“CRBF was created to educate state and federal policymakers, media, and communities on how technology and innovation are providing small businesses access to capital that is necessary for growth,” Sullivan said in an organization announcement this morning.

The organization has been developing for some time, but its official pronouncement nearly coincides with that of the Commercial Finance Coalition, another group with a similar goal.

The organization has been developing for some time, but its official pronouncement nearly coincides with that of the Commercial Finance Coalition, another group with a similar goal.

And it’s shaping up to be quite the Spring here in 2016 because the Small Business Finance Association, yet another organization, is preparing to unveil a white paper of guiding industry principles.

And so that makes three, yet each appear to be bringing their own unique perspectives to the table. That is perhaps better than hundreds of unorganized perspectives under no collaborative banners, some industry vets are saying.

“Small business owners expect and deserve choices for credit,” Sullivan said. “And we at the [CRBF] believe that a better understanding of non-traditional small business lending will lead to greater acceptance by customers, regulators, and local, state, and federal elected officials.”

Touché.

{kind=link}