OLA CEO Mary Jackson: Colorado True Lender Bad for Borrowers

September 21, 2020 Last month, the Colorado Attorney General’s office announced a settlement with Avant and Marlette Funding, setting a precedent for how “true lender” cases will be handled. The fintech lenders and their partners are free to lend in the state, subject to a lot of restrictions, as long as they stick below the 36% APR level.

Last month, the Colorado Attorney General’s office announced a settlement with Avant and Marlette Funding, setting a precedent for how “true lender” cases will be handled. The fintech lenders and their partners are free to lend in the state, subject to a lot of restrictions, as long as they stick below the 36% APR level.

Some touted the decision as a safeguard for fintech bank partnerships. Still, many, like those represented in the Online Lenders Alliance (OLA)- saw misplaced regulation that harms borrowers more than it helps.

Mary Jackson, CEO of OLA, said that while well-meaning, the 36% rule arbitrarily limits the ability for non-prime credit customers to get a loan at all. The limit draws an arbitrary line in the sand, based on an outdated centuries-old lending system, and doesn’t describe loans that last shorter than a year very well, Jackson said.

“What it did was drive out all the lenders,” Jackson said. “Non-prime consumers have fewer choices. They have to go and be subject to fraud or more unscrupulous lenders, or they have to go back to overdraft as another option.”

Jackson represents a group of lenders that offer online services, which regularly partner with banks to provide loans nationwide at higher APR rates than some states allow. Jackson said these are not fintech “rent-a-bank” cases to skirt state regulations, but natural partnerships that enable larger institutions to gain the tech and talent of leading tech companies to reach a greater customer base.

“Big banks cannot keep up with the technology that fintech providers have developed,” Jackson said. “A key US bank has a lot of data scientists that they employ, but if you’re a regional or smaller bank, you don’t have that capability: it’s nearly impossible to drive an IT team as a banker.”

Jackson said that when her firm Cash America, that offered storefront cash advances, was bought by online lender CashNetUSA, she saw the differences between in-person transactions and the IT teams necessary for online lending. “It’s like two different worlds, two different ways of looking at something.”

“Our lenders are sophisticated like Enova, Elevate, CURO, Access Financial,” Jackson said. “These are companies that employ hundreds of data scientists that compete for jobs with Google in Chicago and a small regional bank can’t keep up.”

Fintech talent is helping to reach the 42% of Americans that have non-prime credit scores- FICO scores below 680, according to the Domestic Policy Caucus.

Jackson said these customers, many of whom can pay for loans, have almost no options. Jackson sees many of her partner companies offering a “pathway to prime” service, empowering customers to rehabilitate their credit.

“Most of these people are non-banking customers, these folks have damaged or thin file credit,” Jackson said. “Most banks don’t service that customer, except for overdraft- a 35$ fee for lack of money in their account- I think bankers want to be able to offer longer-term installment loans.”

Jackson said research backs up her claims, pointing to a 2018 US Treasury report that discussed how banks would have to rely on fintech partnerships to innovate and drive product change. That’s what is finally happening, Jackson said.

She also pointed to a 2017 study into the effects of the 2006 Military Lending Act. The act intended to protect military families from lending products with an APR above 36%. The study out of West Point found that the limit only hurt military members, some of which lost their security clearances when their credit fell too low.

“We find virtually no statistically or economically significant evidence of any adverse effects of payday lending access on credit and labor outcomes. In a few cases, we find suggestive evidence of the positive impacts of access. For example, our second survey suggests that a 1 standard deviation increase in the fraction of time spent in a payday loan access state decreases the probability of being involuntarily separated from the Army by 10%”

Not only was there no harm done, but the paper argues on behalf of payday lending as a healthy way to maintain the credit necessary to keep a military job.

She sees similarities in the legal fight over the creation of interstate credit card laws in the 50s and 60s, saying it used to be the case that consumers had to use a texas-based or California based card. The country had to decide how interstate credit worked then, and with the induction of new technology to loans today, the same question is being asked.

The majority of Jackson’s clients offer products above the 36% limit, in the 100 to 175% APR range. She said that looks high, but consumers are looking at it on a monthly basis, and most of them pay it off early.

“These fintech partnerships allow the bank to offer one rate to everybody across the United States,” Jackson said. “We feel that really adds more democracy to credit, making sure that those who’ve been left out of banking have a shot at it.”

Puerto Rican Businesses & People Resilient In Spite of Pandemic and Challenges, Says Alvelo

September 16, 2020 While the US economy slowly opens back up to careful in-person commerce, the territory of Puerto Rico is still facing rising case numbers- So how is business in the “Island of Enchantment?”

While the US economy slowly opens back up to careful in-person commerce, the territory of Puerto Rico is still facing rising case numbers- So how is business in the “Island of Enchantment?”

“I don’t think there’s anything that will shake the confidence of our small business owners in Puerto Rico,” said Sonia Alvelo, CEO of Latin Financial. “Businesses and the people of Puerto Rico are the most resilient I have ever known: I know that as I am one of them.”

Alvelo, a native to the island, has won awards as a top entrepreneur of the year for her business financing partnerships in the US and Puerto Rico. She said that even as the island faces its hardest challenges, the spirit of entrepreneurship remains unbroken.

Puerto Rico has been hit by irregular misfortune in the past couple of years. Destruction from Hurricane Maria and Irma damaged the 2017 infrastructure of the island immeasurably, and the response of the US government was painfully lacking. Commerce continued with caution, seeming to rebound. Then this year, earthquakes and aftershocks punctuated January and February, foreboding the coming storm.

The pandemic was slow to reach the island; Puerto Rico was the first US state/territory to impose a quarantine, banning business and all travel March 15th. The region is a territory of the United States, so it could not directly enforce control over its borders. Recently, Puerto Rico made the news with an increasing case count.

There’s also been the troublesome search for a new governor. After a mass protest, Governor Ricardo Rosselló stepped down last year. After his successor ‘appointment’ was deemed unconstitutional by the Supreme court of Puerto Rico, Wanda Vazquez, the former Secretary of Justice, took office.

In the August primary, thousands of ballots got stuck in delivery trucks that did not move, never reached polling locations. The candidates are now petitioning for a re-vote and the counting of the votes that were cast. The courts are still deciding, so even the election is facing challenges in Puerto Rico.

Besides that, the tourism industry has been devastated. Though the early shut down saved lives, the island saw an unemployment rate of up to 23% in July alone. That could be a low estimate, considering that half of the Puerto Rican workforce hold a job in the “informal economy.” The New York Times reports that the real unemployment rate in the middle of the summer could have reached close to 40%.

Even so, Alvelo conveyed the enduring willpower of the Puerto Rican people, that there was still confidence things would turn around.

Alvelo is partnered with more than 97 pharmacies in Puerto Rico as an MCA provider, as well as with gas stations and other small businesses. She said that she has been receiving calls for business financing options non-stop, on a day-to-day basis. Alvelo shared information she learned from one of her clients.

“They suffered the most at the beginning, but you know only 5-10% of pharmacies in the islands are open,” Alvelo said. “But even still, and we’re talking a hurricane, earthquakes, a pandemic, everything- I still don’t think that anything will change the confidence of business owners in PR.”

Alvelo is standing right next to Puerto Rican business owners, talking to them through their increasing needs during this time, she said. Latin Financial facilitated almost $2 million in PPP loans and $2 million in EIDL loans in the US and PR.

“That was the best experience- when they got the PPP funds,” Alvelo said. “They were crying over the phone; it was incredible.”

Brendan Lynch, Alvelo’s fiancé and business partner, said that the program had a rough rollout. It was unclear how long the Fed money would last, but PPP ended up working well for Puerto Rican businesses. He even saw BlueVine begin funding Loans in PR for the first time.

“One of our finders here in the US was approved for the program, and we were able to use their online platform,” Lynch said. “And normally they don’t really fund in Puerto Rico, but they did allow Puerto Rican businesses to apply for funding; which is great because they had the technology to make it so simple and quick.”

Lynch said Latin Financial was sure to share links to a PPP loan application with every client to make sure aid funds were as accessible as possible.

“Businesses are probably still down-scaled somewhere between 60 to 70% of their total revenue,” Lynch said. “they’re still working shorthanded with less people in the office, and regulations on how many people you can have in your business are making it harder.”

Alvelo and Lynch are no strangers to environmental forces affecting their plans- the pair were planning on getting married in PR in 2017 before the hurricanes hit.

“We started actually looking [for a venue] again, and then COVID happened,” Alvelo said. “Clients were going to be invited and are always asking how they can help, just like when everything happened with COVID, the pharmacies all got together, and said if you need this let us know. Businesses are really working together because they know that they need each other.”

“We started actually looking [for a venue] again, and then COVID happened,” Alvelo said. “Clients were going to be invited and are always asking how they can help, just like when everything happened with COVID, the pharmacies all got together, and said if you need this let us know. Businesses are really working together because they know that they need each other.”

Maria Barzana, the owner of Farmacia Asturias, has been a longtime client of Latin Financial, one of the first dating back to 2015. Barzana went to Alvelo for help. She said the island did not feel an economic impact until this August. Businesses, including most medical offices in the country, have been closed for the past five months. Pharmacies are finally feeling it.

“At the beginning of COVID-19, we were able to manage the economic factor by invoicing refills of prescriptions and the sale of basic necessities related to COVID,” Barzana said. “Due to social distancing, the flow of clients/patients has decreased, concentrating on items necessary to combat COVID-19 and maintenance medications.”

Latin Financial is almost back to regular funding after rushing to help complete PPP and EIDL stimulus loans. Sonia Alvelo will be a panelist speaker this Sept. 24, for the annual Latinas & Power Symposium.

University of Delaware, Other Universities Going Long on Fintech

September 15, 2020The University of Delaware recently received a $9 million tax incentive to construct a new Fintech Center on its premier Science, Technology, and Advanced Research (STAR) campus, with help from a community-building company Cinnaire. Slated for completion in 2021, the building marks yet another fintech-focused resource for higher education.

Financial technology programs have long been offered at prominent business schools such as Harvard, Stanford, and Columbia, international schools such as Oxford, and research institutions like MIT since the late 2000s.

Now that fintech has become a long term value creator in the financial world, other institutions such as the University of Michigan, Fordham, and Delaware are excited to implement fintech opportunities on campus for undergraduate and graduate students alike.

Discover Bank and Cinnaire jointly funded the building, a $39 million project. According to Delaware plans, it will create a space on the Delaware STAR campus to host a new Financial Services Incubator to encourage research and collaboration between students and industry leaders.

Discover Bank and Cinnaire jointly funded the building, a $39 million project. According to Delaware plans, it will create a space on the Delaware STAR campus to host a new Financial Services Incubator to encourage research and collaboration between students and industry leaders.

“The FinTech building will bring together computer science, engineering and business experts in cybersecurity, human-machine learning, data analysis, and other emerging financial technologies,” said Levi Thompson, Dean of the College of Engineering. “These collaborations will allow us to provide our students with a very unique experience that prepares them to excel in the workforce. Furthermore, our Fintech discoveries will benefit people throughout Delaware and the world.”

Cinnaire is a national nonprofit that focuses on improving communities’ financial health by creating capital solutions to revitalization projects: lending funds, managing, and building housing structures.

Funding communities is what Cinnaire does best: in this case, utilizing a New Markets Tax Credit to fund an addition to the Delaware campus.

The nearby University of Fordham at Lincoln Center has also been trending toward preparing students for a fintech world. Undergrad and graduate students pursuing an MBA through the Gabelli School have the option of a fintech concentration.

The nearby University of Fordham at Lincoln Center has also been trending toward preparing students for a fintech world. Undergrad and graduate students pursuing an MBA through the Gabelli School have the option of a fintech concentration.

The course work not only incorporates data science and machine learning skills into the worlds of credit lending and risk management but facilitates relationships between students and a wealth of industry partners.

Sudip Gupta, professor, and Director of the MS Quantitative Finance program, spoke about the courses’ popularity there. The program is ranked in the top 20 of its kind in the world by Risk Magazine.

He has seen a revolution in fintech in the past few years that has recently received a big push by pandemic forces, introducing the wholesale adoption of fintech techniques into traditional financial institutions.

“The fintech revolution in the industry- big data, machine learning techniques, storage capacity, and cloud computing has been going on for the last couple of years,” Gupta said. “The pandemic provided the big push to move toward that direction.”

Gupta has been following the development of alternative credit closely, recently publishing an award-winning paper studying machine learning to create alternative consumer credit scores using mobile phone and social media data.

“The idea of my research- let’s look at people who do not have a credit history or enough traditional credit you could get from a FICO score,” Gupta said. “Using this data, it turns out they are better predictors, and better to judge than FICO, and can reach out to more people.”

Gupta is excited for the adoption of big data techniques into alternative and traditional consumer loans because it offers a win-win for consumers and institutions alike, he said. Echoing the findings of many successful alternative finance companies, Gupta said his research showed that collected data could offer better insight for lending than “stale FICO scores.”

Up north at the Univerisity of Michigan, Professor Robert Dittmar at the Ross School of Business heads the Fintech Initiative. He is working on adding even more fintech classes. Recently, through a partnership with PEAK, a Chicago fintech lending company, Michigan launched a fintech initiative that incorporates undergrad and grad classes, faculty research, and a fintech entrepreneurial club that connects students to industry leaders.

Up north at the Univerisity of Michigan, Professor Robert Dittmar at the Ross School of Business heads the Fintech Initiative. He is working on adding even more fintech classes. Recently, through a partnership with PEAK, a Chicago fintech lending company, Michigan launched a fintech initiative that incorporates undergrad and grad classes, faculty research, and a fintech entrepreneurial club that connects students to industry leaders.

Michigan Ross is adding fintech classes for a variety of reasons.

“The simplest reason: students are interested in learning more about this kind of space,” Dittmar said. “And we’re seeing more demand from the industry side for students that know more.”

For years Dittmar said tech companies and startups in silicon valley were pioneering innovations in the industry. Through talking with alumni and contacts in the industry, Michigan found that fintech has gotten to the place where there is an excellent supply of data engineers. Still, there is a demand for professionals with the financial business expertise to implement these technologies.

“What we are trying to do at Ross is fill in that gap,” Dittmar said. “what we’d like is for [students] to know enough about the technology that they can provide the insights of finance and business to the people that are doing that technical work.”

At Ross, they are organizing what will one day be like a fellowship program. The program will feature a combined learning experience: students will learn data analytic finance, apply their computing skills in credit decision making classes, and then connect with the industry in experiential learning classes.

“In the last couple of years, I have been taking students to London to work at fintech startups in the UK,” Dittmar said. “And we are hoping to expand that program so that most or all graduate students have the opportunity to participate in something like that.”

Last year Ross hosted a “Fintech Challenge” competition to design a banking service to reach customers in a “banking desert” in rural Michigan. The program is hoping to host another challenge this year, despite complications of COVID-19.

Lendini Relaxes Previously Announced Covid-Guidelines

September 9, 2020Bensalem, PA –September 9, 2020– Lendini is excited to announce its return to small business funding. Through superior efficiency and analysis, the company has improved the process of alternative funding from some of the brightest minds in finance, technology and analytics. With updated (temporary COVID-19) guidelines, they remain dedicated and committed to their merchants and ISOs in these unprecedented times.

Lendini works directly with you to prepare the best package for your client, whether that be a Business Cash Advance (BCA) or Merchant Cash Advance (MCA). Simply put, Lendini advances money based on the average monthly gross sales of a business or average monthly credit card sales. Money can be advanced quickly because securing assets and collateral is not required.

Get clients funded in 4 easy steps; application submission, information review, approval or denial, final review and your client is funded. Minimal documentation is required. The company must have 18 months in business with $7,500 per month in gross sales and an average daily balance of $750. We require a minimum of 5 deposits, monthly into the business bank account.

Funding Stipulations:

- Bank login

- Funding call with merchant

Required Documents:

- Application

- All 2020 business bank statements + MTD

- Signed and dated agreement

- Proof of business existence

- Meets state registration requirements

- Proof of ownership

- Merchant interview

- Driver’s license

- Voided check (starter checks will not be accepted)

With $540 million dollars funded to 15,000 small businesses, Lendini offers incomparable solutions customized specifically for your client. The company prides itself in being able to offer up to $300,000 in as little as 1 business day (in most cases). Funding can be used for any business purpose you may have.

Lendini is not a bank and does not provide loans, they offer cash advances. With Lendini, business owners receive the capital they need without lengthy delays or excessive paperwork. In general, Lendini offers pre-approvals in under three hours and next day funding of approved advances. The staff provides unparalleled customer service and treats each business owner with the respect they deserve.

OnDeck Directors Sued in Class Action For Allegedly Withholding “Material Information” From Shareholders To Make Enova Deal Happen

September 8, 2020 An OnDeck shareholder is asking the Delaware Court of Chancery to halt the sale of the company to Enova until OnDeck discloses allegedly material information that would appear to put the landmark deal in an entirely new light.

An OnDeck shareholder is asking the Delaware Court of Chancery to halt the sale of the company to Enova until OnDeck discloses allegedly material information that would appear to put the landmark deal in an entirely new light.

On September 4, Conrad Doaty filed a class action lawsuit against Noah Breslow, Daniel S. Henson, Chandra Dhandapani, Bruce P. Nolop, Manolo Sánchez, Jane J. Thompson, Ronald F. Verni, and Neil E. Wolfson for breaching their fiduciary duties owed to the public shareholders of OnDeck.

According to Doaty, the Enova offer of $90 million ($82 million stock, $8 million in cash) was not even the best bid that OnDeck received but he alleges that OnDeck’s directors and executives took it because they were individually offered “exorbitant personal compensation” including “millions of dollars in severance packages, accelerated stock options, performance awards, golden parachutes and other deal devices to sweeten the offer.”

Doaty makes reference to other bids for OnDeck with specifics including two all-cash offers, one that valued OnDeck at between $100 million and $125 million and one that valued it at between $80 million and $110 million. He says that no explanation for their rejection was disclosed.

Doaty also alleges that OnDeck relied on two sets of financial projections to evaluate a sale of the company, one for all prospective bidders (that projected a quick economic recovery) and another set that was used only for Enova (that projected a slow economic recovery). Doaty’s point is that Enova’s valuation was based on less optimistic data and that OnDeck did not publicly disclose to shareholders the more optimistic version that all the other prospective buyers of the company got to see.

“Most significantly, is that it is not pressing time to sell,” Doaty says. “The company was not facing imminent financial collapse or financial ruin.” He continues by pointing out that the company had $150 million of cash on hand and that it had successfully navigated workouts with its creditors over issues caused by the pandemic.

“Yet as a result of the frantic and unreasonable timing of the sale, the consideration offered for OnDeck is woefully inadequate.”

In addition to “exorbitant personal compensation” promised to the Board members, Doaty argues that a cheap price benefits parties who sat on both sides of the transaction, namely Dimensional Fund Advisors LP, BlackRock, Inc., and Renaissance Technologies, LLC, all of whom are said to hold greater than 5% beneficial ownership interest in both OnDeck and Enova. None of them are named as defendants.

“…even if the exchange ratio is unfair,” Doaty argues, “those institutional investors will still benefit from seeing their positions in Enova benefitted. Non-insider stockholders, on the other hand, will not be parties to the benefit.”

The law firm representing the plaintiff in Delaware is Cooch and Taylor, P.A.

Case ID #: 2020-0763 in the Delaware Court of Chancery.

You can download the full complaint here.

As an aside, AltFinanceDaily mused two days prior to the filing of this lawsuit that the sales price of OnDeck was so low that early OnDeck shareholders stand to recover less of their investment as a result of this deal than investors in a rival company that was placed in a court-ordered receivership by the SEC.

What Stimulus is Next for SMBs?

September 4, 2020 Next week, lawmakers will finally be back from vacation, arguing over the next stimulus package. There are various proposals, and the two competing Republican and Democrat offerings are nearly a trillion dollars apart.

Next week, lawmakers will finally be back from vacation, arguing over the next stimulus package. There are various proposals, and the two competing Republican and Democrat offerings are nearly a trillion dollars apart.

It’s the Senate GOP HEALs act vs. the House Democrats HEROs act. But in between, what may be getting the most support? Standalone bipartisan bills that focus on extending and forgiving PPP loans.

Ryan Metcalf, head of the office of Government affairs and Social Impact for Funding Circle, has been following conversations on The Hill closely.

“Up until Monday, Pelosi said they weren’t even going to even put a bill forward for a new stimulus,” Metcalf said. “But then yesterday [Tuesday] Secretary Mnuchin said he was open to doing a standalone PPP loan. It’s the one that has the most bipartisan support; they can’t meet anywhere else than PPP.”

Funding Circle is one of the world’s largest online lenders, with about $10 billion in global loans to date. Metcalf said Funding Circle mostly offers US loans in the $25,000 to $500,000 range, and as a funder for PPP, offered more loans in just eight days in August than half of their total business in July. His company had to cut off funding requests, locking out some customers that needed help, simply because the deadline had ended.

“When PPP ended on August 8th, the narrative was that PPP had died out, and there was no interest in it, but that is a complete fallacy,” Metcalf said. “We were processing loans for the smallest of small businesses- 10-15 employees- well under $50,000 loans, the people still needed help.”

Steve Denis, Executive Director of the Small Business Finance Associaton (SBFA), has also been engaged in the process. He has been petitioning members of Congress on behalf of what he calls truly small business, those under 10 employees or nonemployers that still need help.

“‘Real’ small businesses: ones with under ten employees that are really grinding, like small hair salons, retail stores, and mechanics don’t really have traditional banking relationships,” Denis said.

SBA data from July found that most of the loans made (66.8%) were in the $50k range and to very small businesses, but the largest amount of capital went towards firms that applied for a $350k-$1M sized loan.

Denis said that the higher dollar amount PPP loans were more profitable for banks to make, so disproportionate funding went toward bigger businesses with pre-established finance connections. This disparity is backed up by research. Studies, like one from the National Bureau of Economic Research (NBER), found that firms with stronger connections to banks were more likely to be approved for PPP funds.

“The way fees are structured: there’s an incentive for big banks to prioritize bigger deals at [commission] rates like 3% or 5%,” Denis Said. “They’d rather make that on a $500,000 deal than on a $40,000 deal.”

Denis said the SBFA was lobbying for Congress to create a prioritized amount of money authorized only for smaller loans, under $100,000-$150,000, to focus on those really small businesses with less than five employees.

Like Metcalf, Denis sees the most likely outcome is an extension of PPP- at least until the end of the federal fiscal year budget in September. If the Fed cannot agree on a budget, the government will go into shutdown- and this year would be the worst time to shut down.

“The only thing that motivates Congress to move big legislation like this are deadlines; there’s a big deadline coming up,” Denis said. “At the end of September, the fiscal year runs out and there needs to be a budget agreement.”

Metcalf said that the next round of PPP programs need to make sure businesses can get their first loan if they haven’t already, and streamline the loan forgiveness process to keep the SBA from getting overwhelmed.

Metcalf said that the next round of PPP programs need to make sure businesses can get their first loan if they haven’t already, and streamline the loan forgiveness process to keep the SBA from getting overwhelmed.

“We need a forgiveness bill that streamlines the process; lenders will not have the resources to process forgiveness, a first PPP and second PPP as it is,” Metcalf said. “In my call with the SBA two weeks ago, they said for processing new 7(a) lender applications and all the other business they do to resume their normal business we’re looking at six months.”

The PPP proposal that Metcalf likes the best is called the Paycheck Protection Small Business Forgiveness Act, which stipulates a one-page forgiveness form for all loans made under $150,000. Metcalf said he saw support from a bipartisan group of over 90 members of Congress.

Another opportunity is the Economic Injury Disaster Loan (EIDL) program- offering long term loans to businesses with less than 500 employees that need financial help. Both Denis and Metcalf encouraged business owners to check out the program, which offers loans directly from the government without the need to prove forgiveness.

In the end, Denis said he was interested in the Republican “Skinny Bill” that is a cheaper breakdown of the GOP HEALS Act, but he said it is all up in the air.

“This is just me guessing,” Denis said. “I have talked to these people every day, but even members of Congress on Capitol Hill have no clue what’s going to happen.”

Lendini is Back

September 2, 2020 Bensalem, PA –September 3, 2020– Lendini is excited to announce its return to small business funding. Through superior efficiency and analysis, the company has improved the process of alternative funding from some of the brightest minds in finance, technology and analytics. With updated (temporary COVID-19) guidelines, they remain dedicated and committed to their merchants and ISOs in these unprecedented times.

Bensalem, PA –September 3, 2020– Lendini is excited to announce its return to small business funding. Through superior efficiency and analysis, the company has improved the process of alternative funding from some of the brightest minds in finance, technology and analytics. With updated (temporary COVID-19) guidelines, they remain dedicated and committed to their merchants and ISOs in these unprecedented times.

Lendini works directly with you to prepare the best package for your client, whether that be a Business Cash Advance (BCA) or Merchant Cash Advance (MCA). Simply put, Lendini advances money based on the average monthly gross sales of a business or average monthly credit card sales. Money can be advanced quickly because securing assets and collateral is not required.

Get clients funded in 4 easy steps; application submission, information review, approval or denial, final review and your client is funded. Minimal documentation is required. The company must have 18 months in business with $7,500 per month in gross sales and an average daily balance of $750. We require a minimum of 5 deposits, monthly into the business bank account.

Funding Stipulations:

- Bank login

- Funding call with merchant

Required Documents:

- Application

- All 2020 business bank statements + MTD

- Signed and dated agreement

- Proof of business existence

- Meets state registration requirements

- Proof of ownership

- Merchant interview

- Driver’s license

- Voided check (starter checks will not be accepted)

Industries accepted:

- Restaurants (with takeout)

- Pharmacies

- Healthcare

- Manufacturing

- Transportation (freight)

- Healthcare (primary care)

- Automotive repair

- Grocery stores

With $540 million dollars funded to 15,000 small businesses, Lendini offers incomparable solutions customized specifically for your client. The company prides itself in being able to offer up to $300,000 in as little as 1 business day (in most cases). Funding can be used for any business purpose you may have.

Lendini is not a bank and does not provide loans, they offer cash advances. With Lendini, business owners receive the capital they need without lengthy delays or excessive paperwork. In general, Lendini offers pre-approvals in under three hours and next day funding of approved advances. The staff provides unparalleled customer service and treats each business owner with the respect they deserve.

Banks, Non-Banks, Fintech and More Came Through for Lendio on PPP, But it Wasn’t Easy

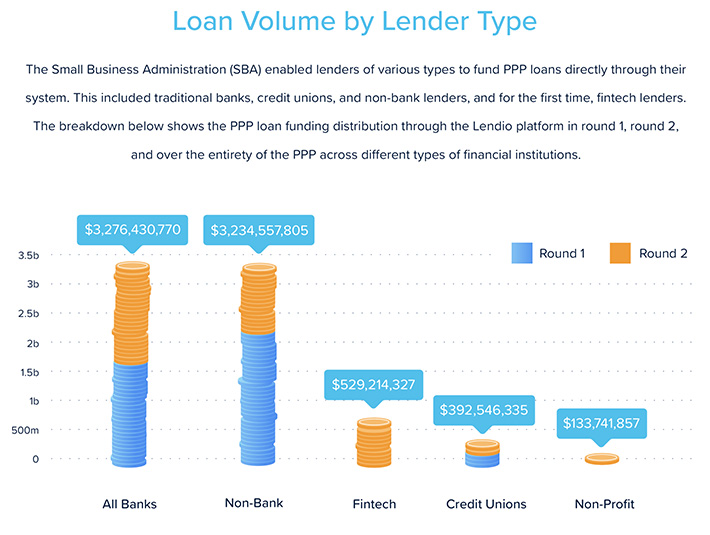

August 27, 2020 Last week, Lendio, a facilitator of small business loans, released a report analyzing the $8 billion of PPP loans that were approved through its lending platform. A coalition of more than 300 lenders was able to give aid, saving an estimated 1.1 million jobs, Lendio indicates.

Last week, Lendio, a facilitator of small business loans, released a report analyzing the $8 billion of PPP loans that were approved through its lending platform. A coalition of more than 300 lenders was able to give aid, saving an estimated 1.1 million jobs, Lendio indicates.

Through Lendio’s service, traditional banks approved the most funding at $3.3 billion- or about 44% of the PPP dollars on the platform. Though non-bank lenders secured the highest number of approvals at 50,264 transactions in lesser dollar amounts.

Fintech lenders funded 6% of the total loan volume through the platform.

Lendio was well situated to facilitate lending from institutions to those that needed help through funds provided by the SBA. Brock Blake, CEO, and co-founder of Lendio, said the company’s success in delivering on PPP was no accident— they had to remove all stops and almost bet on the success of the PPP program.

“Our mission at Lendio is normally ‘Fueling the American Dream’: helping the American business owner accomplish their dream,” Blake said. “We tweaked our mission during this timeframe to ‘Saving the American Dream.'”

Blake said while other companies were closing their doors and sending off employees on furlough, Lendio took on 250 new hires- and buckled down for thousands of hours of engineering work to overhaul their system. Not just loan sales, but legal processes, onboarding, training, and backend tech work had to be updated in just days.

This all came on fast, but so did the quarantine. Beginning in April, more than 100,000 business owners applied for economic relief under the PPP using Lendio’s online marketplace.

The demand for capital was outrageous.

“It was more demand in one weekend than the SBA had seen in the last 14 years combined,” Blake said. “We were helping these business owners that were watching their entire lifes’ work flushed down the drain in a matter of weeks, and they were desperate for capital.”

Lendio was finding that many institutions could simply not handle the volume, Blake said, and he knew if banks were only able to process loan requests for their current customers, there would be an exploding demand for loan processing. The company took on 100 new partners who needed help during this time.

“Our systems were tested to their limits, like 1000 times more pressure than we ever saw before,” Blake said. “Some partners of ours got so much demand they couldn’t handle it and turned off their spigot. So we scrambled to find lenders that would take on new customers.”

Though it was ten times more challenging than anything Blake has done in his career, it was ten times more satisfying. Lendio doubled the number of loans it has issued since 2011, and quintupled the dollar amount the platform facilitated in just four short months. Where are they going to go from here?

For one, Lendio is one company out of many that are hoping for another round of PPP funding. Blake said he is getting customer feedback all the time asking for help, dealing with quarantine regulation that is harming business, like restaurants that have nowhere to seat patrons.

Outside of PPP, Blake said that many of the 110,000 businesses they served are now applying for other loans, or using Lendio’s bookkeeping and loan forgiveness applications. Lendio is happy to help business owners and banks through this tough time by launching digital applications.

“Before, lenders across the country were requiring business owners to come into branches [with] paper applications,” Blake said. “Now, there’s not one business owner in America that wants to walk into a bank branch. The demand for lenders to go digital is as high as it’s ever been.”