No, Corporations Can’t Sue For Usury in New York, Appellate Division Rules

March 25, 2021 Businesses hoping to use the New York State court system to invalidate an MCA or financing agreement, suffered a major defeat on Wednesday. The Appellate Division, Second Judicial Department, ruled that corporations cannot assert usury as a cause of action, even if the allegations meet the criminal usury basis. In deciding this, the Appellate Court was simply affirming what New York’s statute on the matter plainly says.

Businesses hoping to use the New York State court system to invalidate an MCA or financing agreement, suffered a major defeat on Wednesday. The Appellate Division, Second Judicial Department, ruled that corporations cannot assert usury as a cause of action, even if the allegations meet the criminal usury basis. In deciding this, the Appellate Court was simply affirming what New York’s statute on the matter plainly says.

This has not stopped plaintiffs from asserting criminal usury as a cause of action in New York, however, but now such attempts will probably be fruitless.

In May 2016, Global Merchant Cash, Inc. (GMC) entered into a merchant agreement to buy the future receivables of Paycation Travel, Inc. Paycation breached the contract and GMC ultimately filed a confession of judgment. Paycation then tried to vacate the judgment by suing GMC on several grounds including its theory that the judgment was void and unenforceable because the underlying agreement was for a criminally usurious rate of interest.

GMC moved for summary judgment to dismiss the complaint and its motion was denied. GMC appealed the decision insofar as it believed Paycation could not assert criminal usury as a basis for a cause of action.

On March 24, 2021, the Court rendered its decision on the narrow debate in GMC’s favor.

“A transaction . . . is usurious under criminal law when it imposes an annual interest rate exceeding 25%” (Abir v Malky, Inc., 59 AD3d 646, 649; see Penal Law § 190.40). General Obligations Law § 5-521 bars a corporation such as the plaintiff from asserting usury in any action, except in the case of criminal usury as defined in Penal Law § 190.40, and then only as a defense to an action to recover repayment of a loan, and not as the basis for a cause of action asserted by the corporation for affirmative relief (see LG Funding, LLC v United Senior Props. of Olathe, LLC, 181 AD3d 664, 666; Intima Eighteen, Inc. v Schreiber Co., 172 AD2d 456, 457). Accordingly, the Supreme Court should have granted that branch of the defendant’s motion which was for summary judgment dismissing so much of the first cause of action as alleged criminal usury in violation of Penal Law § 190.40.

This decision did not decide the entirety of the case and litigation between the parties is still pending. It does, however, bring conclusive clarity to whether or not corporations can assert usury as a cause of action, even if it’s alleged to be criminal.

The case number is 52579/2017 in Westchester County in New York Supreme Court. The Appellate decision can be viewed here.

NY Court Says MCA Agreement is a Factoring Agreement, Not a Loan

March 22, 2021 A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

In Principis Capital LLC v Team Van Eyk, Inc. et al, Principis sued the defendants over a breach of contract. Defendants “did not deny the facts underlying the motion or the the amount due,” the judge said, “but asserted instead that the Agreement is not an agreement for the purchase of future receivables; but is instead, a criminally usurious loan, and is therefore void as a matter of public policy.”

This defense actually led to victory for the plaintiff.

The Appellate Division, First Department, in Champion Auto Sales, LLC v Pearl Beta Funding, LLC (159 AD3d 507, 507 [1st Dept], lv denied 31 NY3d 910 [2018]) has considered this issue, involving a merchant agreement substantially similar to the agreement in this matter, and has held that the type of agreement involved in this case is a factoring agreement rather than a usurious loan. This court is bound to follow Champion and, therefore finds that the Agreement is a factoring agreement and not, as defendants assert, a usurious loan. There are, therefore, no genuine triable issues of fact, and plaintiff is entitled to summary judgment on its complaint.

Case closed.

Merchant Cash Advance is as Old as The Renaissance

March 21, 2021 The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

In Jakob Fugger the Rich, historian Jakob Strieder writes the Fugger enterprise began as one of the upstart merchant families of the Renaissance. The Fuggers were traders and cloth merchants from Augsburg, Germany. They created a network of aristocratic clients, furnishing weddings and parties through trading warehouses in modern-day Venice, Florence, and Austria. Jakob Fugger I lent some money around, but when Jakob Fugger II joined the family shipping warehouse in Venice, he looked for a better return on capital.

According to International Business History: A Contextual and Case Approach, Fugger entered an agreement to supply some cash- 23,627 Florins to a silver mine owned by Archduke Siegmund in 1487.

Siegmund had plenty of silver laying around for collateral; he just needed cash for the day-to-day. It was a collateral-backed loan, common today: if he couldn’t pay it back, the Fuggers would get paid in silver. The transaction worked so well that a year later, Siegmund reapplied, this time in a revolutionary way. Siegmund would get 150,000 florins, and the Fuggers would get paid the future receivables of the silver mine: unrefined and cheap future silver for cash now.

The problem, written by historian Greg Steinmetz in The Richest Man Who Ever Lived, was the Church. Any interest-based transaction was specifically outlawed, though there were hundreds of lenders during this era. The line from Luke 6:35, “Lend and expect nothing in return,” was taken by the Church to mean an outright ban on usury, defined as the demand for any interest at all.

Even savings accounts were considered sinful, but Venetians ignored these rules as they preferred making money to pleasing God, entombed in the motto “First Venetians, then Christians.” Fugger began accepting deposits like a bank to his clients, with a 5% return to investors.

But convicted usurers could be excommunicated and denied a Christian burial, a nightmare for a capitalist who relied on a Christian network. Fugger did not worry about punishment or the apparent sin of money lending, but as he became a fixture in European society, his reputation became increasingly vulnerable.

Fugger needed the laws to be changed, or at least relaxed, or his lending business was in trouble. In 1515, he wrote a letter to Pope Leo X and funded a debate in the St. Petronius Basilica in Bologna. The debate ran for five hours, a back and forth of philosophy, scripture, and rampant crowd heckling. In the end, it was declared a tie, but Pope Leo X that year signed a papal “bull” reforming the concept of usury.

Originally, the Church pointed to the philosopher Aristotle’s model for determining what was okay to charge for and what wasn’t. Aristotle had said that charging someone for a cow because it produced milk was fine, but money was a dead thing and unfair to profit from.

A silver mine produced silver and as such paying cash for the future proceeds of the mine had allowed Fugger to more or less carry on his business. It wasn’t called merchant cash advance back then but he applied that model wherever he could. Not everyone in need of money had a business, however, and it was critical that he be allowed to charge interest when circumstances called for it.

More than a millennium after Aristotle, Pope Leo X found that risk and labor involved with safeguarding capital made money lending a living thing. As long as a loan involved labor, cost, or risk, it was in the clear. This opened a flood of church-legal lending: Fugger’s lobbying paid off with a fortune.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

McCarthy wrote: That was one of the problems with the Fugger model- “how does one take possession of Austria or France or Spain when its rulers default or lag behind debt repayment schedules?”

After gaining the good faith to lend in the Church’s eyes, the papacy itself became a Fugger customer. Positions in the Church were inseparable from social and political power, and the only way to get a place on the totem pole was by paying for a title. Just as the richest silver mine owners didn’t have the cash to pay for lunch- so did wealthy aristocrats need capital to afford positions in the cloth.

By the time Martin Luther “nailed” his 95 theses to the door of a church in 1517, he was rallying against the Fugger funding family and its stranglehold on the Roman Catholic Church.

It all came down to an in-house promotion. Albert Brandenburg brought a whole new meaning to the concept of “moneychangers in the temple.” A German Archbishop of Magdeburg, Brandenburg was promoted to Elector of Mainz: the second in command of the Holy Roman Empire. Unfortunately, he had to pony up 21,000 ducats to pay the Roman Curia (the Church’s admin)- for the title. Naturally, he didn’t have the cash, and the Fuggers stepped in.

Brandenburg got a loan on interest. To pay it back, he also paid Pope Leo X for the right to sell indulgences. Indulgences were contracts the church sold to forgive sins, allowing believers to purchase their way out of purgatory and into heaven. A fresh round of indulgences was printed to fund the construction of St. Peter’s Basilica, and Brandenburg was entrusted to sell them in 1517. (Their sale was later banned by the Church in 1567).

The sale of indulgences  interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

“I’m saying that there are some specific parts of modern life that derive directly from the Protestant Reformation. We couldn’t have these features if it hadn’t happened.” Ryrie said. “That combination of free inquiry, democracy, and limited government is pretty much what makes up liberal, market democracies. It runs the modern world.”

To this day, no one is sure of the extent of the Fugger fortune. Historian Mark Häberlein found that Fugger struck a deal with Augsburg Tax authorities in 1516: he agreed to pay an annual lump sum on the condition that his family’s true wealth would never be revealed. He died in 1525.

To get an idea of the extent of his wealth, we can base calculations on the cost of butchering a pig in 1522 (yes, that’s a real metric.) It cost one Gulden, a new coin minted in 1500 to butcher a hog. The German coin contained about the same amount of gold as a Florin.

Based on those ham prices, Jim Ulvog from Ancient Finances estimated that in 2017 a single florin would be worth ~$900, and other writers have put the florin in the same range. Though the true wealth of the Fuggers may never be known, when Charles V aimed to take control of the Holy Roman Empire in 1519, the Fuggers were lending Charles 543,000 guldens to buy votes: approximately $448 million. That’s just in a single deal.

It’s been said that merchant cash advances or sales-based financing is relatively new, but it could be argued that such transactions are so old that life as we know it in the modern world only exists because a guy 500 years ago was engaged in non-loan transactions to fund businesses in a manner that was Church-compliant and wanted to expand.

LendingClub Talks Earnings Post Radius-Bank Acquisition

March 11, 2021 “It’s really hard to imagine a better time to be launching a digital bank,” said LendingClub CEO Scott Sanborn on the company’s Q4 earnings call. “First up, we’ll be building on Radius’ multi-award winning online and mobile deposit offering to make it very easy for our customers to manage their lending, spending and savings in a holistic fashion.”

“It’s really hard to imagine a better time to be launching a digital bank,” said LendingClub CEO Scott Sanborn on the company’s Q4 earnings call. “First up, we’ll be building on Radius’ multi-award winning online and mobile deposit offering to make it very easy for our customers to manage their lending, spending and savings in a holistic fashion.”

The company reported a Q4 net loss of $26.7M on $75.9M in revenue and originated $912M in loans. Their status of being a bank, however, is only just beginning. CFO Tom Casey explained the following:

In addition to lowering our funding cost of deposits, our new marketplace bank will capture significant financial benefits from being a bank and having a marketplace. [….]For every $100 million of loans we originate, we generate about $4 million through an origination and servicing fee when we sell the loans in the marketplace. The vast majority of this fee-based revenue is realized immediately and without requiring a significant amount of capital. However, it is highly dependent on origination volume.

[…]

We can now bolster this revenue stream with bank revenue generated by loans held for investment on our balance sheet. As you can see on the left side of the page, every $100 million of loans we hold on the balance sheet should generate additional marginal profitability of approximately $12 million. And when you compare that to the $4 million in the marketplace, that’s 3 times more. And this recurring revenue is not dependent on originations in any given quarter.

LendingClub experienced unique success during the pandemic, stating that loan performance exceeded their expectations.

“Coming out of the pandemic,” Sanborn said, “the strength of our underwriting has now also been cycle-tested. Losses on loans issued pre-COVID are in line with our pre-pandemic expectations, and loans issued since the pandemic are some of our best-performing loans in recent years.”

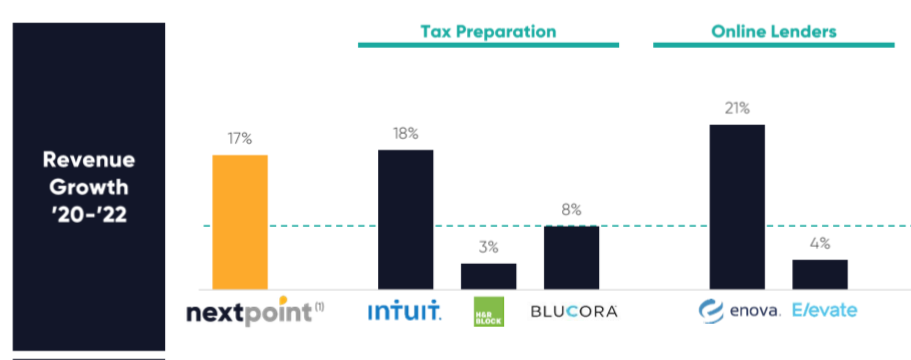

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.

Fintech Lenders Did Better Job Meeting Intentions of the CARES Act, Study Finds

February 18, 2021 Fintech lenders doling out PPP not only reached smaller businesses on average but played an essential role in extending PPP loans to Black-and Hispanic-owned businesses, according to a study conducted by professors at the NYU Stern School of Business.

Fintech lenders doling out PPP not only reached smaller businesses on average but played an essential role in extending PPP loans to Black-and Hispanic-owned businesses, according to a study conducted by professors at the NYU Stern School of Business.

“Fintech lenders originated much smaller loans than other lenders, suggesting they served smaller firms on average,” researchers found. “Overall, we find that, relative to other lenders, [Minority Development Institutions] nonprofits, and fintech lenders make a substantially larger share of their loans to minority borrowers, particularly Black- and Hispanic-owned businesses.”

The team of economists looked over 3.4 million PPP transactions to determine what category of lenders had the highest minority share among their loans. Ryan Metcalf, Head of Public Policy for Funding Circle, member of the Innovative Lending Platform Association (ILPA), shared the full study on LinkedIn, pointing out that six ILPA members had contributed to saving jobs.

“(Funding Circle US, BlueVine, Kabbage, Inc, OnDeck, Fundbox, Lendio) provided more than 476,000 #PPP loans totaling $16.5 billion with an average loan size of ~$30,000, median loan size of $15,000, and helped save more than 2 million jobs,” Metcalf wrote. “And that was just in 2020.”

The study found that fintech lenders did a better job meeting the intention of the CARES act. While most lenders were giving out larger loans to large firms, fintech better reached actual small businesses with smaller loans on average.

“Section 1102 of the CARES Act explicitly specified that the program should prioritize ‘small business concerns owned and controlled by socially and economically disadvantaged individuals,'” they wrote. “However, the SBA did not issue specific guidance for distributing the loans, leaving private financial institutions administering the loans to independently determine which businesses to serve first or at all.”

Instead, as has become clear, many funds went to larger firms and seemed to miss minority communities. The team compared the mean and median loan amounts for different Lenders, finding the smallest in both types were fintech loans.

Researchers put first and last names through a mathematical model to predict race because that data was not available from the majority. Then predictions were compared to the sample borrowers that self-reported race. The algorithm was 78% accurate in guessing black names, 84% in guessing Hispanic, 95% for Asian, and 99% accurate for white names.

Broker in Early Twenties Builds MCA Business in Less Than Three Years

February 10, 2021 Davron Karimov, a 22-year-old MCA broker, went from $10k in debt to collecting $200k a year in commissions. It took less than three years, and Karimov shared his journey on his personal, sometimes chaotic, yet always informative YouTube channel.

Davron Karimov, a 22-year-old MCA broker, went from $10k in debt to collecting $200k a year in commissions. It took less than three years, and Karimov shared his journey on his personal, sometimes chaotic, yet always informative YouTube channel.

The Staten Island native said he first started at a Long Island City shop and quickly made some early deals, eventually leaving to start his own firm, FunderHunt, and recently opened an office in Miami.

But do the YouTube videos help him make deals? Of course they do, Karimov says, and he not only gets deals through his video platform but he also get questions from other MCA brokers who reach out for help.

“Of course, we get people all the time calling in, people that have questions, people in the industry need help with their merchants,” Karimov says. “I started around 2018, and there was no info on YouTube about business funding, a huge void online. I stepped up and thought I could be the one to supply info.”

Nearly three years later, Karimov has built an expanding business while helping others through the struggles of being a broker and CEO in the MCA world. In the last year alone, the pandemic caused applications to explode, Karimov says.

“It’s been better than ever; I’ve never seen so many applications in March and April; they were just soaring,” Karimov says. “And then I’ve never seen so many applications get denied because of the industry at the time everything was shutting down.”

It was a time to capitalize if your shop was strong enough to survive what Karimov called the “dark ages” for MCA. If you survived, you get to reap the reward of a capital-deprived market, he says.

“The whole crisis took out so many funders that were just not good, they probably were supposed to go out of business a long time ago, but this accelerated it,” Karimov says. “It took out all the bad funders and replaced them with people that are solid, fast, and have everyone’s best interest at heart, from the merchant to whoever the ISO is.”

According to Karimov, 2020 solidified who is a real player in the game. Launching a new office himself, Davron says he enjoys sunny days in Miami while it is twenty degrees in-between blizzards in New York. Though snow wasn’t the reason he moved, but instead the funding environment.

“Everyone has been warm and welcoming [in Miami], the government knows what this is, and that’s what we do. We try to educate them: not a lot of people know here about this; it’s like it’s a secret,” Karimov says. “If you go to New York, it’s like everybody knows, there are so many shops there. But here, it’s kind of rare to see someone that knows what a cash advance is.”

Compared to New York’s increasingly restrictive funding ecosystem, the Florida space is open to growth. That’s exactly the environment Karimov hopes to profit from, expanding his business in any way that will be geared toward helping businesses.

“I’m not a huge fan of diversification,” Karimov says. “I like doing one thing. But we opened up an office in Miami; we’re bringing experienced people in and trying to fund deals as fast as possible. We’re maybe looking to develop into offering a debit card, whatever is in the business’s best interest.”

Why Funders Are Investing in Real Estate As Their Side Hustle of Choice

January 25, 2021

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

At that point, Ribeiro’s fledgling company still wasn’t generating much revenue. “I thought, ‘Man, I just can’t get a lot of loans done right now. I only have three or four employees.’ That’s how I got into the real estate industry.” Twelve years later and at the height of a global pandemic, Ribeiro is simultaneously running two thriving ventures —US Business Funding, and a portfolio of hundreds of rental properties he now owns.

At a time when fintech startups and other industry innovators are looking for investors, alternative lending execs like Ribeiro are instead choosing to put their money in real estate to beef up their investment portfolios. Although some execs shy away from talking publicly about their real estate dealings, citing the fact that they don’t want too much exposure, the consensus is that there’s a lot of money to be made in buying, selling and renting property – if you know what you’re doing.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

To Ribeiro, real estate offers a few major advantages: It’s a tangible asset. You can leverage it as it appreciates in value. Deductions make it so you pay very little in taxes. And it offers significant cash flow. “It’s the best investment you can make,” he says.

What makes real estate an especially good fit for alternative lending and fintech execs is that they possess the skills, resources and financial literacy to succeed at it.

“Real estate is a long-term gain,” Ribeiro says. “The industry we’re in is a cash-flow cow. People who are doing well are printing money. But what can you do with that money? You can put it in the stock market, but you won’t control much. Then you pay capital gains on it.”

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

“If you’re a cash advance guy and COVID happened, then you’re not doing very well,” he says. “If you diversified your assets by doing real estate and cash advance, you’re able to weather these downturns a lot more easily than you would otherwise.”

Rianda has not yet counseled any of his own cash advance clients on real estate matters. But based on his insights from working with both areas, he says real estate would be a logical move for MCA executives, and he’s seen some of his clients in the bankcard industry buy up properties.

“One of my clients had a portfolio of merchants and sold it for a few million, then flipped over to real estate. So it’s a means (to an end),” Rianda says.

‘Snowball effect’

Ribeiro has relied on a simple strategy to steadily build his portfolio of residential properties: Buy. Fix. Leverage. Repeat.

“I feel like the portfolio is doubling every couple of years. It’s just a snowball effect,” he says.

After Ribeiro buys a home, he waits about six months before he has it appraised and fixes it up in the meantime.

“If you go to the bank within the first six months of purchasing it, they’re going to give you the actual market value of whatever you purchased the house for,” he says. “If you wait six months, they’ll reappraise the home and give its true market value, which could be another 40, 50 or 60 percent. And so now you’re going to have a lot more equity in the house, and you’re going to get a lot more money when you leverage that home to go buy the next one.”

Ribeiro says he sees lots of people making the mistake of buying a home, and then going to the bank a week or two later for a loan.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Depreciation refers to one of the key tax benefits of real estate. Since owning a rental property is technically a type of business because it generates income, the property is considered a business asset. The IRS allows you to deduct the cost of acquiring that asset – the property – over the span of its useful life. For residential properties, the IRS sets a standard depreciation period of 27.5 years.

So if you buy a $100,000 property with a $20,000 land value, $80,000 of the asset is considered depreciable. Over the course of 27.5 years, you can take an annual deduction of just over $2,900 a year.

The trick, Ribeiro says, is to stick to lower-priced properties with an 80/20 home-to-land value. Most of his properties are single- and multifamily homes between southern California and Las Vegas.

Like Ribeiro, Rianda’s investor clients concentrate on one geographic area to find the best properties. “They look at the area for a long time, understand the area,” he says. “In my neighborhood, three blocks can make a 50 percent difference in the price of a house. You need to focus on a particular geographic area and do a lot of transactions in it.”

Small portfolio, big impact

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

“For me, it’s just a really good second income stream and a way to have a secure return of 4.5% to 6.5% a year,” he says.

Growing up, Weitz got a feel for real estate by watching his uncles invest in multifamily properties. At one point, Weitz’s uncle owned 15 different multifamily homes, and Weitz would help do the maintenance on them.

Eight years ago, Weitz invested in his first two-family home and has fixed and flipped eight properties since then. He currently owns two two-family homes and invests primarily in multifamily homes in Long Island, Brooklyn and Queens. Over the next five years, he plans to pick up at least two more four- or eight-family properties. Working with a small portfolio of residences in his home state has allowed Weitz to have full control over managing his properties and to turn a good profit.

“I think for me, it just offers more liquidity,” he says. “It’s an asset I can sell and liquidate at any time. That’s really important for me.”

Ideally, Weitz would like for his investment to build generational wealth that he can pass down to his son. With many people in the U.S. unable to qualify for mortgages, Weitz sees real estate investing as an opportunity to help the economy by giving renters a place to live and put down roots. “Depending on the neighborhood, you can put yourself in a situation where you have good renters for 20 to 30 years. They want to raise their families and have their kids grow up there,” he says.

Litigation among the pitfalls

Even though Ribeiro has had success with his business model, he cautions that there’s considerable risk involved with real estate.

“I love the industry. It’s a passion. It’s beyond my wildest dreams of the size of the portfolio and how well it performs,” he says. “But don’t think it’s all cupcakes and unicorns. There’s a lot to the madness. That’s why not everyone can replicate the model.”

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

As an attorney, Rianda says his real estate clients call on him not just for the purchase of the property, but for various issues that occur during the ownership period.

Here’s one scenario: A property owner has a tenant who isn’t paying rent, so the property owner sues the tenant. But while the lawsuit proceedings are under way, the tenant declares bankruptcy, which puts a stall on further litigation.

“There are people who understand the system and can make it difficult for you to get them out (of the property),” Rianda says, adding that it’s important to have legal counsel readily available. “You need someone who has really done this a lot and knows how the system works to get that person out of the rental property as quickly as possible.”

To minimize liability, Ribeiro has divided his properties into about 10 different business entities – each with a separate umbrella insurance policy.

Rianda sees his own real estate investor clients follow this strategy by grouping multiple homes under the name of an LLC. “If you personally own all these various assets, there’s the potential that if something catastrophic happened at one, it could bleed into all your other properties and potentially put them at risk,” he says.

Dual careers

Ribeiro’s real estate investments and finance company both serve as full-time occupations for him. Some years, he’ll focus more on one area than on the other, depending on market conditions. He spent more time on real estate between 2008 and 2013; then his business needs flip-flopped when real estate prices started going back up. This past year, he’s directed more attention to the finance company because of COVID, which necessitated some operational changes and a need to help clients who had been trying to get PPP loans. But he’s also started investing in commercial real estate, which has taken a hit because of companies forgoing office space to save overhead costs while employees work remotely.

Ribeiro expects to start seeing more mortgage defaults on lower-level homes in 2021 and 2022, after forbearance periods are over. And he’s been leveraging his assets to start buying more properties around the second quarter of the new year. “I think it will be a good time to start buying heavy again,” he says.

An attractive investment vehicle

With the pandemic weakening business portfolios, secondary investment options might sound like just what the doctor ordered.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

“As time goes on, I’m starting to see my clients go back into their lending,” Rianda says.

Even as clients start to recoup their business, Rianda sees the wisdom in other investments and says cash advance executives are well suited for real estate. “It’s just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” Rianda says. “It’s something I find that people who are doing well in their business do, regardless of what business they’re in. So cash advance guys are just following the things people have done for years.”

Ribeiro cautions that people who get into real estate should look at it as a 10-year investment minimum, and not just a two- or three-month stint.

“It’s not a lottery ticket, and it’s not an overnight race,” Ribeiro says. “This is a long-term gain. But it’s a very lucrative gain from a cash-flow perspective and a tax perspective. I don’t think there’s a more attractive vehicle than real estate.”