Is NAMAA Reborn? Meet the Small Business Finance Association

April 14, 2015Almost seven years ago exactly, the North American Merchant Advance Association announced their presence. As of today, they are now officially the Small Business Finance Association (SBFA). Back then, a release dated April 15, 2008 stated:

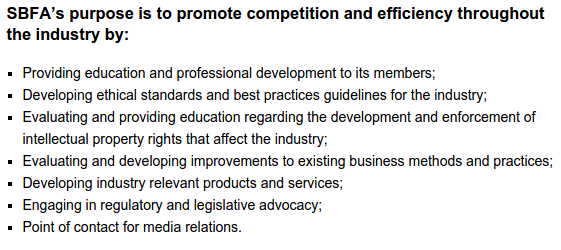

The North American Merchant Advance Association, Inc. (NAMAA) has recently been created to represent merchant cash advance providers and to promote competition and efficiency throughout the merchant advance industry. NAMAA’s members will have the opportunity to share industry education and professional development, ethical standards and best practices guidelines, the development of industry relevant products and services, and the engagement in regulatory and legislative advocacy.

Of the ten original members, a handful are no longer operating. NAMAA’s membership in 2008 arguably encompassed the entirety of the merchant cash advance industry sans AdvanceMe (now named CAN Capital). Today, the SBFA website currently lists seventeen members. The organization has clearly grown but it pales in comparison to the size of the industry in 2015.

Internal data indicates that there are well over one hundred direct providers of merchant cash advance. Several hundred more are ISOs/brokers that co-invest in merchant cash advance transactions (Strategic Funding Source has had more than 200). And there are more than one thousand ISO/brokers that resell the product nationwide.

On this basis alone, less than two percent of industry providers and resellers are members of the trade organization. Granted, the seventeen member companies likely make up at least 15% of the industry’s funding volume. Member company Merchant Cash and Capital for example, announced just last month that they had funded $1 billion since inception.

Some have viewed the organization’s membership as overly exclusive and resistant to change. A seasoned veteran of an ISO that wished to remain anonymous said prior to the organization’s announced changes that, “NAMAA served a purpose for a long time but as the industry has changed, they have not.”

Ironically, Goldin’s statement in today’s release couldn’t be any more well timed. “With the alternative financing industry growing exponentially into a multi-billion dollar industry, we felt it was time for the trade association to evolve with it and open itself up to all types of small business alternative financing providers hence the name change to Small Business Finance Association,” he said.

The shift clearly acknowledges the true dynamic of the industry’s growth, that it’s not all merchant cash advance anymore.

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

But with lenders added to the mix of potential constitutents, is the SBFA a little light? The SBFA will now represent less than 1% of the companies selling or reselling merchant cash advances and business loans. In growing membership however, patience may perhaps be a virtue.

Jared Weitz, CEO of United Capital Source, said, “NAMAA is a beneficial association in the industry and should be choosy with who they let in.” As a broker, his company has historically not been eligible for membership.

Similarly, Chad Otar, Managing Partner of Excel Capital Management, whose company has also not been historically eligible for membership, said, “The aim of NAMAA is to help out our audience to understand and remember the information we stand for as funders and ISOs.”

Otar’s point belies a troubling trend, that many players in this industry disagree about what it is they stand for.

In a AltFinanceDaily Magazine article, titled, Stacking: Is it Tortious Interference?, Robert Cook, Cathy Brennan, and Kate Fisher of Hudson Cook, LLP delved into the industry’s most polarizing debate, the practice of entering into a cash advance transaction or loan knowing that the merchant has one or more open cash advances or loans with a competitor. They wrote:

On one side are companies that only originate first-position deals. These companies generally include a clause in their contracts prohibiting the merchant from obtaining another merchant cash advance or loan until the company receives all of the future receivables it has purchased or is fully repaid. First-position companies view stacking as a threat to recovery of money advanced or loaned to merchants. On the other side are companies that routinely offer second or third-position deals. These companies argue that merchants with adequate cash flow to support additional advances should be free to obtain them.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Lawyers at Hudson Cook, LLP echoed the same. “In the last several months, at least two first position companies have sued their stacking competitors, claiming that stacking constitutes tortious interference with contractual relations,” they wrote.

The lawsuits come on the heels of the International Factoring Association (IFA) ban on merchant cash advance companies, citing tortious interference as the main driver.

After meeting with board members from both associations, the decision was made to deny membership to merchant cash advance businesses. This decision was based on numerous complaints and increased scrutiny that could negatively impact the factoring industry. By distancing ourselves from the merchant cash advance industry, we hope to diminish the chance of potential legislation.

-Commercial Factor July/August 2014

With several merchant cash advance companies left high and dry by the IFA, a potential leadership void has been created.

“As every industry evolves and shapes itself, some sort of governance and guidance is always needed,” said Otar. “This guidance is something that NAMAA holds itself responsible for,” he argued.

“The question is, can they reestablish themselves as a powerful voice that demands respect?” asked an industry veteran on the condition of anonymity.

Goldin assured me that the updated version of the organization’s best practices guide will be a public document.

Industry brokers like Otar are eager to comply with an established code of conduct and play any role they can in its creation. “Most of the business driven industry-wide is brought in through various ISO channels, which are the ones responsible in presenting the product offered by the funders to the end client,” he said.

That enthusiasm may be resonating with the SBFA. Goldin communicated that they are working towards different types of memberships, hinting at the possibility that brokers might one day be extended an invitation to join.

“We are exploring different levels of membership / pricing,” Goldin wrote in an email.

For the right price, they will likely find a lot of eager applicants.

Strategic Funding Source Names Stephen Lerch Chief Financial Officer

March 10, 2015NEW YORK (March 10, 2015) – Strategic Funding Source, Inc., a New York City-based provider of financing options to small and midsize businesses (SMB), today announced that Stephen E. Lerch has joined the company as Executive Vice President and Chief Financial Officer.

In this role, Lerch will be responsible for all aspects of the company’s financial operations, including enhancing fiscal capabilities, identifying new investment opportunities and executing growth plans. He will report to Strategic Funding Source Chairman and CEO Andrew Reiser.

With more than 17 years in various C-suite roles with technology-based companies in both the public and private sectors, Lerch brings an extensive range of expertise in finance, revenue generation and operations management to Strategic Funding Source. Most notably, he is a veteran of the small business finance and marketing industry, having worked for more than seven years as CFO and COO of Rewards Network where he helped pioneer the early successful growth of the alternative lending marketplace. Prior to that, Lerch was a Partner at Coopers & Lybrand, now PwC. He is a graduate of the University of Notre Dame.

“We are thrilled to welcome Steve to the Strategic Funding Source team,” said Reiser. “With his immense financial, operational and industry specific experience, Steve will play a key role in advancing the way we do business and drive the company’s growth.”

“I am extremely pleased to be joining Andy and the talented management group at Strategic Funding Source,” Lerch commented. “With the best reputation in the industry, the premier underwriting and syndication platform and an excellent equity partner in Pine Brook Partners, Strategic Funding Source is extremely well-positioned to take advantage of the tremendous growth opportunity already underway in small business financing.”

About Strategic Funding Source, Inc.

Strategic Funding Source finances the future of small businesses utilizing advanced technology and human insight. Established in 2006, the company is headquartered in New York City and maintains regional offices in Virginia, Washington state, and Florida. The company has served thousands of small business clients across the U.S. and Australia, having financed over $800MM since inception. Visit www.sfscapital.com to learn more about Strategic Funding Source, its financing products and partnership opportunities.

Revenue Recognition for the MCA Industry

March 1, 2015This is question #6 in a 6-part interview series about Merchant Cash Advance Accounting between AltFinanceDaily’s Sean Murray and Yoel Wagschal, CPA and Christina Joy Tharp.

- 1. Merchant Cash Advance How to Guide Intro

- 2. Do I Need a Special MCA Accountant?

- 3. and 4. Recording Merchant Cash Advance Transactions on the Books

- 5. Merchant Cash Advance Accounting Pitfalls

- 7. Q&A – Real questions that MCA companies or syndicators have

Q: How should funders record revenue?

A:

The accounting of MCA companies must not show their transactions in a way that cash advances can be seen as loans. As we all know, a lot of people in the law enforcement community wish to compare MCAs to lending companies. They would like to conclude that MCAs are lending money at a higher interest rate than is currently allowed by law.

The accounting of MCA companies must not show their transactions in a way that cash advances can be seen as loans. As we all know, a lot of people in the law enforcement community wish to compare MCAs to lending companies. They would like to conclude that MCAs are lending money at a higher interest rate than is currently allowed by law.

When our firm speaks to clients in the MCA industry who continually use the loan method of accounting, it makes our firm very nervous for them. We see that MCA companies are unwittingly affirming what those law enforcement communities want to allege.

By keeping your accounting books on an established lending method of accounting, you are setting up your company for lawsuits while simultaneously setting up the industry for scrutiny. There is one thing we all must agree on: MCA companies must strive against accounting procedures that will ultimately classify them as loan sharks. If an MCA company is unsure as to how to set up their accounting so as to reflect MCA standards, please contact a knowledgeable CPA who can guide you appropriately.

In general, revenue is recognized when a specific critical event has occurred and when the amount of revenue is measurable. Every American business recognizes revenue and gains when goods and services, merchandise, or other assets are exchanged for cash (or claims to cash). However, there are a number of issues with the old US GAAP way of revenue recognition, especially for MCA companies.

A lot of companies are struggling in their attempt to establish the right path for their specific industry. What happens is that certain companies in the same industry conclude differently than other companies and this leads to inconsistencies in reporting. This is why the accounting standard setters now feel a need for new revenue recognition standards. As most accountants are aware, the new standards will be put into practice over the next two years.

Unfortunately, although the new standards reach a wide variety of industries they have not specifically addressed the MCA industry. The MCA industry has its own challenges in accounting for revenue, specifically the ‘right’ way to account for purchasing future sales. Whenever the topic comes up it soon turns into a hot debate regarding how and when to recognize revenue.

Going into all of the nuances would be too complex and truly each side of the argument may have merit. The real issue is when revenue should be recognized. One option is to recognize revenue at the time of funding. The other option is to recognize revenue on an ongoing basis (pro-rate when funds are being collected).

Here we will go back to our initial example and show the difference between the two options. All we need to change is journal entry C and journal entry D.

Here are the original entries, which show immediate revenue recognition:

| Accounts | Debit | Credit |

| Accounts Receivable | $100,000 | |

| MCA Cash | $70,000 | |

| Revenue | $30,000 |

| Accounts | Debit | Credit |

| MCA Cash | $1,000 | |

| Accounts Receivable | $1,000 |

Here we use the deferred method, which show ongoing revenue recognition:

| Accounts | Debit | Credit |

| Accounts Receivable | $100,000 | |

| MCA Cash | $70,000 | Deferred Revenue | $30,000 |

| Accounts | Debit | Credit |

| MCA Cash | $1,000 | |

| Accounts Receivable | $1,000 | |

| Deferred Revenue | $300 | |

| Revenue | $300 |

There are two other methods, both of which are completely incorrect and both of which our accounting firm has seen in use. The first incorrect method is when revenue is only recognized at the end – when the contract is completely paid off. This method could get your organization into real trouble. For instance, what if the contract is renewed? In those terms, a contract could renew over and over and the MCA company would never recognize the revenue. This could lead to the IRS charging you (even criminally) for tax evasion.

The second incorrect method is the loan method. This method calculates each payment’s interest and principal (similar to a conventional loan). As we outlined above, using the loan method of accounting only sets your MCA company up for scrutiny and legal action. Your own books could be used as evidence to show that your company is violating usury laws.

In conclusion, if it looks like a duck, quacks like a duck, and swims like a duck – it’s a duck! Be sure your accounting books do not paint the portrait of a loan company. Simply calling yourself a MCA company is not enough – you must be a MCA company through and through.

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.

The Industry’s Bad Paper

February 8, 2015 Sometimes deals go bad. But what happens next?

Sometimes deals go bad. But what happens next?

I just finished reading, Bad Paper: Chasing Debt From Wall Street to the Underworld on a recommendation from a friend. In it, author Jake Halpern walks readers through the shadowy world of consumer debt collection. It was eye-opening to say the least.

Halpern’s research uncovered that consumer debts with seemingly no original paperwork is sold, resold, and resold again to companies that the debtor never heard of and would not recognize. A debt’s record amounted to some fields on a spreadsheet where the information is not always correct and might even have been collected already by someone else.

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

I’ve found that a lot of my defaulted loans thus far have gone bad in the first few months, a pattern that looked more like fraud than borrower hardship. It actually prompted me to call Lending Club and speak to a representative about it, who explained that they’re doing all they can to prevent fraud.

They were pretty relentless on this particular file, a nurse that was making $60,000 a year sounded like a winner. They had virtually no debt but the loan was supposedly used to consolidate outstanding debt into one monthly payment at the rate of 9.67%. The story didn’t exactly add up but since I don’t actually get to talk to the borrowers or look at their paperwork, I’m essentially just playing a numbers game.

That debt has been sold off and I as a note holder do not appear to be entitled to any money on the sale of it, not even pennies on the dollar. Bummer.

Because of platforms like Lending Club, I wasn’t the only one to lose out. 277 other retail investors who I don’t know and have never met participated in it with me. We’re all playing the numbers and we lost on this one.

With 1907 notes acquired on the platform so far, I’m not emotionally invested in any of them. How can I be? I have no idea who the borrowers are. I don’t even know their names! All I can do is diversify and make decisions based off of statistical analysis. If the borrower stops paying, go after them hard whoever they are!

Meanwhile in commercial transaction land

When it comes to merchant cash advance and business lending, the collection rules are different but so are the relationships. Even with strong advancements in automation, phone interviews remain an integral part of the underwriting process. A risk analyst typically calls the business owner, their landlord, and even several of their suppliers. Large dollar amount deals may even be presented to an entire risk committee for approval.

Suffice to say, pesky things like signed contracts do not usually prove elusive when a collector in this world gets their hands on it. Many commercial funding providers even record phone calls with the business owners where they get an additional verbal confirmation to the terms and conditions of the arrangement.

The collections process usually begins with the sales person or sales office that negotiated the terms with the business. Back when was I was an account rep, my commissions were paid in two pieces, upfront and a residual. That meant almost half my pay on a deal was tied to its performance. If a deal started to fall apart or defaulted, I had a personal stake in restoring the business to good standing.

The Fair Debt Collection Practices Act does not cover commercial transactions. And in the case of traditional merchant cash advances, there is likely no debt at all in a default, but rather a possible case of stolen receivables.

In the event where a deal I brokered was suspected of diverting receivables, I’d be the first one to know about it and the first person tasked with fixing it. That meant calls to the business, their home phones, their cell phones, and when necessary their landlord. If none worked, then their suppliers. The first goal was to determine if the business was still operating and in the vast majority of cases where defaults happened, they were.

Hardship was sometimes cited as a reason for breaching the agreement but not always. With a chunk of my paycheck on the line, I had to talk them back into good standing and unlike debt collectors, I didn’t have the ability to renegotiate the terms, lower a payment or cut them slack. It was back to the way it was or nothing.

It escalates

Some returned to good standing and others played hardball. The deal’s original underwriter might then involve themselves and if they failed, then on it went to the internal funder’s portfolio management/collections team.

This is why the situation here on out is different: Imagine a doctor sells you the accounts receivable of all his patients for a discounted price. The doctor gets cash upfront and the buyer will hopefully collect the full value of the accounts receivable to earn a profit.

Now imagine the doctor accepts your cash upfront and then also collects the accounts receivable from the patients and shuts you out. In traditional merchant cash advances, collectors aren’t going after debt, but rather acquired property that is rightfully theirs. The business has shut them out of receivables they purchased.

If internal collection efforts fail, they can attempt to freeze various receivables the business might have. Merchant processing proceeds are usually the first stop. If the business accepts credit cards, the merchant processor can be instructed to freeze all or a percentage of the revenues without a court order. This is easier said than done but it does work and there are even a few third party collection firms that specialize in this.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

Some business owners are shocked to learn that a deal they made over the phone with people they never met will actually track them down and sue them. Unlike consumer debts which might only be a few hundred dollars, commercial transactions are typically tens of thousands or hundreds of thousands of dollars. They will definitely pursue it.

On the largest default I ever presided over as an underwriter, the business owner said something to the effect of, “I stole your money. Let’s see how good you are at getting it back.” He said this just 24 hours after we had wired him the money. Ouch!

That happened more than six years ago but it was something I’ll never forget. A quick Google search today reveals that guy is still alive and kicking as he was recently interviewed about his success in amassing a restaurant empire in Florida.

Over the next couple years, I would hear variations of that “I stole your money” line from other businesses, typically on deals larger than $75,000. These were strategic defaults designed to strong-arm the funding company into a settlement or an attempt to simply walk off with the funds altogether. In other words, fraud.

All this does is raise the cost for the next business that conducts themselves honestly. It’s a damn shame.

Merchants prey on Wall Street

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

One experience I had was with the owner of a steakhouse in NYC that flew up from his residence in Brazil to try and close me (as the underwriter) on purchasing roughly $400,000 of his future credit card sales. What he didn’t know is that the night before I checked out the place anonymously by having dinner there with my wife. When the bill came, the server told me they no longer accepted credit cards. The next morning, the owner who spoke only in Portuguese arrived in tow with a translator and a lawyer. They traveled directly from JFK to our office, to which I informed them of the decline. They had stopped accepting credit cards a day too early for their scam on us to work and the restaurant closed two months later.

In another case, a souvenir shop in NYC asked if I would come by to pick up his application and statements in person since we were locally-based. After spending a half hour with the guy at his shop, I returned back to the office only to find out that he gave me doctored bank statements.

And then there’s the owner of a florist that made a career off of robbing merchant cash advance companies. The store, which is close to my hometown, had obtained more than 20 merchant cash advances by late 2008 and defaulted on all of them, netting the business close to $1 million. They hoped to make me victim number 21 but we figured it out in the 11th hour before the funds went out. The business is still there today though I’m unsure if it’s still the same owner.

In 2015, fake documentation is an epidemic. Underwriters in the industry cannot rely on faxed or emailed statements alone. They should be verified through APIs or through direct contact with banks. Many funding providers go a step further and actually request the usernames and passwords to business bank accounts just to be absolutely sure that what they’re seeing is what they’re getting.

But as tech-savvy millenials become the face of American small business, the ante is being upped on fraud. One underwriter told me they saw something even more worrisome, a fake bank website.

The scam is this: Knowing the underwriter is going to request the username and password of the business bank account to verify the statements, the applicant has designed a functional replica of a bank website on a web domain they own, one that looks like the bank name. The unsuspecting underwriter logs in to it and verifies the account data. There’s only one problem, it’s all fake.

While this appears to be an isolated event, it just goes to show that the war on bad paper is entering another phase.

Bad paper

While fraud is a substantial cause of the bad paper in the merchant cash advance and business lending industries, hardship does have its place. It is perhaps fortunate that in the commercial space, the paper isn’t sold off into some convoluted world of debt collection. More than likely the business will be dealing with the actual funding provider the entire way through the collections process, not a debt buyer ten levels down the chain. That’s good and bad for them.

It’s good because the owner will able to discuss matters related to the default with the party directly familiar with the original contract.

It’s bad because any chance that the contract and proof of the agreement will somehow get lost in the shuffle is pretty much nil.

Jake Halpern discovered that debtors can win lawsuits by simply challenging the debt buyer to produce evidence the debt is owed. That might work in the consumer world where debt changes hands ten times. On the commercial side, bad paper is an enduring companion. It may be business-to-business but somehow it’s more personal.

Contrast that with the Lending Club nurse who I know only as Member XXXXXXX. His/her debt is in the wind. I have no idea who they are, nor anything about the 277 other people that invested with me.

Halpern spent 256 pages tracing the path of a debt, the companies that bought it, sold it, stole it, and sued for it. It’s amazing how complex it is.

If he were to do a book on bad paper in merchant cash advance, it would go like this:

The business defaulted, the funding provider tried to collect and then sued. The End.

Heather Francis Launching New Funding Company

January 5, 2015 One of the Six Women of Alternative Finance is leaving their current position to launch their own funding company. Heather Francis, EVP of Merchant Cash Group appeared in the September/October issue of DailyFunder. A regular at the industry’s conferences and who was in many ways the face of Merchant Cash Group, Francis is moving on to start Elevate Funding.

One of the Six Women of Alternative Finance is leaving their current position to launch their own funding company. Heather Francis, EVP of Merchant Cash Group appeared in the September/October issue of DailyFunder. A regular at the industry’s conferences and who was in many ways the face of Merchant Cash Group, Francis is moving on to start Elevate Funding.

When the news broke, AltFinanceDaily asked Francis about the change. This was her response:

“So the start of the new year begins with something exciting for me as I will be leaving Merchant Cash Group to pursue heading up my own funding company. Elevate funding is still in the set up stages and will not be operational and funding until Mid February but I can assure you that with each unveiling of what we will be funding and what we will offer to the Alternative Industry as well as the business owners will help shape a new future. I enjoyed my time at Merchant Cash Group and I wish them all the best but I am excited for this new adventure and to take a lot of the ideas that have been kicking in my head for a while and see them come to fruition. I know it will be difficult and I am greatly looking forward to the challenge. In the words of a Fort Minor song : This is 10% luck, 20% skill, 15% concentrated power of will, 5% pleasure , 50% pain, and a 100% reason to remember the name… Best of luck to all in 2015!”

Elevate will be based in Gainesville, FL.

The Funding Calls That Won’t Stop

November 23, 2014“Your business has been approved for a loan…”

Last week, Chicago Public Radio (WBEZ 95.1 FM) investigated a trend in the small business community, the use of merchant cash advance financing. The station called me in advance to answer some questions about merchant cash advances and I gave my best explanation of the industry and its products.

Of the discussion that lasted more than 30 minutes, only about five of my sentences made it on the air. While I clarify some of my positions below, it was sobering to learn the context of how they were used, as a defense to real life merchant complaints.

The satisfaction rate with merchant cash advances are pretty high and I say that mainly because it’s so rare to hear complaints from anyone other than journalists that can’t believe anyone would accept rates above 6% APR. And while there are indeed bad actors in the industry (as there are in any industry), the gripe one merchant had about phone solicitations that just won’t stop is a recurring theme.

It’s happening to me too.

As an account representative in 2010 calling real time leads sold to five parties at once, I did what anyone would do, I pretended to be a small business myself and inquired through the website that we bought leads from and entered my cell phone as the point of contact

Ring. Ring. Ring…

Within a half hour, representatives from four companies called me, and I learned exactly who my competition was, how they explained the product, and what they would say to win me over. Two of the four were really good and one even referenced my name personally, saying something to the effect of, “If you get a call from Sean Murray, his rates are worse than mine.” Obviously he had already done what I was doing now, which was pretend to be a small business so he could prove to the prospect he was well informed about the alternatives. He had heard my pitch already and was now throwing me under the bus by planting the seed that I was going to offer something more expensive even if it wasn’t the truth.

In the end none of them won because it was all a farce. One never called me again after the first call. Another kept at it for a week and the remaining two followed up for a month.

And then it got quiet…

I had been marked as a dead lead and forgotten about until three months later when one company sent a follow up email. “Smart,” I thought. But then a call came six months later, and then more emails, some from companies I didn’t originally engage with.

And they continued at regular intervals, every couple of months an email or call. Was it interesting? Yes. Annoying? No.

Until this year.

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The press 9 option doesn’t work for me. Sure, I might be removed from that marketer’s list, but it in no way removes you from anyone else’s list. I knew that already of course because I’ve been on the other end before.

The first time I got one of these calls, I was excited to tell the sales representative who I really was, level with him, and explain that it was a really good idea to take me off the list. But much like other business loan robo call complaints, the representative wouldn’t tell me anything about himself or his company.

I got yelled at.

Every time I tried to ask a question, he’d get louder, insisting I tell him my monthly gross sales volume for the “cash advance I wanted.”

A rogue actor maybe, but I’ve since gotten additional business loan robo calls and have made no progress in getting myself removed. I just hang up now.

Call it sweet irony perhaps. Or maybe a wake up call (pun intended). I applied on a website once four years ago and the rest is history.

My experience with repeat solicitations is marginal compared to somebody that has actually used a merchant cash advance. With the filing of a public UCC-1, anyone in the industry can easily access that data and convert it into a marketing list. And they do.

Brokers that scorn UCC marketing acknowledge that these businesses could be getting called 5-10 times a day. My own clients had reported repetitive calls back when I was an account representative. And while UCC marketing is very cost effective, in today’s market where more than a thousand companies are offering similar financial products, it’s probably safe to say it’s overly saturated.

And if 5-10 calls per day were even remotely accurate, I’d surmise that level of volume is marring the industry’s reputation as a whole.

I could argue though that when customers have a great many options to choose from, they win. With more than a thousand companies offering merchant cash advances and business loans, it’s truly a buyer’s market. Play all the companies against each other and you should end up with the best possible terms. It’s a great time to seek capital.

Except we’ve got to do something about those phone calls, or at least the robo calls.

Every angry robo dial recipient becomes one less person likely to speak positively about the the nonbank financing industry. Aged leads, UCCs and phone calls might be inexpensive, but the cost to undo negative preconceived notions is immeasurable.

Do you want to be known as the company that helped small businesses or the annoying people that won’t stop calling? If merchants are taking to the air waves to complain, it will only be a matter of time before the FTC and FCC become interested.

—

Regarding my comments on the radio about APRs and daily amortization, they were pulled from a conversation that compared daily payment loans to purchases of future sales. I DO believe bad actors exist and every business owner should have an accountant, lawyer, or savvy third party review any contracts they enter into, financial or otherwise.

Industry Takes ALS Ice Bucket Challenge

August 24, 2014Have you been nominated to take the ALS ice bucket challenge yet?

Kabbage below:

Their video made the local Atlanta news.

OnDeck in Times Square NYC:

Noah Breslow, their CEO also did it:

Funding Circle:

PayPal

Coincidentally, in the industry’s 2012 fantasy football competition for charity, league winner Sure Payment Solutions chose to donate all funds raises ($7,100) to the ALS Association.

Whether you get nominated or not, you can donate at http://www.alsa.org/.

Feel free to tweet @financeguy74 if you or your company accepted the challenge. 🙂