LOOP Brings Real Tech to Auto Insurance

October 6, 2021 LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

“We get rid of all the stuff that doesn’t matter in pricing [customers],” said John Henry, Co-CEO and Co-founder of LOOP, when explaining how the ways traditional insurance companies price their customer’s rates. This is where LOOP separates themselves from the pack. Things like credit scores, education, and income are not considered when pricing out their customer’s rates according to Henry, rather it’s how and where they are driving that determines the cost of insurance.

As an [Managing General Agent] MGA, LOOP underwrites its own risk and chooses the services they partner with to operate their claims. “This is not some digital brokerage or a quoting engine,” said Henry. “When you are insured by LOOP, it’s our actual product you’re insured by. We don’t sell any other products, we don’t sell leads, we are in the business of insuring people.”

LOOP will provide information to its customers that enables them to improve their driving and decrease their future rates. They will send customers tips on where and when to drive, and how to drive if they are driving erratically via a phone-based app. Their initial rate is based on population-level statistics from the respective area, and their personalized rate is a standard 6-month premium, meaning that the monthly rate won’t change month-to-month based upon how customers drive at certain times.

“We have millennials encumbered with student loan debt, we have immigrant populations with consumer loans, baby boomers selling their homes and losing their home and auto bundles, and the realities of the post-pandemic era means that we need more flexible and contemporary insurance solutions, and we are proud to be emerging as that,” Henry said.

![]() “We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

“We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

Henry boasted about how his company is the only one writing policies without traditional demographics in mind. “Today, I’m really proud to say that LOOP is the only insurance product that is a standard auto product that doesn’t have any of those demographic factors, it’s completely technology driven,” Henry said.

According to Henry, LOOP’s status as a public-benefit corporation, or B-Corp, will give his company the moral obligation it needs to fulfill its mission of being a fair, non-biased, and non-discriminatory auto insurance provider. The B-Corp status creates a “double bottom line” as Henry put it, creating a legal obligation for the company to hold the values in its mission statement for its customers, as well as the traditional corporate obligation to what’s best for its shareholders.

“From a business perspective, it’s kind of a risky thing,” Henry stressed when talking about the obligation to their customers as part of the public-benefit agreement. “The public can sue us if they ever feel like we are straying away from our mission.”

Customers are saving an average of 35% on their auto insurance premiums when quoted by LOOP, according to Henry. The company name directly correlates with the envisioned series of events that a LOOP customer will experience while holding a policy. A LOOP customer signs up, gets a good rate, utilizes the information given by LOOP, their driving is tracked and the data is analyzed, and the rate drops upon renewal after the policy expires. By repeating this, the customer “loops” around a cycle of better information leading to better rates.

“This is a mass market product. There is mass consumer demand. Our waitlist has grown to over 30,000 people across all fifty states, with different age groups and backgrounds,” Henry said. “I think people are excited to have an insurance company they can love again.”

Fintech Déjà Vu: Wait, Has This All Happened Before?

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

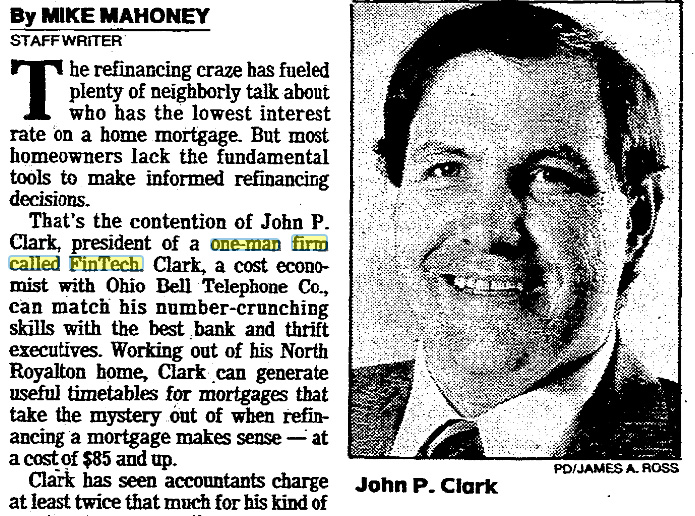

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

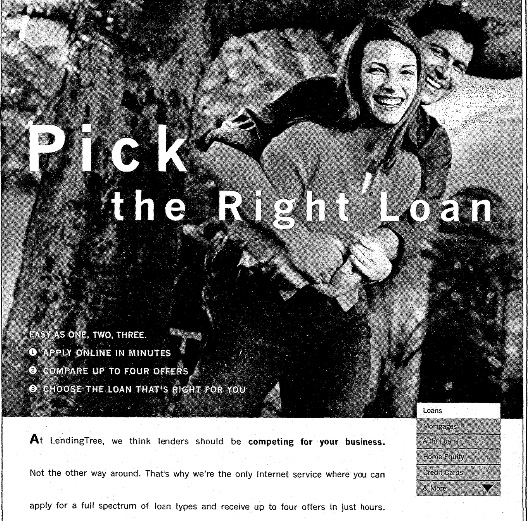

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”

Canada is Looking Forward to Open Banking

October 4, 2021 “It’s a fairly big deal,” said Tal Schwartz, Senior Advisor to the Canadian Lenders Association, when discussing the Canadian government’s renewed interest in alternative lenders after the recent Canadian election. As potential government officials from both parties discussed ideas about open banking in their election campaigns, such a conversation had been quelled by the “Big Five” Canadian banks— until now.

“It’s a fairly big deal,” said Tal Schwartz, Senior Advisor to the Canadian Lenders Association, when discussing the Canadian government’s renewed interest in alternative lenders after the recent Canadian election. As potential government officials from both parties discussed ideas about open banking in their election campaigns, such a conversation had been quelled by the “Big Five” Canadian banks— until now.

“The closer we get to some kind of entrenched regulatory framework, the better positions fintechs will be in to actually compete, get access to financial data, and raise money in an environment where there is regulatory certainty,” said Schwartz.

In August, the Canadian department of Finance welcomed a Final Report from the Advisory Committee on Open Banking that showcased a plan to modernize the Canadian financial regulatory system, with open banking and fintech in mind.

“Consumer-driven finance, or open banking, is already part of Canadians’ lives,” said Chrystia Freeland, Canada’s Deputy Prime Minister and Minister of Finance, in the report.

“Many use digital services every day to manage their money, to budget for expenses, and to make investments. Working towards a regulated, made-in-Canada system will make sure that we continue to enjoy a strong, stable, and innovative financial sector that is globally competitive, promotes consumer choice, prioritizes data privacy, and contributes to economic growth,” Freeland continued.

Schwartz said that the traditional oligopolistic structure of Canadian banking can offer advantages in times of financial crisis, but not when the government is shelling out money to help businesses during pandemic-related shutdowns.

“The reality was, if you’re a small business, you don’t have a credit relationship with a big bank, the only credit relationship you have is with an alternate lender,” said Schwartz. “By distributing money through big banks, in one sense, you’re not servicing customers the way they want to be served, and you’re cutting oxygen to a flourishing part of the innovation economy in Canada.”

“The reality was, if you’re a small business, you don’t have a credit relationship with a big bank, the only credit relationship you have is with an alternate lender,” said Schwartz. “By distributing money through big banks, in one sense, you’re not servicing customers the way they want to be served, and you’re cutting oxygen to a flourishing part of the innovation economy in Canada.”

Unlike in the United States, the Canadian government gave exclusive access of allocation to pandemic-induced federal assistance loans to the Big Five banks, leaving small business lenders relatively out to dry during that time. When asked about what issues he would like to see the new administration tackle first when it comes to alternative lenders, Schwartz mentioned the allocation of this type of money moving forward.

Other institutions outside of big banking in Canada are making strides in their effort to compete. Fintech giant Stripe announced hiring sprees for their new Toronto office last Thursday. Then there’s Nuula, a startup that aims to build a user-centric financial super app, announcing $120M in funding in early September.

To reach its full potential, Canadian fintech companies need the access to more data. The report recognizes the acknowledgement of the necessity this data is to fintech companies. “The scope of Canada’s open banking system in its initial phase should include data that is currently available to consumers and small business through their online banking applications,” it says. “Financial institutions should be allowed to exclude derived data – described as data enhanced by financial institutions to provide additional value to their consumers, such as internal credit risk assessments” the report reads.

“Historically, there hasn’t been very tech friendly or [Big Bank] challenger friendly regulations,” Schwartz said. “This is really the first time we’ve seen the political parties even mention issues of open banking and saying this will be a priority for our next government.”

“This has given the industry a lot of hope,” said Schwartz.

Would You Invest Your IRA Funds into MCAs?

September 22, 2021 A partnership between Supervest and Alto Solutions will bring in an unprecedented opportunity for investors, as the two groups will come together to allow IRA investors a chance to put their money in MCA funding. Account holders with Alto will be able to divide their money on a fractional basis to a diverse set of investments on the Supervest interface.

A partnership between Supervest and Alto Solutions will bring in an unprecedented opportunity for investors, as the two groups will come together to allow IRA investors a chance to put their money in MCA funding. Account holders with Alto will be able to divide their money on a fractional basis to a diverse set of investments on the Supervest interface.

“We expect these alternative investments to be very popular given the meaningful diversification they can provide to individual retirement portfolios in addition to being yield-generating and short-duration products,” Alto’s Chief Revenue Officer Tara Fung told AltFinanceDaily on Tuesday. “We will continue adding to our platform so that clients have more options to invest in alternative assets that further diversify and grow their retirement portfolios.”

Alto has made a business model out of using IRA funds for unique alternative investments. Crypto investments are another option listed on their website.

Supervest is no stranger to incorporating new business ideas, either. Their business model is based on connecting investors to inaccessible classes of assets, like MCAs for example.

John Donahue, the Chief Investment Officer with Supervest, spoke with AltFinanceDaily on Wednesday about the opportunity it gives IRA account holders. “It’s the opportunity for any accredited investor to now be able to access the Supervest platform of fractionalized participation in MCA deals through their self-directed IRA,” Donahue said.

MCAs can be inherently riskier than a typical lukewarm investment portfolio, but the IRA concept is basically detached from the selected risk profile therein.

“The IRA is strictly a structure,” said Donahue, when asked about the inherent risks of MCA investments with IRA money. “It really doesn’t have a connotation of conservative or aggressive nature. You can have aggressive mutual funds [in an IRA], you can have your entire investment of your IRA in the ARK New Technology fund, and while that has gone up considerably in the past few years, there’s a massive amount of volatility, it’s extremely risky, and arguably much riskier than an MCA investment.”

Donahue reiterated that only “accredited investors” would have access to these types of investments through the Supervest platform.

As the partnership between the two companies kicks off, it’ll be interesting to see if individuals are willing to put their retirement money on the line to invest in small businesses.

Homegrown Software Enables FundKite to Reconcile MCAs Daily Rather Than Monthly

September 21, 2021 “Data is the future,” said Alex Shvarts, CEO of FundKite. Through his own proprietary software that he personally built, Shvarts and his team can see daily deposits from merchants that FundKite has funded while also viewing the real-time financial condition of their customers. There are no assumptions, no end-of-month scrambling to do MCA reconciliations, and there are significantly less defaults, he says.

“Data is the future,” said Alex Shvarts, CEO of FundKite. Through his own proprietary software that he personally built, Shvarts and his team can see daily deposits from merchants that FundKite has funded while also viewing the real-time financial condition of their customers. There are no assumptions, no end-of-month scrambling to do MCA reconciliations, and there are significantly less defaults, he says.

Shvarts believes that he has a better chance of retaining clients and keeping deals in place when customers face difficulties. “When merchants are in trouble, they are being coached not to pay,” he said, hinting at third parties in the industry that lobby customers to stop payment in exchange for some kind of alleged assistance.

“Our merchants don’t go under,” Shvarts said.

The premise is that FundKite’s tech enables both themselves and the customer to keep track of how much money is going in and out in real time. That allows them to apply the precise holdback on a daily basis instead of waiting for a bank statement at the end of the month to see what the difference was.

“Our goal is to use our software to be extremely merchant friendly,” said Shvarts.

By compiling different data sets about the merchant, potential clients can be pre-approved and fully funded in less than an hour through a completely digital application process. While this process of instant pre-approval isn’t new to the industry, it’s the idea of having access to client’s banking information that is key to the software’s accuracy and success in funding packages and payment options.

By compiling different data sets about the merchant, potential clients can be pre-approved and fully funded in less than an hour through a completely digital application process. While this process of instant pre-approval isn’t new to the industry, it’s the idea of having access to client’s banking information that is key to the software’s accuracy and success in funding packages and payment options.

The idea of end-of-month reconciliation doesn’t work for many merchants, according to Shvarts, who was speaking in reference to merchant cash advance transactions. “A month later, they could already be in the hole,” he said. “This product [where debits vary daily based upon true sales] works better for merchants, it works better for portfolios, if you’re actually reconciling and pulling what you’re supposed to, and not what you’re anticipating.”

The system is maintained in-house at the firm’s downtown Manhattan offices, with a fully temperature-controlled server room that is home to dozens of computers that host the company’s software. Backed up in the cloud as a failsafe, the system is as much of a presence in the office, both physically and virtually, as the individuals that work there.

“I’ve always had coding implanted in my mind, it’s an everyday process to make things simpler and faster,” he said. Shvarts explained that his love for coding and finance stems from a childhood passion for chess. “Chess taught me the ability to analyze moves.”

Aquila Services Inc. Has Ceased Operations

September 9, 2021Aquila Services Inc, a data-driven small business cash flow management platform, ceased operations sometime early last year, AltFinanceDaily has learned. The company had been trying to pivot even before the pandemic began. CEO and Founder Taariq Lewis, who had spoken about AI and machine learning at some length to us in 2018, updated the company’s website with the bad news.

Aquila is now closed for business and we have shut down our servers after a three year run. Thanks to all our 9,688 customers and our many investors for allowing us to provide cash flow analysis for small businesses.

If you are seeking business funding, please be sure to check our partners at Rapid Finance, Credibly, Kabbage, and others for access to capital and please check with Home Depot for discounts on construction equipment.

Lewis is now listed as a co-founder of UniFi DAO, according to LinkedIn.

Knight Capital Technology to Play Continuing SBA Loan Role at Ready Capital Corporation

September 7, 2021 Ever since Ready Capital’s name arrived on the big stage for its leading role in the nation’s PPP lending, the company has continued to be very active in small business lending. They completed round 2 of the PPP program with $2.2B in loans to more than 72,000 small businesses. For comparison’s sake, that’s twice what PayPal contributed, who provided $1B to 43,000 businesses.

Ever since Ready Capital’s name arrived on the big stage for its leading role in the nation’s PPP lending, the company has continued to be very active in small business lending. They completed round 2 of the PPP program with $2.2B in loans to more than 72,000 small businesses. For comparison’s sake, that’s twice what PayPal contributed, who provided $1B to 43,000 businesses.

Ready Capital is the #1 non-bank in the nation in 7(a) SBA loan originations this year so far, according to John Moser, President of the company’s SBA lending division, and is #7 in the entire SBA lending industry nationwide.

Some of the technology behind their success can be attributed to Knight Capital, the company Ready acquired back in 2019. Knight has enabled the company to roll out offerings of SBA loans under $350,000, which it is using to grow its already impressive marketshare.

Speaking about Knight, Ready Capital CEO Thomas Capasse said in the Q2 earnings call, the “[Knight] investment will be levered into more technology affinity-based expansion of the SBA business.”

Overall, the company is optimistic. “Ready Capital is off to a strong start in 2021,” Capasse said during the call. “We have accomplished much in the first quarter of the year with our small balance commercial or SBC, CRE lending operations and Small Business Administration or SBA 7(a) lending businesses, posting record originations, including high volume in round two of the Paycheck Protection Program or PPP.”

Knight’s merchant cash advance business is combined with its small business lending division for quarterly reporting purposes so its individual stats are not easily ascertainable. The company still touts “same day business funding” on its website.

What The “Capital Dude” Said About Experience, Success, and the Future

August 18, 2021 Coming in at rank #1,044 on the 2021 Inc 5000 list was a small business finance provider with a whimsical name, Capital Dude. Having some common ownership overlap with another Inc ranked company, Central Diligence Group (#2,893), the Dude told AltFinanceDaily that they didn’t shut down or pause funding throughout 2020. In fact, they continued to grow.

Coming in at rank #1,044 on the 2021 Inc 5000 list was a small business finance provider with a whimsical name, Capital Dude. Having some common ownership overlap with another Inc ranked company, Central Diligence Group (#2,893), the Dude told AltFinanceDaily that they didn’t shut down or pause funding throughout 2020. In fact, they continued to grow.

“We really have to attribute the company’s growth to our hardworking and efficient team that made sure we didn’t miss a beat while having to work remote,” said company partner Andrew Hernandez.

The name, Capital Dude, was chosen to convey an easy process to their partners and clients, the company says, while at the same time being compatible with a mascot they had in mind. The Capital Dude himself is a superhero in a green suit with the letters “CD” emblazoned on his chest. He’s also got a red cape and a flashy smile.

Behind the optics, however, is a seasoned team.

“We got started in the industry during the ’08 – ’09 recession,” Hernandez said, “so when you experience getting started during a downturn, you quickly realize that the only way to keep going is to stick to your principles while continuously taking inventory of the ongoing situation and making any necessary changes quickly in order to protect the portfolio. While both downturns were very different in how they played out, applying that previous experience to the past 18 months has been interesting as we have seen a lot of similarities that are very measurable.”

Central Diligence Group, meanwhile, has gotten repeat recognition on the Inc 5000 list.

“CDG offers consulting and underwriting services to other alternative financing companies in the industry,” Hernandez explained. The “short term plan is to scale out this portion of the business in 2022 via licensing of our platform to funders, funds, accredited investors, etc.”

The companies are currently in the process of moving to a new office and they expressed that they are “very bullish on the future” and plan to increase their headcount and continue to grow.