North Mill Announces $353MM Term Securitization

October 17, 2022OCTOBER 14, 2022, NORWALK, CT – North Mill Equipment Finance LLC (“NMEF”) announced today the closing of its sixth commercial equipment backed securitization (ABS), NMEF Funding 2022-B (“NMEF 2022-B”). The $353MM transaction is North Mill’s 2nd ABS transaction this year, bringing the total privately placed bond proceeds raised this year to $724MM for the year. NMEF’s Capital Markets team has now raised $1.4B in bonds since inception. NMEF 2022-B featured fixed-rate asset backed securities across three classes of notes with the A note split into two tranches; an A-1 money market class, and a AAA/Aaa rated tranche by KBRA/Moody’s. This was NMEF’s first ABS issuance to be rated by Moody’s. It was also NMEF’s first transaction to include all investment grade tranches.

“The transaction was well-received by institutional investors with 31 unique investors, including 12 new investors in the NMEF shelf, making it NMEF’s largest ABS investor base of all time. We attribute this to the addition of a big-three rating agency with a 4% base case cumulative net loss assumption as well as a reduction of the base case loss assumption from KBRA from 6.1% – 6.6% on our last transaction down to 4.79% on NMEF 2022-B,” said North Mill’s President and Chief Operating Officer, Mark Bonanno.

Pier Snider, NMEF’s Chief Financial Officer added, “The transaction includes a $101MM 3-month post-close prefunding period that gives NMEF a fixed cost of funds for 4th quarter originations in a rising rate environment.”

About North Mill Equipment Finance

North Mill Equipment Finance originates and services small to mid-ticket equipment leases and loans, ranging from $15,000 to $1,000,000 in value. A broker-centric private lender, the company accepts A – C credit qualities and finances transactions for many asset categories including construction, transportation, vocational, medical, manufacturing, printing, franchise, renovation, janitorial and material handling equipment. North Mill is majority owned by an affiliate of InterVest Capital Partners, Inc. (FKA Wafra Capital Partners Inc.). The company’s headquarters is in Norwalk, CT, with regional offices in Irvine, CA, Dover, NH, Voorhees NJ, and Murray, UT. For more information, visit www.nmef.com.

They Grew Tremendously Through the Pandemic and Landed on the List

September 26, 2022 Inc recently dropped the latest annual list of the fastest growing small businesses in the country. These 5,000 businesses span across a range of industries including health, financial, IT services and more. Companies such as Fundomate, Fountainhead, and Business Lending Blueprint have been featured on this year’s list due to incredible growth.

Inc recently dropped the latest annual list of the fastest growing small businesses in the country. These 5,000 businesses span across a range of industries including health, financial, IT services and more. Companies such as Fundomate, Fountainhead, and Business Lending Blueprint have been featured on this year’s list due to incredible growth.

For Sam Schapiro, the grit to grow Fundomate through a pandemic stemmed from a realization he came to years earlier.

“I think one of the best lessons I learned when I launched Fundomate, I was in Las Vegas at a conference to raise money,” Schapiro said. “…and barely anybody looked at us and I literally left with nothing.”

Full of doubt, Schapiro had lunch with someone he respected that had built several successful startups. That mentor told him that despite what he thought, 99.9% of the people pitching their business at the show were going to fail regardless, even if they really wanted success.

“So if you don’t really really really want it, then don’t bother doing it, because your chances of success are so slim,” Schapiro was told. That hard dose of advice led Schapiro to first question how bad he wanted it and he realized he was fully committed to seeing it through.

“I always say that if I knew how long it would take us to get here and how hard it would be to be down this road, I’d never get on the road,” Schapiro said. “But that’s the thing about life in general. Anything worth having and anything worth doing requires consistency and determination. And over and over and over again. So if something’s not working, and you can obviously see it’s not working and it’s clear, you know, the job is to keep looking at it, and at the point where it becomes a clear message that it just doesn’t work, then you got to pivot.”

Fundomate is a white label funding and banking platform for wholesale processors and MCA funders to automate their funding in a scaled way. Schapiro says that success was due in part to their technology, which collects a true daily percentage of a business’s sales.

As the pandemic subsided “we didn’t have to get back on the phone with every merchant and say, ‘Hey, we want to increase our daily payment again’ because we’re not on daily payments, we’re on instant collections that are happening on a daily basis,” Schapiro explained. “As soon as their sales came back up and even grew to get through the 2021 boom, all the sudden collections happen faster.”

Meanwhile, for Chris Hurn, Founder and CEO of Fountainhead, he had to refocus his non-bank small business lending company into a PPP loan operation.

“Pivoting our business solely to do PPP loans over the last two years was a pretty challenging experience,” said Hurn. “And we did, we worked ridiculous hours. I mean I averaged about three to four hours of sleep a night for months at a time every day. So, you know, that was probably the biggest challenge we had.”

But the work paid off. Hurn said that they were one of the most active PPP lenders over the last two years, making approximately 300,000 loans.

“Obviously, that helped accelerate our growth,” said Hurn, “as well as many of our full time hires that we made during that time are still there. And we’re still growing now.”

The process is no walk in the park when it comes to being listed on the Inc 5000. Thousands of companies apply annually to be ranked on the list. It’s months of lengthy paperwork and long-waited verifications. After realizing that one’s company has made the list, they find out their ranking along with the rest of the world.

“It’s a painstaking process because you can’t just apply and claim that you’re a growing company,” said Oz Konar, Founder at Business Lending Blueprint. “Your CPA needs to send them income verification or revenue verification, and all the things need to be documented and signed off on so they can actually prove that you’re a growing company, and you can make it on the Inc 5000.”

The hardest part of newfound success is maintaining it. With massive growth over the past four years, Konar believes growth happens when you have happy customers. Focusing on democratizing the lending space for new and existing brokers has drawn clients into his business.

“When you do things the right way consistently and stay laser focused on one problem, one solution, one product, that’s what brought us to the Inc 5000,” said Konar. “And to our surprise, we were hoping that we were going to be ranking about 1,000, the first 1,000 companies. We ranked in 799. So, it’s such an honor, we’re so happy, and we’re just getting started.”

In the competitive industry of finance that is always changing and rearranging, SMB finance companies may feel pressured to do all things for all people. But sometimes it may be more beneficial to stick to what one is good at. As Hurn can agree, it is much more complicated to compete in every marketplace.

“I think if you as a business, if you’re starting out, you need to definitely focus on a niche you want to attack and try to be the best at that,” said Hurn.

The Merchant Marketplace Announces Its New Launch with Industry Powerhouse Executive

September 19, 2022 BALDWIN, NEW YORK SEPTEMBER 19, 2022 – The Merchant Marketplace, a leading fintech platform provider of direct financing to small and midsize businesses, announced today the launch of its new leadership with backing from industry powerhouse executives. The company’s new leadership team brings over 75 years of collective financial, technology, and business experience within its core leadership group: Adam Schwartz as CEO and Kevin Harrington, the Original Shark Tank Investor, will serve as a Strategic Partner. This partnership will revolutionize how merchants and independent sales organizations (ISO’s) obtain capital for growing their merchant’s businesses, changing the game for entrepreneurs throughout the United States.

BALDWIN, NEW YORK SEPTEMBER 19, 2022 – The Merchant Marketplace, a leading fintech platform provider of direct financing to small and midsize businesses, announced today the launch of its new leadership with backing from industry powerhouse executives. The company’s new leadership team brings over 75 years of collective financial, technology, and business experience within its core leadership group: Adam Schwartz as CEO and Kevin Harrington, the Original Shark Tank Investor, will serve as a Strategic Partner. This partnership will revolutionize how merchants and independent sales organizations (ISO’s) obtain capital for growing their merchant’s businesses, changing the game for entrepreneurs throughout the United States.

“We are looking to change the industry by using a true fintech platform to facilitate transactions amongst ISO’s, merchants, and the Merchant Marketplace,” said Merchant Marketplace CEO Adam Schwartz. “We understand the challenges many small business owners face when trying to secure financing to help make their dreams a reality. The Merchant Marketplace is happy to be a resource for entrepreneurs by providing them access to capital so they can build a successful business.”

The Merchant Marketplace created a proprietary syndication platform that offers real time data and full transparency. In most instances, the company will offer ISO’s a two percent syndication as bonus for every deal that it funds, with the ability to syndicate more funding if needed. ISO’s can earn another stream of income by being vested in every deal they fund with the Merchant Marketplace, as well as earn a referral fee. The platform also offers a profit-sharing program and technology tutorials to show ISO’s how to engage with the platform to help achieve the best end results.

“The merchant cash advance market has been witnessing an escalation in growth over the past few years with the help of innovation. Our technology integrates with over 25 different third parties to give us complete insights into our merchants, giving us the ability to make offers with lightning speed and efficiency. We understand the needs of our clients and we want them to be part of the process. We do not want to be seen as just another funder; we want to be seen as a business partner for our ISO’s,” said Merchant Marketplace Director of ISO Relations, Justin Strull.

For questions on the service and to sign up as an ISO, contact Justin Strull at 516-980-4932 or email in to justin@merchantmarketplace.com

About Kevin Harrington

As an original “shark” on the hit TV show Shark Tank, the creator of the infomercial, pioneer of the As Seen on TV brand, and co-founding board member of the Entrepreneur’s Organization, Kevin Harrington has pushed past all the questions and excuses to repeatedly enjoy 100X success. His legendary work behind the scenes of business ventures has produced more than $5 billion in global sales, the launch of more than 500 products, and the making of dozens of millionaires. He’s launched massively successful products like The Food Saver, Ginsu Knives, The Great Wok of China, The Flying Lure, and many more. He has worked with amazing celebrities turned entrepreneurs including, Billie Mays, Tony Little, Jack LaLanne, and George Foreman to name a few. Kevin’s been called the Entrepreneur’s Entrepreneur and the Entrepreneur Answer Man, because he knows the challenges unique to start-ups and he has a special passion for helping entrepreneurs succeed.

Let’s Get Personal! (In Sales)

September 16, 2022 “Personalization is adding that human element to a buying process that can traditionally feel either very stressful or cold and clinical,” said Taylor Hicks, Creative Strategist at Elevate Funding. “It’s about recognizing that clients (and prospects) are humans with their own unique set of needs and goals.”

“Personalization is adding that human element to a buying process that can traditionally feel either very stressful or cold and clinical,” said Taylor Hicks, Creative Strategist at Elevate Funding. “It’s about recognizing that clients (and prospects) are humans with their own unique set of needs and goals.”

Working in this industry and communicating with clients is a given but being personable with each one encountered is a task within itself. No client wants to be victim to a boring sales call where the one pitching lacks a persuasive personality. And nobody wants to be on the other end of the call feeling like they are wasting their clients’ time with a dull sales pitch. Making the client-to-business communication an eventful experience for both parties comes with a great amount of pressure, and it also can make or break a deal.

“Be a human being. Don’t do the high-pressure sales things like some of these guys are doing,” said Alexander Gold, CFO at Future Funding. “I get compliments that my guys are not doing that, and I feel like it’s just timing. So, if your timing is good, people will give you the shot. If your timing is bad, you won’t get the shot…”

The client needs to know that they can fully put their trust into a company or product, and it will be worthwhile. Creating a mutual trust, especially when dealing with a person’s finances can be a very personal experience. The key to that can be very simple, as Gold says, to tell them who you are and how you can help with just a moment of their time.

“So first, you have to build credibility, I would say that’s the most important thing is building credibility,” said Gold. “That could be knowing something they don’t, showing them something or teaching them something that you can prove and then possibly show them as well. I would say products, being very knowledgeable in your products and your product base.”

“So first, you have to build credibility, I would say that’s the most important thing is building credibility,” said Gold. “That could be knowing something they don’t, showing them something or teaching them something that you can prove and then possibly show them as well. I would say products, being very knowledgeable in your products and your product base.”

“…[It’s] how do you provide them interesting insights into their finances or into their needs without coming across overbearing or selling them something that they don’t need?” said Greg Varnell, VP of Product and Development at Q2. “And that’s a real balance. And so, I think, for us, personalization isn’t just trying to sell somebody something, but it’s trying to tell them the information that they need when they need that information.”

“I think trust has to be earned,” said David Roitblat, Founder and CEO at Better Accounting Solutions. “Most of our clients are referral based from other clients. So I guess that speaks for itself. […] So that does give us a head start on that, but ultimately, people judge you based on your work.

“At Elevate, we take a custom-tailored approach for each client,” said Hicks of Elevate. “We send out newsletters to our clients biweekly to remind them of our various programs, like add-ons and renewals. We are proactive in reminding them of their Future Receivables Sales Agreement, and we’ll always work with them on reducing their payment amount if their revenue drops. We provide our clients a variety of ways to get ahold of us – whether that’s email, call, text.”

Regardless of your role in the finance industry, interactions can have long lasting impacts. From the initial meeting to developing trust, and eventually turning that journey into a meaningful working relationship. And who knows, that one great client interaction could lead to many referrals and recommendations in the future.

Think The New California Disclosure Law is Just About a Disclosure Form? Think Again

September 13, 2022 “We’re one of the good guys so of course we’ll comply and include the form with our contracts.”

“We’re one of the good guys so of course we’ll comply and include the form with our contracts.”

Variations of the above phrase have been oft-repeated in the last few months by participants in the commercial finance industry when queried by AltFinanceDaily about California’s new disclosure law. Several companies have shared that they are prepared for what’s to come, but are they? The regulations go into effect on December 9th and begin a new chapter of compliance for the industry.

Though one might be aware that California will require specific disclosures on commercial finance contracts (including purchases of future sales), Katherine C. Fisher, Partner at Hudson Cook, LLP, explained that the breadth of the state’s law will likely require changes to a funding company’s operational processes as well. Fisher told AltFinanceDaily that there’s not just the matter of disclosing but also the matter of what triggers a disclosure having to be made. What might otherwise be considered the normal discourse between a funding provider and a customer prior to a deal being consummated is now an area requiring close examination.

“If a broker sends a text to a merchant with the offers, could it trigger this?” is one scenario she posed about the threshold for disclosure.

The funding provider needs to know the answer because once the disclosure requirement is triggered, the broker needs to relay back the details of the offers made, the specific disclosures provided, and the timestamp of when this took place. All of this data then needs be stored by the funding provider to maintain compliance.

And funding providers will need to be vigilant.

“The funder is responsible for broker compliance,” Fisher said.

The entire process of who-said-what, when, and how will suddenly become a realm requiring tight control it seems. And that all comes back to the form itself, which is not all that simple either.

California will require funding providers to estimate an APR on a purchase transaction using one of two methods: the Historical Method or the Underwriting Method. While the methodology selected is probably best left to qualified counsel to assist with, the likely deviation of a future estimated APR from a backwards-looking APR was a reality considered by state regulators. To bridge this gap, California requires that funding providers disclose reasonably anticipated true-up scenarios. A true-up in this instance refers to the already well-established option for a merchant to perform a monthly reconciliation of payments if the amount collected is above or below the purchased percentage specified in the contract.

California will require funding providers to estimate an APR on a purchase transaction using one of two methods: the Historical Method or the Underwriting Method. While the methodology selected is probably best left to qualified counsel to assist with, the likely deviation of a future estimated APR from a backwards-looking APR was a reality considered by state regulators. To bridge this gap, California requires that funding providers disclose reasonably anticipated true-up scenarios. A true-up in this instance refers to the already well-established option for a merchant to perform a monthly reconciliation of payments if the amount collected is above or below the purchased percentage specified in the contract.

Though the very nature of the reconciliation is a consequence of not being able to predict the future exactly, California’s law requires that funding providers disclose the dates and amounts of the true-ups that they reasonably anticipate. Such concepts and mathematics, once perhaps the subjective domain of a funding provider’s in-house underwriters will soon be subject to regulatory scrutiny for total accuracy. And this just scratches the surface.

The scope of this law is so unique and technical that the Hudson Cook law firm spent a considerable amount of time preparing a guide on this very subject. AltFinanceDaily saw some of the pages of this guide during a call.

Fisher, meanwhile, insisted that compliance in California is different than compliance with the law recently enacted in Virginia and that if funding providers wait until December to begin preparing, it will probably be too late to be ready in time.

“This is more than just a form,” Fisher said. “You need to spread the word about it.”

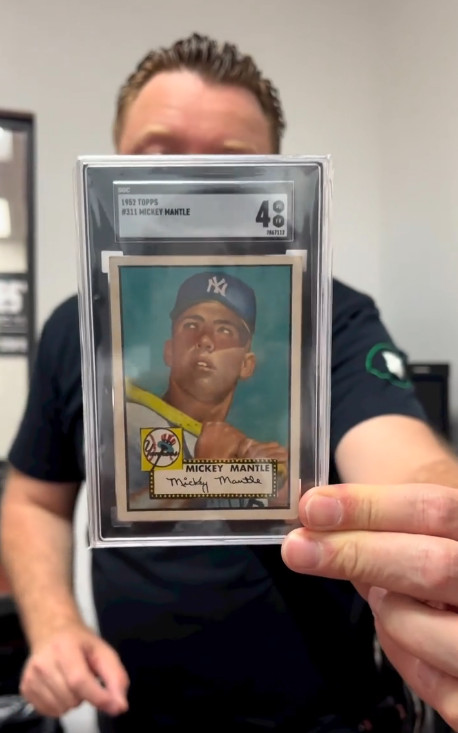

Got a Mantle, Bryant, or Mahomes Card? This Company Wants to Fund You

September 12, 2022 Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

The value of the Mantle sale came as no surprise to one budding entrepreneur in South Florida. On Instagram, he’d been talking about Mantle cards for weeks, even going so far as to hold up another ’52 Topps Mantle card to the camera to promote what his company can do, which is provide quick cash advances to owners of valuable sports cards.

The entrepreneur’s name is Edward Siegel, CEO of Card Fi. Siegel’s no stranger to the alternative finance space because he spent about a decade in the MCA industry, most recently as the founder of Bitty Advance, which he sold in 2020. Since then, Siegel returned to his roots and early passion of his youth.

“I had a background in sports cards as a collector, you know as a kid, but then in my early twenties, I was promoting card shows at malls,” Siegel said. “I was heavily into the hobby, setting up the card shows and promoting them and doing player appearances where players come in and do an autograph appearance.”

That was back in the late 80s, early 90s, according to Siegel.

When Covid hit and he exited his most recent company, he noticed a massive resurgence in the sports trading card market. His next business ultimately became Card Fi, a company that will evaluate the market value of a card and make an advance against it. There’s obviously risk involved so they take possession of the card for the duration.

“We have to get a hold of these cards and we’re responsible for them and then we vault them in our in-house bank vault,” Siegel said. The cards are stored in a highly secure climate controlled environment. Card Fi shows the vault off frequently in its Instagram videos.

Such a business requires large amounts of capital so Siegel went searching for investors, a pursuit that led him to a unique place, an Instagram Live pitch competition hosted by famed CEO and reality TV star Marcus Lemonis. Siegel entered himself in as a contestant, knowing full well that the odds of even being chosen to present his business to Lemonis were about a million-to-one.

Somehow, he was called up to pitch.

“So [businesses] went on there during the quarantine and you pitched your business,” Siegel explained. “I went on there and I pitched it […] And he understood it and he thought it made sense.”

The moment eventually led to a deal with Lemonis’ company and Card Fi was on its way.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

“If we look at it, there’s two different markets, you have the modern card market [where] I would say it’s basketball [that leads the pack],” he said. “For the vintage card market it’s baseball.”

Football is huge as well, he explained. A Patrick Mahomes rookie card, for example, an NFL Quarterback that’s still currently playing, recently fetched $861,000. There are only one of five like it in the world, the scarcity playing a major role in the value. Meanwhile, a Justin Herbert rookie card, an NFL Quarterback who’s only in his third year was already receiving bids above $1 million at the time this story was being written.

“It really depends on the card itself,” Siegel explained. “Some players might be known for having better careers but then you have cards that have more scarcity to them. Something that’s a one of one or maybe a very low populated card and a graded PSA 10 could very well be worth more than a [Michael] Jordan rookie because it has scarcity in it.”

PSA refers to cards that have been verified as authentic and graded on the condition of the card itself. Ten is the highest level a card can receive. Card Fi will only work with graded cards to avoid any funny business when it comes to advancing funds based upon the value.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

“This financing benefits the market as loans and cash advances have become an increasingly asked-for offering among trading card collectors,” said Chad Fister, PWCC’s CFO in a story that originally appeared on Sportico. “Enabling our clients to access liquidity through a menu of capital offerings is key as trading cards continue to prove themselves to be a valuable tangible asset class.”

For Card Fi, customers that take an advance can track everything through an online portal, including details about their cards, payments, and balance.

“We want to note that we built a full-service automated underwriting and collection platform to where, whether it’s the customer or the broker, they can log into our system and put the description of the card into the system and it’s going to automatically underwrite it and price it out,” Siegel said.

That description sounded like something straight out of the fintech industry of his past, especially the component about brokers.

“Just like the MCA space, we have a whole partnership side, a broker side, where brokers can refer us customers just as an affiliate where they just send the info over,” Siegel said. Similarly, they can earn a commission if a transaction is completed, he explained.

In this industry, brands like Topps, Upper Deck, and Panini have become the bread and butter for Card Fi. Even though it’s all business for Siegel these days, he couldn’t help but mention a particular card he had a personal attachment to.

“My personal favorite card in my collection is the 1965 Topps Joe Namath rookie card,” Siegel said. “Of course being a die hard New York Jets fan, that has to be my favorite card.”

Why is a Recession Good for the MCA Industry?

August 30, 2022

The MCA industry has strived for many years to overcome tremendous challenges. Interestingly, many in the industry – especially the many new “rookie funders” – are very nervous about the looming recession. In this article, we will attempt to calm nerves and delve in detail about how high inflation rates have affected the MCA space. More importantly, we will address how the inevitable recession will actually be good for the industry – if we play it right.

The MCA industry has strived for many years to overcome tremendous challenges. Interestingly, many in the industry – especially the many new “rookie funders” – are very nervous about the looming recession. In this article, we will attempt to calm nerves and delve in detail about how high inflation rates have affected the MCA space. More importantly, we will address how the inevitable recession will actually be good for the industry – if we play it right.

A Changing Environment

Funders and ISOs alike must be superefficient in working within the MCA guidelines, so they can avoid collapsing in the coming recession. The MCA game has drastically changed in recent years. The product, the rules, the accepted norms, and even the actual laws have changed. It is only natural that many of the “new funders” won’t have a complete grasp of the very original merchant cash advance product, and what made it work. Unless a funder has a complete understanding of why and how something works, they won’t know why and how it cannot work. Before we directly address the status of the current inflation, and discuss how to prepare for the recession, lets briefly go back and talk about the original merchant cash advance product.

The Monkey’s Ladder

It reminds us of an old parable where a scientist placed a ladder with a bunch of bananas on top of it, in the center of a cage full of monkeys. Whenever one of them attempted to climb the ladder, the scientist sprayed all of the monkeys with icy water. Eventually, whenever a monkey took a first step onto the ladder, the others would pull him off and give him a beating, because they wanted to avoid the icy water. The scientist then substituted one of the monkeys with a new one, who naturally jumped on the ladder as soon as he entered the cage and noticed the bananas. He immediately received a proper beating and learned to never go up the ladder – but he never learned why. Eventually all the monkeys were replaced, and the new monkeys learned not to climb the ladder, but no one knew why. Here, we will attempt to inform our new monkeys, I mean funders, about why we do things the way we do. When the recession finally hits, at least they will know to prepare a raincoat before the icy water hits them in the face.

Bob’s Pizza

The original merchant cash advance recipient was a hard-working pizza shop owner named Bob. Unfortunately for him, his oven broke, and the replacement cost was ten thousand dollars. Bob didn’t have good enough credit for traditional financing options. Of course, without a pizza oven Bob’s business faced an imminent demise. As a last-ditch effort, he contacted a factoring company, who funded businesses with their existing receivables, and asked if they would consider funding “future” receivables. The funder reviewed Bob’s file and immediately identified Bob’s bad credit, which was why no bank wanted to take a risk on Bob’s Pizza. The funder calculated that if the big banks had been able to legally charge a much higher APR, they may have taken the risk on Bob after all. The reality – it was the funding price that limited Bob’s credit options, not his bad credit.

This funder happened to be a “softy” and since the factoring industry was not limited to what the usury laws allow, he decided to come up with a solution that worked for both parties. To make the long story short, the funder offered to take a risk and fund the crucial pizza oven, by purchasing the future sales of Bob’s pizzas. The funder would do this if Bob was willing to pay a 1.49 factor rate, and let the funder draw a small percentage of Bob’s daily sales as payment. The funder determined that the pizza shop generated enough sales to cover the cost of the oven by paying just a small percentage of the running daily sales.

The funder believed the risk was minimal, and the rate balanced out the risk that Bob’s Pizza would default before the oven was paid off. Bob figured out that the cost for the oven was not ten but fifteen thousand dollars because of the funding arrangement. Bob believed it a relatively small charge to pay the additional five thousand dollars, in order to get the ten thousand dollars needed to buy his oven. After all, without the oven, his business would fail.

MCA in the Post-Covid19 Era

A lot has changed since Bob received the first MCA. For the purposes of this inflation-recession conversation, let’s skip to the current post-Covid19 era of the MCA space. First, the basic economic concept involved is that the need for a high-cost funding product such as an MCA peaks when interest rates are generally high and there’s a tight credit market on main street. Those in the high-risk bracket will find it even more difficult to obtain financing, and will seek out an MCA. Reversely, the demand for the MCA product is lowest when interest rates are low, and it is easier for a business to access credit. Even if Bob himself doesn’t have direct access to credit, if the oven supplier has easier access to financing, they will offer an in-house finance option directly to Bob. He won’t need to sell his future pizza pies at 1.49 factor rates for an MCA funder to replace his pizza oven.

How do these basic foundational MCA concepts line up with actual historical events in the space? The economic boom leading up to Covid19 saw record low interest rates and unemployment, which caused a drastic drop in the demand for high-cost funding. In reaction, the MCA space normalized stacking. As a direct result of the imbalance in supply and demand, funders added the option to fund multiple positions. Post-Covid19, the government issued many rounds of PPP and EIDL loans, and the demand for MCA money plummeted to the lowest point in the history of the industry. This also explains the high inflation rates we currently experience. With easier access to money, more people spend more money, which drives up the prices to access money, through the old economic law of supply and demand. However, by this theory, we should have seen a sharp decline in the number of MCA funders. Unexpectedly, the outcome has been the opposite. Since Covid19, funders have opened at a rate faster than ever seen before in the MCA space.

In fact, the opening of brand-new funders has proportionally outpaced the opening of brand-new merchants.

Investing Changes Post-Covid19

The reason for this outcome is simple. When more people have access to money, more people invest money. A lot of people choose cryptocurrency as their easy ride to riches, others have an appetite for the MCA space. Each time a funder opens shop, they add to the overall supply within the MCA space, which aggravates the already stressed demand imbalance. The new funders who came into the space carrying large bags of money from investors weren’t willing to simply return the unopened bags – they wanted to fund. To overcome the lack of demand, these new funders relaxed the underwriting standards. It is now normal to see new funders advertise “we fund defaults.” As a result, many lead generators have stopped creating leads for new merchants. Instead the focus is officially on UCC filings, defaults, etc. These people are basically saying they have given up on expanding the MCA market share, and rely on rerouting the same leads over and over like the game of musical chairs.

A New Era For Bob

Not so long ago all reputable funders funded only 1st positions. Now many of the new funders officially do not fund 1st positions, they only fund a merchant who is a proven payer to a big funder. By this logic, Bob would not have received funding for his pizza oven from most of the new funders. But the truth is that Bob was helped many years ago, and wouldn’t need funding in the current environment, after he wisely saved his PPP and other loans. But, given that he once received an MCA, a lead generator dug him up and Bob was a fresh lead once again.

After receiving many unsolicited offers, Bob realized that the supply and demand imbalance had flipped the game upside down. This was a new era where the demand for merchants was higher than for funding. With such feelings of empowerment, Bob couldn’t resist the offers and decided to take a deal. However, he was determined not to touch the funds. Bob decided to use the funds only to make the payments and build solid MCA credit for a rainy day. The UCC filing chasers picked up on Bob’s situation, and guess what, within a few short weeks, Bob was receiving 2nd position offers.

At first Bob relentlessly refused the offers. He didn’t feel comfortable committing too much of his daily sales that he needed for rent, payroll, and pizza ingredients. Bob soon realized that in the current MCA era, as long as he maneuvered to move his money around so that his bank statements met the new robotic guidelines of the funders, they would keep funding and renewing him. In fact, given the current state of affairs, Bob now realizes that zero of his actual pizza sales need to be committed, since the many funder’s positions and renewals provide plenty of resources to cover the daily payments, just like an efficient Ponzi scheme.

The Effect on Competition

The tricks to artificially force more demand within the same group of merchants was not exercised by the smart and disciplined funders. Many of the big funders officially slowed down on funding. They haven’t provided a detailed explanation about why they are issuing a lot more declines than usual. Some of the big funders choose to battle with the new funders by competing with them. Those big funders, being fully aware that the new funders shy away from 1st positions, also know that when a new funder receives a bank statement with a daily payment to a big reputable funder, it is almost an automatic certainty that the new funder will want to fund a 2nd position, and 3rd, even a 4th position, etc.

Therefore, the big funder has every reason to go ahead and fund it, considering that the merchant will certainly pay the 1st position to qualify for the many more positions to come. However, the big funder is limited to their publicly advertised policies. They now face a problem trying to even get these types of fundings. If one of their “partners” happens to submit such bad paper, they can’t lower themselves to fund it, because they don’t want to admit to their ISOs how desperate they really are.

To overcome these limitations, those big funders who choose to compete with the new funders open their own little “new funder shops.” These anonymous “new funders” do not have any obligations to the big and reputable ISO shops. These new funders accept all ISOs and all paper. This provides an underground tunnel where the big funder can take part in the slum of the MCA space, where demand for high-priced funding is always rampant, despite the laws of economics. Those big funders then take the data from their very own “new funder shops” and backdoor them back to their “big company.” The submissions are then funded as a 1st position to create an illusion of an excellent file, funded by a reputable brand name funder. Of course, this merchant will receive many offers for many more positions which will provide plenty of cash flow to pay the big funder’s 1st position.

These “big funders” will also at times utilize their “new funder” shops to compete on 2nd and 3rd positions. They will ultimately use the same trick to drop a deal to this merchant from their big company, and rely on the “real new funders” who will undoubtedly jump in to act as reliable cleanup hitters, and drop even more cash to drive the other positions home.

Bob’s New Business

By now Bob no longer operates a genuine pizza shop. He simply does not have the time to manage that business, and quite frankly he doesn’t have to. Bob is now an entrepreneur, with various companies and bank accounts, all of which are of course related to the pizza industry. The influx of funding has given Bob an opportunity to walk away from the hot oven and focus on business – the MCA kiting business. MCA kiting is a phrase coined by OPV. The term is derived from a similar practice in the banking industry known as check kiting. It is a form of fraud where a check is intentionally written for a value greater than the balance in the account. Then a second check is written on a different account, to cover the non-existent funds in the first account. This falsely inflates the balance of a checking account, to allow written checks to clear that would otherwise bounce.

The sales on Bob’s banks statements no longer consist of small amounts that shoppers drop for a slice. We now see large deposits and large expenses coming and going as transfers wires, etc. Bob now even imports and exports flour from international flour mills, which explains the large offshore wires.

Bob remembers the days of working hard in a Pizza shop, so he is determined to do the right thing and keep making money from his new companies. Bob studies the guidelines from the various funders, and he makes sure not to mess up. He is an excellent merchant with a perfect MCA payment history. If Bob keeps the process moving forward, he can get funding every few weeks, skim off the top and save the rest for payments until the next advance. This can mathematically go on and on for a long time, where the funders keep paying the merchant to make payments.

The only time this could become an issue for Bob is if the new funders stop opening new shops and the influx of fresh supply comes to an abrupt halt.

The Impact of a Recession on MCA Kiting

Some economists in the MCA space have expressed concern that the upcoming recession will affect the merchants’ sales, and force them to default on their payments. However, this is not a major concern for the legitimate merchants, since many of them are in essential business markets that will not experience a substantial drop in sales, and thus won’t be greatly affected by a recession. But – it is a huge concern for those in the MCA kiting business like Bob. When the recession hits and interest rates rise to rates not seen in a century, investors will be stressed to the max and seek to pull the “huge profits” that they made in the MCA space. There won’t be an influx of new funders that can be relied upon to bail out the previous positions.

As those MCA-kiting merchants collapse, so will the funders who heavily relied on that part of the market share within the space.

Surviving The Recession

On the other hand, the recession will bring major relief and recovery to those funders, new and old, big and small, who were disciplined throughout the inflation period when demand was low. As mentioned earlier, the reason for high inflation rates is easy access to cash. In order to curb inflation the government will raise interest rates to induce lower inflation, which will restrict the easy access to cash. This will usher in a new era of legitimate merchants that find themselves trapped in a credit crunch, who will seek out the MCA option just like Bob did all those years ago.

During these volatile times it is important to always be mindful that your network is your net worth. As a funder, if a large portion of your portfolio consists of merchants who are playing the MCA kiting scheme, then prepare a raincoat for when the recession hits. On the other hand, if you are a funder that remembers why we do not climb the ladder for the bananas, then you are in a perfect position to survive the upcoming recession. The same goes for ISOs, where building solid relationships with solid companies will be the difference between failure or getting a win during the next great recession.

Funders Weigh in on the New Disclosure Law in Virginia

August 10, 2022 “I think there are pros and cons on this law,” said Boris Kalendarev, CEO at Specialty Capital, in regards to the recently enacted sales-based financing disclosure law in Virginia. “I’m on the pro side and I think first and foremost it allows the good funders and the good brokers in the space to operate in the right manner.”

“I think there are pros and cons on this law,” said Boris Kalendarev, CEO at Specialty Capital, in regards to the recently enacted sales-based financing disclosure law in Virginia. “I’m on the pro side and I think first and foremost it allows the good funders and the good brokers in the space to operate in the right manner.”

The law technically went into effect on July 1st, shaking things up for funding providers and brokers alike, particularly through a set of uniform disclosures that are required every time a contract is put in front of a Virginia-based business.

“It holds a broker more responsible for the transaction that they’re going to complete,” said Sharmylla Siew, Senior Underwriter at Lending Valley. “It builds a deeper bond between the broker and the merchant. And it also creates a better bond between the broker and the funder.”

Echoing Siew’s perspective, Kalendarev also believes that being clear creates an honest business space for the broker, merchant, and funder.

“I think transparency is really the right way to run this business. Let’s try to make sure there’s even more transparency,” said Kalendarev.

One intent behind the law is to provide the business customer with all of the pertinent information in a digestible format. Notably, this includes the commission that a broker may be receiving from the funder.

“I do believe that it should be fully transparent on both sides to understand the transaction in full,” said Dylan J. Howell, CEO of Liquidibee. “The merchant should understand that the broker is getting compensated. And if he decides that the broker deserves an additional commission on top of what he’s getting paid from the funder, well, that’s an informed decision between the merchant and broker to come to an agreement with.”

“I do believe that it should be fully transparent on both sides to understand the transaction in full,” said Dylan J. Howell, CEO of Liquidibee. “The merchant should understand that the broker is getting compensated. And if he decides that the broker deserves an additional commission on top of what he’s getting paid from the funder, well, that’s an informed decision between the merchant and broker to come to an agreement with.”

Howell Suggested that some of what is required would be expected in other types of deals.

“If you would go out and buy a $500,000 house, you get to the closing table and you look at the bill, it says it’s $545,000, but the purchase price is 500,000, you would want a reconciliation page to show where that 45,000 of additional capital is going,” Howell said. “And it’s no different than in this transaction, in my opinion.”

Banks and credit unions were exempt from the law but some view targeted regulations like this one as a way to raise the bar and credibility of sales-based financing products in general.

“Merchants who wouldn’t have considered an MCA as a practical form of funding in the past may decide to explore this avenue knowing that the industry is being held to a higher standard of practice,” Howell said.

Siew, of Lending Valley, echoed same.

“I am actually very excited about the new regulations, and I feel that it would make a huge impact on the MCA industry,” she said.