Trump’s Two-For-One Regulation Deal

January 31, 2017Trump’s newest order is that for every new regulation proposed, two must be identified for repeal. If a new regulation goes into effect, the costs must be offset by the repealed regulations. The idea behind it is to strip away costs on small businesses and unburden the system. “There will be regulation, there will be control, but it will be normalized control where you can open your business and expand your business very easily,” Trump said prior to signing the executive order. Watch that below:

Trump later said that “Dodd-Frank is a disaster” and that “We’re going to be doing a big number on Dodd-Frank.”

When he does that “big number,” he should pay close attention to Section 1071 of the law, which many believe the CFPB will try to use to police commercial finance and business-to-business transactions.

Ironically, as Trump works to slash federal rules, states will likely be doing just the opposite. Already in New York, Governor Cuomo’s 309-page budget proposal includes edits to an existing law that would impose strict regulations on all non-bank business finance.

Fintech Hearing Summary (7/12/16)

July 13, 2016 A hearing about marketplace lending put on by the House Subcommittee on Financial Institutions and Consumer Credit covered a wide array of topics on Tuesday. From merchant cash advance to business loans to consumer loans, the witnesses tried to help members of Congress understand the circumstances in their respective industries.

A hearing about marketplace lending put on by the House Subcommittee on Financial Institutions and Consumer Credit covered a wide array of topics on Tuesday. From merchant cash advance to business loans to consumer loans, the witnesses tried to help members of Congress understand the circumstances in their respective industries.

Parris Sanz, the Chief Legal Officer of CAN Capital, explained the differences between a receivable purchase and a loan, a distinction that needed to be made in order to answer some of the questions from Missouri Congressman Lacy Clay.

The questions were generally exploratory and broad. For example, Georgia Congressman David Scott wanted to know what made consumer loans different from business loans. Sanz answered by saying that commercial loans power the economy and that their application was for creating jobs and growing businesses. More to the point, he added that these weren’t hobbyists calling themselves businesses because their average customer has been in operation for at least 13 years and does $1 million to $2 million in revenue a year. These are sophisticated users of capital, he said.

Missouri Congressman Blaine Luetkeyemer, who first read comments he obviously disagreed with that were made by CFPB Director Richard Cordray, repeated the question about the differences between the two. Rob Nichols, the CEO of the American Bankers Association, responded by saying that he didn’t believe the lines were blurred. Cordray had previously said that he believed the lines were indeed blurred, which created some fear in the commercial finance community

Where they might be blurred is in regards to data collection as mandated by Dodd Frank’s Section 1071, something that was only touched upon lightly. Ms. Gerron Levi, Director of Policy & Government Affairs, National Community Reinvestment Coalition, said that we don’t know a lot about marketplace lenders because the data isn’t being collected yet.

While there was some skepticism by the Members over how data was being used by fintech companies to make decisions, it appeared to be early days for a lot of the subjects such as the potential for creating a limited federal charter and whether or not these customers are truly underserved or are just being acquired by marketplace lenders because there is a degree of regulatory arbitrage occurring.

The tone of the hearing was overall neutral in nature.

Meet the Lending Platform With 0% Interest (Kiva)

January 6, 2016 Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Meet Kiva Zip, the anti-Lending Club because the borrowers are far from anonymous and the yield delivered to investors is negative due to inflation.

Angela’s Boutique, which is a real prospect on the Kiva Zip platform, includes a picture of the owner, her bio, endorsements, and comments from supporters.

According to Jessica Feingold, Kiva’s East Coast Manager of Development, “Kiva is the world’s first and largest crowdfunding platform for social good with a mission to connect people through lending to alleviate poverty and expand economic opportunity.”

And just like Lending Club, contributions as small as $25 are accepted. Obviously structured as a non-profit, “Kiva and its growing global community of 1.2 million lenders has crowdfunded more than $775 million in microloans to over 1.7 million entrepreneurs in 83 countries, all the while maintaining a 98% repayment rate,” according to Feingold.

Normally thought of as an overseas endeavor, Feingold said that “in 2011, Kiva launched Kiva Zip, a pilot program in the US that provides 0% interest crowdfunded loans to small business entrepreneurs.” Their underlying purpose and target market sounds very much like those being served by for-profit alternative lenders. “Kiva doesn’t require a minimum FICO score, collateral, or a minimum operations period for the business,” Feingold said.

Since inception they’ve made loans to over 1,800 borrowers in 47 days states, Peru, and Guam.

Notably, Lending Club promises borrowers that their “identity will at all times remain confidential and not be disclosed to anyone,” according to their website. Kiva by contrast is looking to “instill empathy” in their lenders. “We want to show that whether in East New York or Uganda, underserved entrepreneurs are credit-worthy, and will pay you back,” Feingold said. “All of these features on the Kiva websites enhance our ability to do so.”

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

According to the law, no loan underwriter or other officer or employee of a financial institution, or any affiliate of a financial institution, involved in making any determination concerning an application for credit shall have access to any information provided by the applicant about whether or not the business is women-owned or minority owned.

As small businesses often celebrate the heritage of their founders, and at times that can be the entire reason customers buy from them in the first place, the law has presumably put the small business lending world in an awkward position (and that’s why the law should be repealed). Non-profits like Kiva have embraced the very things that make a small business bankable outside of a credit score, like the owner, their background, and their story.

Borrowers on the Kiva Zip platform don’t raise all the money from strangers though. Their credit-worthiness is based on their ability to recruit friends and family to fund a small portion of their loan. The other lenders though of course may make their decisions based on the numbers or entirely on the perceived cultural, racial, or gender values of the borrower, all of the things that the CFPB is attempting to eradicate in the for-profit arena.

I didn’t ask Kiva any questions about Dodd Frank or Section 1071, but many people might empathize with their empathy approach as a way to fund small businesses that otherwise don’t qualify for bank loans. Its reminiscent of the subjective underwriting that a lot of alternative lenders and merchant cash advance companies employ to get deals done that banks won’t touch.

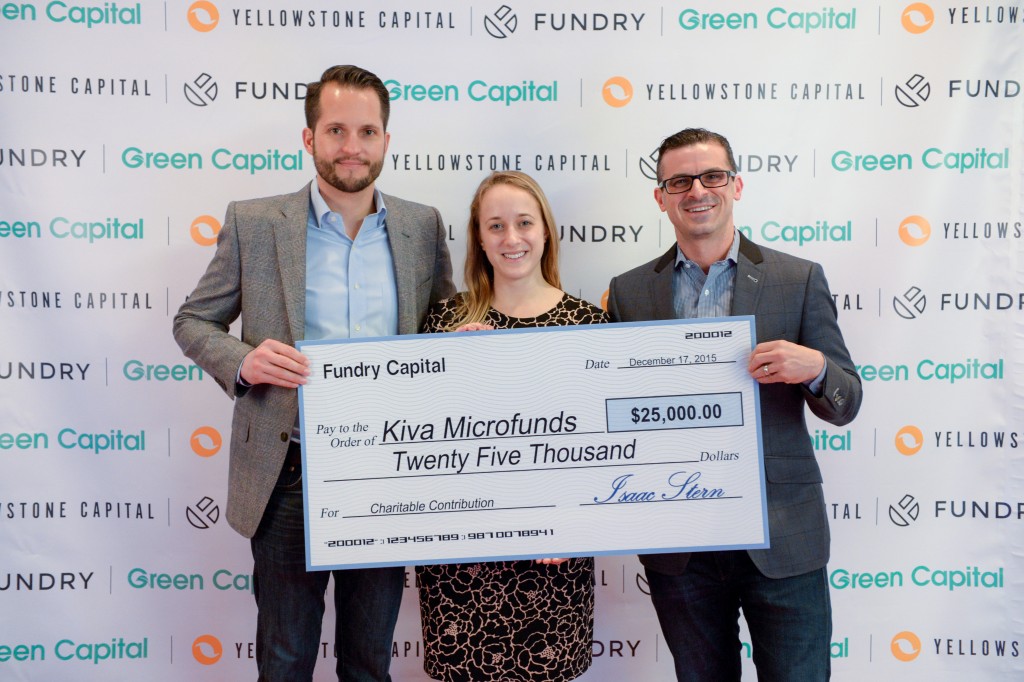

Not so coincidentally, Fundry, Yellowstone Capital’s parent company, donated $25,000 to Kiva just last month to support their cause.

Kiva’s Feingold (pictured at center above) said in regards to that, “Kiva is thrilled to receive a grant from Fundry to further our work to make credit more affordable.”

Year of The Broker Concludes – 2015 Recap

December 31, 2015 It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

But there’s money being made. One broker is on pace to do more than $100 million worth of deals annually after working as a plumber eight years ago. Another went from sleeping in his car to driving a Ferrari. Meanwhile, brokers like John Tucker are basically saying just the opposite. Tucker has repeatedly taken to AltFinanceDaily to preach things like “minimalism,” a practice of living below your means to a point where you can survive, and telling everyone it’s okay to embrace the satisfaction of a middle class life.

So is it the end of days or just the beginning?

In October, initial survey results of top industry CEOs revealed a confidence index of 83.7 out of 100, but out there on the street for the little guy, it’s been a tumultuous year. Things like commission chargebacks have hit brokers at unexpected times, with several funders privately telling us over the year that rogue brokers have closed their bank accounts or frozen the ACH debits in order to avoid giving the commissions back.

In 2015, brokers sued their sales agents and sales agents sued their employing brokers. Deals got backdoored, deals got co-brokered, and soliciting deals anonymously got banned from industry forums. Stacking continued mostly unfettered but is being pursued in the court system by funders allegedly injured by it. Brokers took over Wall Street and are supposedly being watched by regulators. Oh, and robo-dialing? Brokers should probably steer clear of that, just as underwriters should ditch paper bank statements.

It’s a lot to manage. Sometimes for a broker, just losing a deal can make them so sick that they have to go home. That’s apparently what happens when you don’t answer the phone fast enough. At least one said there’s no room left for more competitors so if you were thinking of starting a brokerage now, $2,000 won’t be enough.

But things could be worse. In 2015, IOU Financial was under attack by Russian nuclear scientists, a story that was more truth than exaggeration. In the end, Qwave Capital acquired a 15% stake in IOU.

An OnDeck class action lawsuit that looked bad at first turned out to be mostly based on the words of a convicted stock manipulator with a short position in the stock. The case is still ongoing and OnDeck’s stock price is down 50% from their IPO.

In 2015, two guys lost God but found $40 million (although numerous sources say that number is off).

“Madden” no longer means the football video game and Section 1071 is not a seating area in a stadium.

An RFI turned out to be something not to LOL about. Despite an overwhelming response from lenders and funders, the Treasury isn’t completely sold.

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Lobbying coalitions formed. NAMAA became the SBFA. The CFPB lied and community bankers testified.

But things are looking up. Brokers can obtain outside investments, get acquired, or make millions through syndication.

Bad Merchants are now ending up in more than one bad database, though a deal for the ages slipped through the cracks. Other merchants went to jail. Square went public and brought merchant cash advances along with them. The industry beamed its message through Times Square and one Democratic congressman has asked God to bless it all.

It was a crazy year. Marketplace lending became an acknowledged term (and the name of a conference) and already companies under that umbrella have been linked to presidential candidate (and desperate loser) Jeb Bush and the San Bernardino Terrorists. The FDIC had a few things to say and SoFi went triple-A. Marketplace lending is making a lot of people money, but when looking at the tax implications is there something funny?

In 2015, the big boys shared their wisdom and their figures. Turns out, it was beyond hyperbole. Brokers experienced an incredible rise or they pawned their ferrari to the other guys. Some focused on a specific crop, while others are trying it over the top. California sucked, John Tucker tucked, and one lender got totally F*****. In 2015 some funders got tanked, so in 2016 we’ll all be AltFinanceDaily.

Happy New Year!

CFPB Track Record on Anti-Discrimination Analyses Show Malfeasance

December 11, 2015Congressman David Scott (D), the same congressman that said, “God Bless the online lenders” back in October had some choice words for the Consumer Financial Protection Bureau recently after learning they manipulated data to falsely support evidence of racial bias in lending. According to the Wall Street Journal, Scott called their data “shamefully flawed.”

As explained by the WSJ:

The bureau has been guessing the race and ethnicity of car-loan borrowers based on their last names and addresses—and then suing banks whenever it looks like the people the government guesses are white seem to be getting a better deal than the people it guesses are minorities. This largely fact-free prosecutorial method is the reason a bipartisan House supermajority recently voted to roll back the bureau’s auto-loan rules.

The House of Representatives responded on November 18th by voting 332-96 in favor of stripping some powers away from the CFPB. In a bill, that hopes to be known as the Reforming CFPB Indirect Auto Financing Guidance Act if it is also passed in the Senate and signed by the President, attacks the CFPB’s guidance of the Equal Credit Opportunity Act as it applies to auto lending.

The House of Representatives responded on November 18th by voting 332-96 in favor of stripping some powers away from the CFPB. In a bill, that hopes to be known as the Reforming CFPB Indirect Auto Financing Guidance Act if it is also passed in the Senate and signed by the President, attacks the CFPB’s guidance of the Equal Credit Opportunity Act as it applies to auto lending.

“Bulletin 2013-02 of the Bureau of Consumer Financial Protection (published March 21, 2013) shall have no force or effect,” the bill states outright.

Bulletin 2013-02 addressed the auto lending industry by saying, “the ECOA makes it illegal for a ‘creditor’ to discriminate in any aspect of a credit transaction because of race, color, religion, national origin, sex, marital status, age, receipt of income from any public assistance program, or the exercise, in good faith, of a right under the Consumer Credit Protection Act.”

The CFPB reviewed loan data as expected to see if there were racial disparities but disturbingly did not actually know the race of the borrowers in many cases. So they guessed, according to the WSJ, by reviewing the last names and addresses of the borrowers. When being shown the results of their guesses against a sample of data for which they actually had racial background data, the CFPB only successfully guessed correctly 54% of the time. Despite being aware of this, the CFPB sued Honda, Fifth Third Bank, and others for discriminatory lending practices. Honda was pressured into settling for $24 million and Fifth Third for $18 million even though the CFPB’s data and methodology were false.

The House bill also requires that the CFPB publicly disclose the methodologies and analyses used to assess discrimination in auto financing, lest they continue to manufacture their own data, draw conclusions based on that, and then extort corporations for tens of millions of dollars through lawsuits, investigations and public shaming.

88 Democrats in the House joined their Republican colleagues in passing this bill.

This kind of blatant malfeasance is especially alarming considering the CFPB is already licking their chops to collect data on small business lending so that they can test it for racial and gender disparities as well.

As small business underwriting is markedly different from the commoditized world of consumer lending, it would be near impossible for a pious, law-abiding, and even omnipotent CFPB to make meaningful determinations. Considering that the CFPB we have acts in a manner as described above, small business lenders have a lot to worry about over the implementation of Dodd Frank’s Section 1071.

CFPB Officially Begins Work on Small Business Data Collection Rule

November 23, 2015 On Friday, the CFPB issued its semiannual update to its rulemaking agenda. The agenda lists the Bureau’s major current and long-term initiatives. Long listed as a long-term item, the Small Business Data Collection rule required by section 1071 of Dodd-Frank is listed on the update as a current initiative.

On Friday, the CFPB issued its semiannual update to its rulemaking agenda. The agenda lists the Bureau’s major current and long-term initiatives. Long listed as a long-term item, the Small Business Data Collection rule required by section 1071 of Dodd-Frank is listed on the update as a current initiative.

The move is unsurprising given the number of lawmakers that have publicly called for implementation of the rule. CFPB director Richard Cordray also recently mentioned that the Bureau would begin its initial work on the rule early next year.

In the update, the Bureau states that it plans to build off of its recent revision to the home mortgage data reporting regulations as it develops the new Small Business Data Collection rule. The first stage of the CFPB’s work will focus on outreach and research. This will be followed by the development of proposed rules concerning the type of data to be collected as well the procedures, information safeguards, and privacy protections that will be required of the small business lenders that will report information to the Bureau.

CFPB Signals Alarming Interest in Small Business Lending

November 10, 2015 The Consumer Financial Protection Bureau posted an alarming job opportunity on LinkedIn last month for the position of Assistant Director for Small Business Lending Markets. Ominously self-labeled as an “Expression of Interest” rather than a job opening since the job is not currently open to applications yet, the CFPB has inadvertently revealed its own expression of interest in small business lending.

The Consumer Financial Protection Bureau posted an alarming job opportunity on LinkedIn last month for the position of Assistant Director for Small Business Lending Markets. Ominously self-labeled as an “Expression of Interest” rather than a job opening since the job is not currently open to applications yet, the CFPB has inadvertently revealed its own expression of interest in small business lending.

If there was any doubt that data collection required under Section 1071 of Dodd Frank was never going to happen, the CFPB also revealed that there will not only be a person responsible for small business lending, but in fact an entire team. And they won’t just be collecting data, but they’ll be monitoring it, analyzing it, interpreting it, and advising on rulemaking, according to the listing.

Candidates are being offered a once-in-a-career opportunity to make the market for small business finance fairer and more transparent.

So much for just collecting data, the CFPB apparently plans to directly insert itself into the fairness of transactions conducted between commercial entities.

Perhaps, we are not too far off from a world like this:

Check out my thoughts about the troubling narrative developing around small businesses in the Sept/Oct magazine issue of AltFinanceDaily.

Blurring Small Business: A Troubling Narrative is Gaining Steam

October 30, 2015Almost 18 months ago at LendIt’s 2014 conference, Brendan Carroll, a partner and co-founder of Victory Park Capital said that in regards to business lending, “the government doesn’t have the same scrutiny on this sector as it does in the consumer space.”

This double standard is the crux of American capitalism. In business you can win or lose, be smart or foolish, risk it all or play it safe. Government regulations don’t let the average consumer be subjected to the same stakes. They are viewed to be at a natural disadvantage against businesses and thus there are laws to protect them, and perhaps rightly so.

Since entrepreneurship is a choice, businesses and the people that own businesses are held to a higher standard of acceptable risk taking. In the free market, the pursuit of profit holds the system together.

This economic worldview is part of the reason why entrepreneurial TV shows such as Shark Tank are so popular. In the Tank, contestants can just as easily walk away with a terrible deal as they can a good one. And when bad deals get made, and they do, I’ve yet to see regulators descend on the set to fine or arrest Daymond John, Kevin O’Leary, or Barbara Corcoran.

But Shark Tank features entrepreneurs on a remote stage detached from their daily environment, giving it the look and feel of a game show. If you want to see cold hard dealmaking with mom-and-pop shops on an up close and personal level, just watch CNBC’s The Profit. On the show, small business expert Marcus Lemonis does not sugarcoat what he is. “I’m not a bank. I’m not a consultant. And I’m not the fairy godmother,” he bluntly told one small business owner. It doesn’t matter if it’s a family owned store or a full fledged corporation, Lemonis is looking to make a deal and make some money. When it comes to business, he is well… all business.

Just as the CFPB hasn’t shut down Shark Tank, (which one has to wonder if they’ll be subject to Reg B of Dodd Frank’s Section 1071) none of Lemonis’ deals have been scrutinized by a Federal Reserve study, nor has the Treasury Department issued an RFI to better understand why entrepreneurs go on the show in the first place.

It’s no wonder then at LendIt 2014, Carroll also said that there wasn’t the same sort of moral hurdle when it came to institutional capital investing in business lenders as opposed to consumer lenders.

Moral was a telling word choice because the morality of certain commercial transactions have recently come under fire by groups claiming to represent small businesses. The premise of their argument is that commercial entities are no more sophisticated than consumers, that a corporation and the average joe are equal in their ability to take risks and make decisions for themselves.

Their evidence is that sometimes in business-to-business transactions, particularly in lending, one side accepts terms that would be considered far outside the norm for consumers, terms that violate a moral threshold. One has to wonder where a loan with an infinity percent interest rate ranks on this morality scale, a deal that’s actually been made and accepted several times on a TV show. Referred to as a “Kevin deal” since they are Kevin O’Leary’s favorite, the borrower is obligated to pay a perpetual royalty on top of repaying the loan itself. In simple terms, it’s a loan that can never be paid off.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

The fact that Wicked Good Cupcakes decided what made sense for them and was happy about it, damages the storyline that businesses need to be saved from their own decisions. But there’s another problem, government entities themselves may be inadvertently effectuating this false narrative by inferring incorrect conclusions from their own research.

Nowhere is this more evident than in a report recently published by the Federal Reserve Bank of Cleveland that analyzed small businesses and their understanding of “alternative lending.” The report shared the results of two focus groups that had been shown terms for three hypothetical products that supposedly represented actual products in the real world.

Unsurprisingly, the report concedes “when comparing the products, participants initially reported the three were easy to compare and that they had all the information to make a borrowing decision.” But the researchers pressed on until they got an answer that fit their expectations, that small businesses are confused when it comes to money and finance.

In a hypothetical scenario where a commercial entity sold $52,000 of future receivables for $40,000 today, it stated that the “lender” would withhold 10% of each debit/credit card transaction until satisfied. Participants were then asked to guess the interest rate on this loan if they paid it back in one year. That caused a lot of folks to scratch their heads and that’s because it was a trick question.

The question itself introduced conflicting facts and lacked crucial variables to make an intelligent guess. Nevermind that respondents prior to that question said that there was “nothing confusing” about the products presented as is. The original feedback should’ve been enough. Below are some of the responses offered before they were deliberately tricked.

- “Nothing Confusing.”

- “No, it’s pretty straight-forward.”

- “I can’t think of anything more I would need to see, really.”

- “This is enough info for me to make a decision.”

The researchers concluded however that the answers to their trick question suggested there were “significant gaps in their understanding of the repayment repercussions of some online credit products and the true costs of borrowing.”

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

But even if that was the case, at what point does confusion become unfair in a purely commercial transaction? And what would be an appropriate remedy?

We’ve been down this road before where federal regulators have set mandatory disclosures in order to bring transparency to a lending environment believed to be obscure. And just recently on September 17th, 2015, the House Committee on Small Business Subcommittee on Economic Growth, Tax and Capital Access pressed community bankers on the impact of such measures dictated by Dodd-Frank.

Congressman Trent Kelly asked if all the added new pages to loan agreements make it easier for their borrowers to understand. “Do they understand what they’re signing?” he asked.

B. Doyle Mitchell Jr., the CEO of Industrial Bank that was speaking on behalf of the Independent Community Bankers of America responded that they do not. “It is not any more clear,” he answered. “In fact it is even more cumbersome for them now.”

If anything, the Federal Reserve study offered compelling evidence that small businesses are happy with the way alternative lenders are currently disclosing their terms. It is only when government researchers tricked them that they became confused. That should say it all.

One consequence of entrepreneurship is that businesses are not created equal in their ability to assess financial transactions and no amount of disclosures or intervention can save them. There must be losers in order for there to be winners.

Case in point, there are lenders out there doing deals so lopsided that they actually turn to each other and say, “I can’t believe she took that.” Such is the case of RuffleButts, a children’s fashion line that appeared on Shark Tank in 2013.

“When they wake up, they’ll realize they messed up,” said Mark Cuban in reference to the deal Lori Greiner proposed and closed. An article on BusinessInsider.com covered the episode and unabashedly concluded, “Shark Tank isn’t a charity. The investors are putting in their own money, so they have every incentive to push to get the best deal possible for themselves.”

Shark Tank has risen in popularity because it is a reflection of a culture that believes dealmaking, both good and bad, is inherent to the endeavor of entrepreneurship. When a bad deal is made, regulators don’t come on the show to urge a do-over.

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

And if the Federal Reserve study indicated anything, it’s that business owners feel there’s nothing confusing about these deals.

So it would seem that everything as Americans know it, watch it and understand it, is business as usual.

Even Brendan Ross, the president of Direct Lending Investments, was quoted by the BanklessTimes as saying, “I want to emphasize there’s absolutely nothing novel about lending money to businesses. This isn’t some phenomenon we are rediscovering. There isn’t going to be increased regulation because this isn’t new.”

Perhaps the only thing that could be considered new is that loan sizes have gotten smaller and the types of products small businesses can access has diversified. Along the way, some of these new startups have decided to offer products in line with a self-professed moral code, which is to deliberately lend money at a loss and lash out at lenders who seek profit.

There’s a term for lending startups that don’t make money. They’re called “failed startups.” By casting small businesses as being no different from unsophisticated consumers, it’s quite possible that shows like Shark Tank and The Profit would become illegal in the process. Disclosures meant to help make things more transparent could actually make things less clear and more cumbersome, just as they have in the past.

I don’t think anybody is in favor of small business failure or an environment where confusion prevails, including the guys making infinity percent interest loans like Kevin O’Leary. But if the goal is to increase transparency, it should be in a way that businesses on both sides are content with.

The Federal Reserve study showed the system is working well as is and that prescribing mandatory changes to fit some universal standard would only serve to usher in an era of confusion that everyone is trying to avoid. Lenders can always do better to serve their clients, but the free market must prevail. As Mitchell, Industrial Bank’s CEO said when he testified in front of the Small Business Committee, “the problem with Dodd-Frank is you cannot outlaw and you cannot regulate a corporation’s motivation to drive profit at all costs so while it has a lot of great intentions in over a thousand pages, it has not helped us serve our customers any better.”