Online SME lender Capify secures $125 million credit facility from Pollen Street Capital

April 29, 2024Leading online SME lender Capify has today secured a $125 million credit facility from Pollen Street Capital (“Pollen Street”), an alternative asset manager dedicated to investing within financial and business services.

The new facility will support the lender’s ambitious future growth plans and provide working capital to thousands of SMEs over the coming years.

Founded initially in the United States in 2002, Capify was one of the world’s first online alternative financing companies for SMEs. It was launched in the UK and Australia in 2008, against the backdrop of the global financial crisis, when many small and medium-sized businesses were struggling to access vital funding from banks. Last year it was named the UK Credit Awards SME Lender of the Year (up to £1m).

“We are extremely excited about our future relationship with Pollen Street, a capital provider with a proven track record of partnering with impactful and innovative businesses. This deal represents another significant milestone for Capify and underlines the strength of our business model in providing fast, flexible and responsible support to SMEs”, said David Goldin, Founder and CEO of Capify.

“We are absolutely delighted to secure this financing deal with Pollen Street” added John Rozenbroek, CFO/COO at Capify. “The credit facility will enable us to continue on our growth trajectory while offering even more attractive and innovative solutions to the growing number of small businesses in need of funding. We are passionate about the vital role SMEs play in the success of any economy . This new multi-year credit facility allows us to provide much-needed access to capital for SMEs to help them manage and prosper, whilst also enabling us to deliver on our own growth plans”.

“With continued investment in our platforms and customer experience, we will streamline our processes and provide even faster decisions to brokers and SMEs,” said Rozenbroek. “These enhancements underline our commitment to leveraging technology to meet the fast-evolving needs of small businesses, ensuring they have quick access to capital and can seize growth opportunities more effectively.”

“We are impressed by Capify’s seasoned management team and their enduring presence in the market. Since its inception in 2008, Capify has been at the forefront of online SME lending in both the UK and Australia, consistently demonstrating its commitment to the sector. Capify successfully addresses the needs of the underserved market segment, resulting from a chronic undersupply of bank financing, and promotes both financial inclusion as well as regional economic growth, aligning closely to Pollen Street Capital’s ESG framework. We are delighted to partner with Capify and support their ongoing growth” added Ethan Saggu, Investment Director at Pollen Street Capital.

About Capify

Capify is an online lender that provides flexible financing solutions to SMEs seeking working capital to sustain or grow their business. Originally started in the US over twenty years ago, the fintech businesses have been serving the SME market in the UK and Australia for over 15 years. In that time, it has provided finance to thousands of businesses, ensuring the vibrant and vital SME community can meet the challenges of today and the opportunities of tomorrow.

For more details about Capify, visit:

http://www.capify.co.uk

http://www.capify.com.au

About Pollen Street Capital

Pollen Street is a purpose led and high performing private capital asset manager. Established in 2013, the firm has built deep capability across the financial and business services sector aligned with mega-trends shaping the future of the industry. Pollen Street manages over £4.2bn AUM across private equity and credit strategies on behalf of investors including leading public and corporate pension funds, insurance companies, sovereign wealth funds, endowments and foundations, asset managers, banks, and family offices from around the world. Pollen Street has a team of over 80 professionals with offices in London and the US.

For more information, visit: www.pollenstreetgroup.com

Media enquiries

Capify

Ash Yazdani

Ash.yazdani@capify.co.uk

Pollen Street Capital

PollenStreetCapital-LON@fgsglobal.com

Backdooring Deals? You’re a Loser

April 24, 2024 “Backdooring is just for losers,” says Thomas Chillemi, founder and CEO of Harvest Lending, a small business finance brokerage. “Like I think anybody who participates in it is just a loser.”

“Backdooring is just for losers,” says Thomas Chillemi, founder and CEO of Harvest Lending, a small business finance brokerage. “Like I think anybody who participates in it is just a loser.”

Backdooring, as colorfully referenced by Chillemi, is a colloquial term used widely across the industry to describe how leads, apps, or entire deals are stolen from brokers. The deal gets submitted through the front door and then leaks out the back door to an unauthorized third party. Chillemi sums it up as such: “backdooring is ‘I secured a lead, I secured a file in some way, shape or form. And that merchant is being contacted through my efforts somehow that I didn’t give permission to.'”

It’s a scenario that’s been top of mind at brokerages across the country for years, and it’s a problem that’s getting worse, according to sources that AltFinanceDaily has spoken with.

“I would say backdooring is the worst of the worst right now,” says Josh Feinberg, CEO of Everlasting Capital, another small business finance brokerage. “I think as far as rogue employees go at direct funders, it’s the worst it’s ever been.”

Feinberg’s reference to “rogue employees” is just one such way that backdooring can occur. It can be an employee of a lender, management of a lender, an employee of the broker, a broker pretending to be a lender, and possibly in a worst case scenario even a cyber intruder like a hacker. Sometimes it’s a clandestine operation structured in a way to make it difficult for the broker to detect that their client’s file has been intercepted while other times backdooring is such a normalized function of one’s business that accepting a submission from a broker and then shopping it elsewhere to circumvent them is practically firm policy and done on an automated basis.

Some of the more seasoned brokers who are used to being on guard with what a lender intends to do with their file advise that their peers approach any proposed ISO agreement with a fine-tooth comb to establish what is or isn’t allowed. After all, if the agreement grants the lender the contractual right to backdoor the broker, is it really backdooring?

Others say the contract’s language can only carry the relationship so far.

“I only try to board up with people that seem to be good actors, but then you never know what an employee might do, right?” says Chillemi.

Whether it’s a jaded underwriter, a slick admin, or Bob in accounting who never says a peep, it only takes one individual to set eyes on an application to be in a position to transfer the information elsewhere for personal gain. AltFinanceDaily examined this subject in years past and learned the lengths that rogue employees go through to extract deal data. For example, when one funding company blocked the ability to transfer data outside of the company’s network, an employee took photos of their screen with their phone. When the employer banned cell phones in the office in response, one employee wrote down deal data on scrap paper, threw it in the garbage, and then returned to the office building after hours to try and fish it out of the dumpster.

Whether it’s a jaded underwriter, a slick admin, or Bob in accounting who never says a peep, it only takes one individual to set eyes on an application to be in a position to transfer the information elsewhere for personal gain. AltFinanceDaily examined this subject in years past and learned the lengths that rogue employees go through to extract deal data. For example, when one funding company blocked the ability to transfer data outside of the company’s network, an employee took photos of their screen with their phone. When the employer banned cell phones in the office in response, one employee wrote down deal data on scrap paper, threw it in the garbage, and then returned to the office building after hours to try and fish it out of the dumpster.

The absurdity of that visual alone implies there must be big bucks in the backdoor business. Indeed, according to screenshots forwarded to AltFinanceDaily of what appears to be an underground Whatsapp group, backdoored deals are currently being marketed for sale with bank statements, social security numbers, and all. A single fresh backdoored file can go for $20 – $35 or buyers can purchase them in bulk, up to 600 at a time, for a discounted price.

“Fresh Packs” apparently fetch more because the applicants may not have signed a funding contract with anyone yet and are theoretically more warm to doing a deal even if they’re not quite sure how the company approaching them got all of their information. And it’s this speed and efficiency of the backdooring happening that’s making things extra difficult for brokers. For Chillemi, he says the backdooring in earlier years would reveal itself when someone would try to call his customer a month or two after the fact. “Like even if it happened after two or three days that felt really fast,” he says. “But now, you’re talking hours, like these people have it within hours and I just don’t even know how anybody could really compete with that.”

Brokers, ready for this, developed a tactic that is still used today as a front-line defense mechanism. They replace the applicant’s email address and phone number on the application with ones they control, so that when an attempted backdooring occurs, the caller is unsuspectingly contacting the very broker they are trying to steal the deal from. The result? They’re caught red-handed.

Brokers, ready for this, developed a tactic that is still used today as a front-line defense mechanism. They replace the applicant’s email address and phone number on the application with ones they control, so that when an attempted backdooring occurs, the caller is unsuspectingly contacting the very broker they are trying to steal the deal from. The result? They’re caught red-handed.

“I got a text from somebody claiming that they worked at Fidelity,” says Chillemi. “They texted me a picture of my own application. They’re so brazen that they’re just texting the merchant… they thought they were texting the merchant.”

Not only was the Fidelity component a deception, but the mistake of texting the broker who was just waiting to catch them is causing the backdoor shops to evolve. New backdoor callers know the application contact info might be booby-trapped so they’re now skip-tracing the applicants on an automated basis and getting their real contact info and using that instead.

For Feinberg at Everlasting, he says the method of substituting out an applicant’s contact info is not something they do, though he’s aware that it’s done by others in the working capital space. He says that it’s not something that would really be tolerated in the equipment finance side of the industry which operates much cleaner with no backdooring, at least in his experience. The lenders there hate it and everyone involved needs to be able to communicate with the customer. It’s just the working capital deals where all these problems happen.

“It’s defeating, and it’s a very very difficult thing to diagnose,” Feinberg says. He adds that the feeling is worse when realizing that it has happened even when submitting to top tier A players. There’s no delay either. He says that the customer can be called literally within the same hour of submitting it, which puts them in an awkward position.

“They lose complete trust in our company,” Feinberg says. “And it makes it very difficult to be able to work with these clients.”

According to Chillemi of Harvest, “Most of the time what happens is the merchant calls us and says, ‘Now I’m getting all these phone calls people saying they’re working with you,’ and it’s just kind of like an embarrassment of where I’ve got to explain to this person that somebody at these companies leaked their information that wasn’t supposed to. And it just makes me look bad, right?”

According to Chillemi of Harvest, “Most of the time what happens is the merchant calls us and says, ‘Now I’m getting all these phone calls people saying they’re working with you,’ and it’s just kind of like an embarrassment of where I’ve got to explain to this person that somebody at these companies leaked their information that wasn’t supposed to. And it just makes me look bad, right?”

Another owner of a large broker shop, who did not authorize his name to be used in connection with this story, says that while everyone’s mind immediately goes to the lending companies, the most common source of backdoored deals is actually from rogue employees inside the brokerages themselves. Whether it’s the rep backdooring their own deals to circumvent splitting commissions with their employer or someone else in the chain that has access to the data, his advice was that brokerage owners first need to look extremely inwards before pointing fingers outwards. Investing in proper security is critical, he says.

But assuming that base is covered, Feinberg says that brokers should do a background check on the lenders and interview them like a lender would interview a merchant for funding.

“We absolutely look into the agreements that we sign but a lot of due diligence happens just on the first phone call,” Feinberg says. “Just on the first phone call we can judge whether this is going to be a real lender…”

A key question to ask, he says, is how compensation works. And that’s because an individual lender will have a defined fixed system whereas a backdoor broker pretending to be a lender is subject to the different compensation structures they have at all their different lending relationships and would not be able to guarantee any fixed commission pricing to the broker they are trying to trick into submitting, that is if they are intending to pay them out a percentage of the deals they backdoor them on in the first place.

“Trust is the number one thing with us,” Feinberg says. “And if trust gets broken, then it’s over. So we really try to work with people that we know personally. And the way that we’ve met people personally is through trade shows, specifically AltFinanceDaily events.”

Chillemi argues that someone who tries to make their living off of backdoored deals are not salespeople at all, but as he reiterates, losers.

“[the backdoor broker] knows he’s a liar,” says Chillemi, “He’s calling these people saying he’s an underwriter… he’s not strong, he’s not learning. They don’t know what they’re doing. They’re putting the lenders at risk.”

Stop the Debt Settlement People, Funders Come Up With Merchant-Friendly Alternative

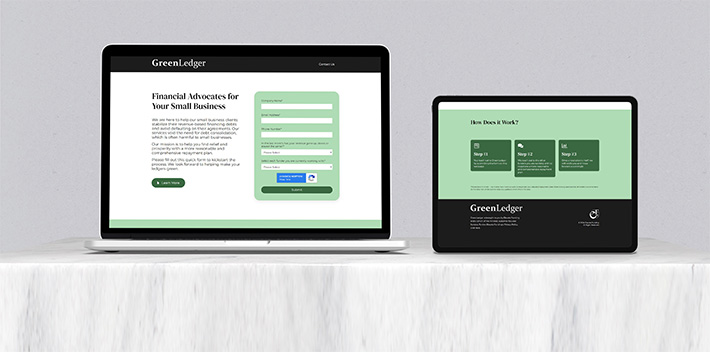

April 3, 2024 Are debt settlement “advisors” interfering with your contracts and putting your merchants in a bad spot? The industry is now taking the reins on a solution. It’s called GreenLedger, a platform for funders to work together on resolving a merchant’s situation with no debt settlement middlemen encouraging an intentional default, taking fees, and making false promises.

Are debt settlement “advisors” interfering with your contracts and putting your merchants in a bad spot? The industry is now taking the reins on a solution. It’s called GreenLedger, a platform for funders to work together on resolving a merchant’s situation with no debt settlement middlemen encouraging an intentional default, taking fees, and making false promises.

Founded by Elevate Funding CEO Heather Francis, who aims to eventually make it a non-profit, merchants would go to this industry-collaborative platform, indicate who they have open contracts with, and the platform would notify the funders directly.

“From there, the primary points of contact at each funder can get together to come up with a more specific and comprehensive payment plan that works with the merchant’s needs,” said Francis. “GreenLedger’s mission is to work directly with our small business clients to stabilize their revenue-based financing arrangements and avoid breaching their agreements, eliminating the need for potentially predatory middlemen.”

The platform has already been generating interest.

“As an attorney deeply committed to the financial empowerment of small and medium-sized businesses, I am thrilled to endorse Elevate Funding’s creation of GreenLedger,” said industry attorney Patrick Siegfried. “This initiative represents a pivotal step in our ongoing battle against the increasing prevalence of unscrupulous entities in the commercial finance debt settlement industry. Far too often, these bad actors employ deceptive sales tactics and bind clients with unfair contracts, leading not to the promised debt relief but to further financial strain for small businesses. GreenLedger, with its dedication to transparency and integrity, stands as a true avenue for business owners seeking legitimate and effective financial solutions. Its mission to root out malpractices and safeguard the interests of small businesses is not just commendable but essential in today’s challenging economic landscape.”

To learn how you can participate and cut the debt settlement people out of the picture, attend this webinar on April 16th.

How Merchant Cash Advance Companies Can Avoid Problems This Tax Season

April 2, 2024David Roitblat is the founder and CEO of Better Accounting Solutions, an accounting firm based in New York City, and a leading authority in specialized accounting for merchant cash advance companies. To connect with David or schedule a call about working with Better Accounting Solutions, email david@betteraccountingsolutions.com.

In the fast-paced and ever changing world of cash advance, tax season can often present a labyrinth of compliance and reporting challenges. These challenges are not just bureaucratic hurdles that must be overcome; they also serve as crucial tests of a company’s financial health and operational integrity. Given the intense scrutiny the cash advance industry faces from regulatory bodies, particularly in light of recent industry shaking events, alongside the unique nature of how its financial transactions can be structured, ensuring tax compliance is not just advisable—it’s essential. Let’s discuss frequent speed bumps cash advance companies encounter during tax season, and some solutions for these problems.

In the fast-paced and ever changing world of cash advance, tax season can often present a labyrinth of compliance and reporting challenges. These challenges are not just bureaucratic hurdles that must be overcome; they also serve as crucial tests of a company’s financial health and operational integrity. Given the intense scrutiny the cash advance industry faces from regulatory bodies, particularly in light of recent industry shaking events, alongside the unique nature of how its financial transactions can be structured, ensuring tax compliance is not just advisable—it’s essential. Let’s discuss frequent speed bumps cash advance companies encounter during tax season, and some solutions for these problems.

Misclassification of Income and Advances

One of the most significant stumbling blocks for cash advance businesses lies in the misclassification of the funds they advance to customers. This misstep can lead to serious tax implications, distorting the financial understanding of a company in the eyes of the law. A robust accounting system that accurately differentiates loans, advances, and income is not just a recommendation; it’s a necessity. Each category must be meticulously reported for tax purposes, a task that underscores the importance of seeking guidance from a tax professional well-versed in the nuances and implications of these classifications.

Misreporting Income

A common oversight among cash advance companies is the inaccurate reporting of income. Whether it’s underreporting or misclassifying earnings, the repercussions can be severe, and include the possibility of triggering an audit or incurring a severe financial penalty. The remedy? An accounting software tailored for the funding industry (such as Orgmeter, MCA-Track, OnyxIQ, Centrex, or LendSaas), capable of automating the calculation and reporting all necessary metrics and income. This ensures not only compliance but also a transparent overview of a company’s financial health that benefits you as well.

State-Specific Tax Obligations

Just over 5 years ago, Wayfair was successfully sued by South Dakota for failing to tax online sales even though they had no physical presence in the state, beginning a new era of legal understanding of state tax obligations in the internet and cross-state trade era.The complexity of tax compliance is magnified for cash advance companies operating across state lines, each with its unique tax laws and regulations. This multi-state maze can easily lead to oversight or misunderstanding, risking non-compliance. The solution is twofold: developing a comprehensive compliance checklist for each state and consulting with tax professionals who specialize in navigating these multi-state operations. Together, these strategies form a bulwark against the many possible blind spots of state-specific tax obligations.

Documentation for Audits

Not having the correct documentation and record-keeping on hand can transform a routine tax audit into a nightmare scenario, and cause businesses to be slapped with heavy penalties and fines. To counter this risk, cash advance companies need to maintain meticulous records of all transactions. Experts often recommend businesses conduct regular audits, whether internal or external, to ensure these records are both accurate and will back you up when they are needed.

Planning for Tax Liabilities

Perhaps one of the easiest mistakes to avoid is not adequately planning for surprise tax liabilities. Without planning in advance and setting aside sufficient funds to cover these obligations, companies can find themselves in a precarious cash flow situation when taxes are due. A proactive strategy to counter that involves specifically marking off a portion of income in a dedicated account for unforeseen expenditures (tax liabilities included), calculated with an estimated effective tax rate. This approach, developed with the assistance of a tax professional, can prevent the unwelcome surprise of a hefty tax bill when you’re not ready for it.

At the end of the day, tax compliance, while definitely not fun, should not be viewed (just) as a regulatory pain-in-the-butt, but as a way to ensure a cash advance business’s success and longevity. By embracing proactive tax planning and compliance, companies can not only successfully navigate the complexities of tax season but also reinforce the integrity and sustainability of their business and ensure their success and viability for years to come, free from any stress or government microscope.

NYC Promotes its Own Online Business Loan Marketplace

March 17, 2024 There was so much demand for NYC’s experimental Small Business Opportunity Fund last year that it had to stop accepting applications after just 3 weeks. The program, however, ultimately enabled 1,046 businesses to collectively borrow $85 million at a low interest rate of only 4%. While the Mayor’s office has declared it a major success it is now encouraging anyone else seeking funds to use its relatively new online business loan marketplace called NYC Funds Finder.

There was so much demand for NYC’s experimental Small Business Opportunity Fund last year that it had to stop accepting applications after just 3 weeks. The program, however, ultimately enabled 1,046 businesses to collectively borrow $85 million at a low interest rate of only 4%. While the Mayor’s office has declared it a major success it is now encouraging anyone else seeking funds to use its relatively new online business loan marketplace called NYC Funds Finder.

Facilitated by Next Street, a b2b platform whose co-CEO Michael Roth is a former interim chief of the SBA, NYC Funds Finder promises to connect business owners with capital products that are “non-predatory and have been screened to ensure fair and transparent pricing and terms.”

An example of some of the lenders on the platform include Lendistry, Accompany Capital, and SmartBiz. APRs tend to range roughly from 7% to 19%.

“NYC Funds Finder serves New York City’s small businesses by aggregating funding options from many of [the NYC Department of] Small Business Services (SBS) and Next Street’s trusted partners,” said an official announcement that went out in September. “Additionally, the platform makes it easy for the business owner to connect with a free advisor if they need help navigating or applying for capital. This partnership with trusted SBS advisors is key for small businesses to access the best financing options for their business.”

Coincidentally, the SBA has also been pushing its own online business loan marketplace as of late. The SBA’s Lender Match tool has 1,000 SBA lenders and 257 community based lenders on its platform already.

What Big Publicly Traded Companies Say About Merchant Cash Advances

March 13, 2024AltFinanceDaily examined the public messaging from some of the largest publicly traded merchant cash advance facilitators in the US and this is what it found:

SHOPIFY

A merchant cash advance is a purchase of your future sales, also known as receivables. If your application for funding is accepted, then Shopify provides you a lump sum of money for a fixed fee. Under the Shopify capital agreement, this lump sum is known as the amount advanced, and the total to remit is the amount advanced plus the fixed fee. In return, you pay Shopify Capital a percentage of your daily sales until Shopify receives the total to remit. The percentage of your daily sales that you must remit to Shopify is known as the remittance rate. The amount advanced and the remittance rate depend on your risk profile.

For example, Shopify Capital might advance you 5,000 USD for 5,650 USD paid from your store’s future sales, with a remittance rate of 10%. The 5,000 USD amount that you receive is transferred to your business bank account specified in your admin, and Shopify Capital receives 10% of your store’s gross daily sales until the full 5,650 USD total to remit has been remitted. You have the option, at any time, to remit any outstanding balance in a single lump sum.

There is no deadline for remitting the total to Shopify Capital. The daily remittance amount in USD is determined by your store’s daily sales, because the remittance rate is a percentage of your store’s daily sales. The remittance amount is automatically debited from your business bank account.

DOORDASH

DoorDash Capital is a cash advance, not a loan. With a cash advance, the offer is based on your sales and account history, and includes a simple, transparent one-time fee that you’ll know before you decide to accept the offer. A loan operates using interest, which can compound over time, and often includes other fees in addition to the stated interest rate.

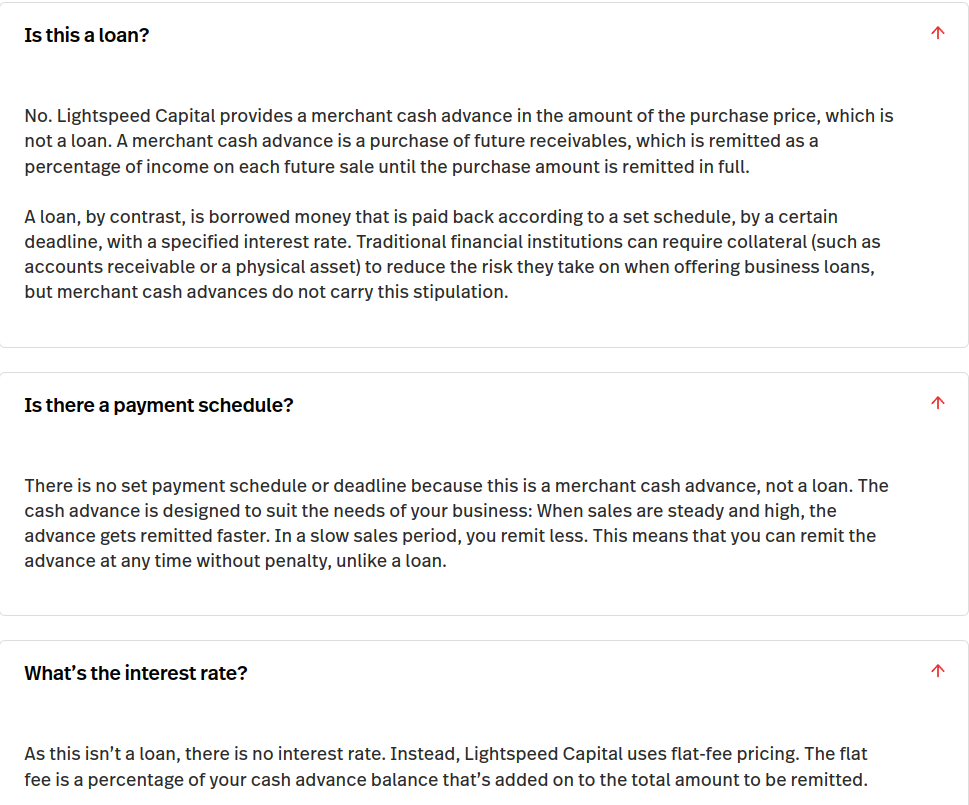

LIGHTSPEED

AMAZON

A [merchant cash advance is a] non-revolving sum of funding with flexible payment, no personal collateral required and no late fees. With flexible payment, no personal collateral required and no late fees, a merchant cash advance provides sellers funding to help run and grow their business. Unlike interest-bearing loans, the advance ties payment to a portion of a seller’s future sales for a fixed capital fee, there are no additional fees or interest charged.

NERDWALLET

Fixed withdrawals from a bank account

Merchant cash advance companies can also withdraw funds directly from your business bank account. In this case, fixed repayments are made daily or weekly from your account regardless of how much you earn in sales, and the fixed repayment amount is determined based on an estimate of your monthly revenue.

PAYPAL

A merchant cash advance is not a loan, but rather a type of financing that business owners pay back with a percentage of their future sales.

Amazon Discontinues Its In-House Business Loans

March 9, 2024 After AltFinanceDaily reported that Amazon’s on-balance-sheet business loan receivables had remained steady throughout 2023, the company has abruptly decided to terminate its in-house lending program altogether.

After AltFinanceDaily reported that Amazon’s on-balance-sheet business loan receivables had remained steady throughout 2023, the company has abruptly decided to terminate its in-house lending program altogether.

Through an email confirmed to Fortune, Amazon ended its in-house term loan business on March 6. That same story says that they will continue to work with third party lenders and funders as they have been doing for a while. Some of their partners include Lendistry, SellersFi, and Parafin.

The in-house program had been running since 2011 and was first discovered by AltFinanceDaily in 2013.

While the company was shy about disclosing origination figures, it carried approximately $1.3B in loan receivables on its books throughout last year.

The Amazon news coincides with the announcement that business loan rival Funding Circle has decided to exit the US market. Funding Circle US is currently up for sale.

Wow we sort of called this @amazon sellers pic.twitter.com/MOWsPWxcb1

— Amazon Sellers ASGTG (@AmazonASGTG) March 7, 2024

Small Business Administration Upgrades its Business Loan Marketplace

March 5, 2024 Add the SBA to the list of organizations capitalizing on the popularity of business loan marketplaces. The Administration recently announced the next generation of its Lender Match tool.

Add the SBA to the list of organizations capitalizing on the popularity of business loan marketplaces. The Administration recently announced the next generation of its Lender Match tool.

“The enhanced Lender Match will provide Americans seeking funding to start and grow their businesses with a simple, online tool that will more effectively match them with the SBA’s competitive lending products and additional offerings from a trusted network of banks and private lenders,” the SBA said.

The updated homepage says that the tool will match applicants with competitive rates and fees while offering unique benefits like lower down payments, flexible overhead requirements, and no collateral needed for some loans.

“Borrowers will now be able to easily view all of their matched lenders in one place, allowing the borrower to find and compare lenders to help them decide where to apply for a loan. The enhanced tool will also verify borrowers and screen for fraud to streamline the process for both lenders and borrowers. Importantly, with Lender Match, small businesses that are not matched to lenders will be connected to the SBA’s local network of free advisors to help them get capital-ready.”

The SBA says that it gets 50,000 requests for capital every month through Lender Match, a platform which now has nearly 1,000 SBA lenders and 257 community-based lenders.

Matching borrowers with lenders is big business right now. In January, for example, SoFi launched its own small business loan marketplace.