Round Two of PPP Is Targeting Much Smaller Businesses

May 4, 2020 $79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

$79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

Though the pause button for big lenders was only in effect for eight hours that day, it was recognition that the playing field had not been level in the first round. JPMorgan Chase, the largest lender in round 1, for example, had an average PPP loan size of $515,304 in that round.

It’s a competitive process for limited dollars. 5,400 direct PPP lenders have already participated in the second round. More than 80% of those have less than $1 billion in assets. Senator Marco Rubio, a champion of PPP, called the latest figures released by the SBA as “all good news.”

Square Capital, meanwhile, has taken small to the extreme. Their average PPP loan approval as of April 29th was just $16,000, according to stats published by Square Capital head Jackie Reses on twitter. But only 2,711 of the 38,000+ approved had received the funds so far.

Still, that average is significantly smaller than the average loan size of $73,000 approved by Ready Capital in Round 1, a non-bank lender that got widespread attention for approving more PPP loans than any other lender in the country. Those record-breaking numbers, however, led to delays in borrowers receiving their funds to the point where as of April 30th, the responsibility of funding those loans had reportedly transferred to Customers Bank.

OnDeck has also played a role in the PPP, though only as an agent despite being approved by the SBA to lend. That news, which was revealed last week in the company’s quarterly earnings call, is likely due to the company’s current predicament brought on by government-mandated shutdowns.

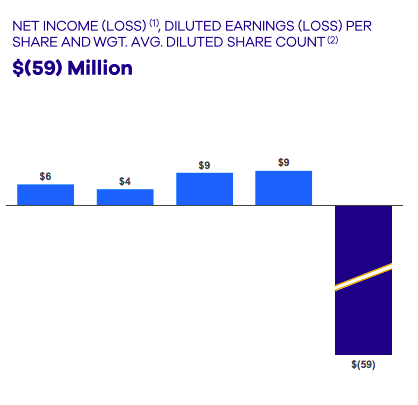

OnDeck Reports Q1 Net Loss of $59M, Suspends Non-PPP Lending Activities

April 30, 2020O nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

The company has also suspended its pursuit of a bank charter. The company has instituted a 15% pay reduction for its full-time employees, a 60% pay reduction for part-time employees, and furloughed additional employees that will receive benefits but no salary. OnDeck CEO Noah Breslow and members of the Board took a 30% pay reduction.

The company said that PPP funding has not really reached real small businesses like the ones they serve and as such only a handful of their customers have received PPP funds. While OnDeck is approved to operate as a PPP lender themselves, they have been acting as an agent of them in the interim and will dedicated their resources almost entirely to this endeavor. The company anticipates that originations of its own products could contract by 80% or more in Q2.

The company has not tripped any covenants or triggers with its own lenders as of yet but is currently in discussions with them on a path forward in this environment.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

Noah Breslow, chief executive officer, is quoted in the announcement:

“In the span of several weeks, the spread of COVID-19 led to government-mandated lockdowns for small businesses both in the US and globally, placing our customers under unprecedented economic stress.After a successful and rapid transition to remote work, we effected immediate changes to our business to preserve liquidity, support our customer base, manage our loan portfolio and reduce costs. With an uncertain timetable for the reopening of the economy, and the effectiveness of government stimulus for small businesses unclear, we will be reducing debt balances in the second quarter and focusing on managing our portfolio, delivering government stimulus to our customer base and ensuring the company has the runway to scale operations again when the economy reopens.”

The company fully utilized its initial $50 million share repurchase authorization in the first quarter of 2020. On February 10, 2020, the Board authorized the company to repurchase up to an additional $50 million of common shares, and the company has approximately $23 million of remaining capacity under that authorization. The company suspended share repurchases late February but maintains authorization to resume purchases at its sole discretion.

For 2020, OnDeck expects:

- Portfolio contraction reflecting an 80% or more reduction in second quarter origination volume

- Increased delinquency and charge-offs stemming from COVID-related economic deterioration

- Reduced Net Interest Margin reflecting a lower portfolio yield

- Reduced operating expenses, on pace to cut second quarter expenses by approximately 25%.

The company had been on a modestly positive trajectory as of year-end 2019.

The company’s stock had a somewhat minor rally on Wednesday, closing at $1.61. That’s still substantially down from where it stood on February 20th at $4.22. It hit a low of 66 cents on March 18th. The share price dropped by nearly 19% after earnings were released on Thursday morning.

This story will be updated as the information becomes available.

Ready Capital Was The Biggest PPP Lender By Volume in Round 1 of PPP Funding

April 22, 2020 Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

“As a leading non-bank, SBA lender, there’s 14 of us, we’re number two in terms of originations last year,” Capasse said on Fox Business, “we focused broadly, we don’t have deposit relationships, so we open our doors broadly to in particular the smaller mom and pop, the local deli, the pizzeria, the nail salon, so just in terms of the numbers, round one of the PPP, we approved 40,000 loans which is number one in the US, it was about $3 billion in total approvals. And our average balance was only $73,000 versus $230,000 for the average in round one.”

Among Ready Capital’s channels for acquiring PPP loan applications is Lendio, who reported consistent figures (a rough average of $80,000 per PPP loan facilitated), and high volume. Lendio has said on social media that they have been working with several partners, Ready Capital among them.

Ready Capital’s Capasse reasoned that their speed could probably be attributed to an affiliated fintech lender. “We are maybe more efficient than some of the banks because we have an affiliated fintech lender which is able to create online portals and processes to work in a more efficient manner and that enabled us to not only process these loans more efficiently but also to provide broad access to the program, to the smaller business owners.”

The company acquired Knight Capital, a small business finance provider, late last year.

Small Business Group Advocates For Community Anchor Loan Program (CAP) In Wake Of PPP Wind Down and Possible Refresh

April 17, 2020 At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

Congress is considering another round of additional PPP funding but Americans may be worrying that such funds will once again go into the hands of some of America’s largest chains. (44.5% of the $349B PPP funds went toward loans over $1 million)

Outspoken successful businessman Mark Cuban has proposed a solution, a lottery system next time around to improve the chances that smaller businesses get their share of the pie. While the public debates the merits of such an approach, one organization (the SBFA) is calling for something much more direct, a targeted fix via a Community Anchor Loan Program (CAP) that would appropriate $10 billion for businesses that were PPP-eligible for loans under $75,000 but did not receive funds.

Deployment of this capital under CAP can and should be administered by non-bank alternative lenders with proven success with this particular small business market, they say.

The proposal also calls for 25% of the funds to specifically be allocated for minority, women, and veteran-owned and agricultural businesses.

In a letter the SBFA submitted to Congress earlier this week, the organization said:

“Women and minority-owned businesses are historically smaller and employ fewer people and, in some communities, are under-banked without the established relationships required to secure a PPP loan. Small farms and agricultural businesses are important to communities and often have trouble qualifying for traditional financing.”

The Small Business Finance Association is a non-profit advocacy organization whose mission “is to take a leadership role in ensuring that small businesses have access to the capital they need to grow and thrive.”

Facebook Announces $100M Small Business Grant Program

April 13, 2020 Earlier this month Facebook announced that it will begin rolling out its small business grant program across the world to provide relief for companies affected by the coronavirus. Totaling $100 million in value, the program will provide funding to small businesses in over 30 countries via grants that are mostly cash, but will also include Facebook ad credits. The news comes one month after the tech giant launched its Business Hub.

Earlier this month Facebook announced that it will begin rolling out its small business grant program across the world to provide relief for companies affected by the coronavirus. Totaling $100 million in value, the program will provide funding to small businesses in over 30 countries via grants that are mostly cash, but will also include Facebook ad credits. The news comes one month after the tech giant launched its Business Hub.

$40 million of this will be allocated to 10,000 American small businesses. Beginning in Seattle and New York, the plan is to eventually launch the program in an additional 32 US cities.

Eligible businesses need not be active on Facebook, Instagram, or WhatsApp; however they must employ between 2 and 50 workers, have been in business for over a year, have experienced challenges due to covid-19’s impact, and be in or near a location where Facebook operates.

As well as the grant initiative, Facebook has launched a number of web resources to provide information about applying for SBA loans, how to better connect with customers at this time, and how to bring businesses more online. As well as this, it has expanded its digital services, upgrading its fundraising portal, offering digital gift cards, and enabling business pages to offer delivery and pickup.

“These are rolling out today in the US and our teams are working hard on bringing these tools to more countries, as we know they can be a lifeline for businesses to quickly get the capital they need until it is safe to open their doors again,” said Facebook COO Sheryl Sandberg in a statement. “Small businesses are the heartbeat of their communities. We are determined to help and we know the road ahead will require a lot more from all of us.”

Business can begin the application process by heading to Facebook’s site and checking whether their location will be included in the program.

Canadian Small Businesses Face Tough Challenges As Government Passes Over Fintech

April 8, 2020 This week the Canadian government announced its coronavirus economic relief plans. Among them are two initiatives that aim to assist small businesses: the Canada Emergency Response Benefit (CERB) and Canada Emergency Business Account (CEBA).

This week the Canadian government announced its coronavirus economic relief plans. Among them are two initiatives that aim to assist small businesses: the Canada Emergency Response Benefit (CERB) and Canada Emergency Business Account (CEBA).

The first of these is a wage subsidy that will cover up to 75% of a company’s payroll. The hope being that this will postpone the overcrowding and clogging of the Canadian unemployment benefits system, known as employment insurance. However this program appears to appeal to only certain types of businesses. With subcontractors not qualifying as part of payroll, there is the fear that CERB could leave many small businesses and startups that rely on freelancers unprotected. As well as this, there is a requirement that the company’s most recent month of revenue be at least 30% less than what it was at the same time the previous year. This specification again acting as an obstacle to startups and high growth businesses.

The second is a loan program that is capped at CAN$40,000 with 0% interest for the first two and a half years, and then 5% annual interest beginning January 1, 2023. There will be an opportunity for the remainder of the loan to be forgiven if the business has repaid 75% by December 31, 2022.

According to Smarter Loans’ Vlad Sherbatov, the situation in Canada mirrors what is happening in the US with regards to PPP. “There are very little details available about how people are going to apply to get the funds,” the President and Co-Founder explained. “Nobody knows what’s actually happening and nobody knows when business owners can actually anticipate to receive any funding.”

Expressing frustration that the Canadian government chose to ignore non-bank lenders in favor of allowing Canadian banks like BMO, RBC, and TD to distribute the funds, Sherbatov noted that it is the lenders who have the technology and processes to speedily disperse capital. “We did a survey that said almost 50% of business owners said they would shut down in less that four weeks without additional help … so it’s not that it’s just fine that there is help available, it’s how fast can [business owners] get the help, because every day that goes by makes the situation worse.”

Expressing frustration that the Canadian government chose to ignore non-bank lenders in favor of allowing Canadian banks like BMO, RBC, and TD to distribute the funds, Sherbatov noted that it is the lenders who have the technology and processes to speedily disperse capital. “We did a survey that said almost 50% of business owners said they would shut down in less that four weeks without additional help … so it’s not that it’s just fine that there is help available, it’s how fast can [business owners] get the help, because every day that goes by makes the situation worse.”

Speaking to Kevin Clark, President of Lendified, he echoed Sherbatov’s concern.

“It’s all good that the government is making these decisions, but the capital has to move and the programs have to be in effect. So announcing these things is one thing, actually practicing them and executing them is another. There’s a time lag that could potentially put companies out of business and so, for us, it’s about trying to connect with a lot of these borrowers to say, ‘What can we do to help you with payments?’ But at the same time, we don’t want deferments for a long period of time because then our revenue base is challenged. So the fintech lenders all have significant challenges at hand, because defaults that move from within the normal course of between 5 and 10%, say now to between 15 and 25%, or even higher, are significant challenges for the operations of our business.”

Also a member of the Canadian Lenders Association, Clark is involved in the CLA covid-19 working group that was launched in March. Formed with the intention to assist the government’s approach to capital distribution, Clark was disappointed with the government’s decision to exclude non-bank lenders after the group reached out to both the Ministry of Finance and the Business Development Corporation of Canada. And with no government funding operation to assist, Clark, like many lenders in Canada, is turning toward his existing customers, hoping to keep their heads above water.

“What we’re all doing independently is trying to work with our customers to give them guidance on what is going on in Ottawa. And so most of us have made website adjustments to give some education to interested parties on what’s available in terms of subsidy. We’re trying to provide support to our customers through deferments and so forth, just as every lending institution is doing these days. It’s just that I think it’s harder for us and smaller firms that don’t have the margin and the wherewithal to withstand any sort of significant timeline in this situation. So it’s a little bit of week by week for us, trying to manage our own costs and so forth and keep our customer bases as happy and healthy as we can.”

Can The SBA Handle The Stimulus On Their Own?

March 27, 2020 As the market cheers the upcoming passage of a $2 Trillion stimulus bill that is intended to provide much needed support to small businesses, industry insiders are beginning to raise concerns about the SBA’s infrastructural ability to process applications in a timely manner.

As the market cheers the upcoming passage of a $2 Trillion stimulus bill that is intended to provide much needed support to small businesses, industry insiders are beginning to raise concerns about the SBA’s infrastructural ability to process applications in a timely manner.

In a webinar hosted by LendIt Fintech yesterday, Opportunity Fund CEO Luz Urrutia estimated that conservatively, it could take the SBA up to two months to even begin disbursing loans offered by the bill. Kabbage President Kathryn Petralia offered the most optimistic estimate of 10 days, while Lendio CEO Brock Blake thinks that perhaps it could take around 3 weeks.

Blake followed up the webinar by sharing a post on LinkedIn that said that small businesses were reporting that the SBA’s website was so slow, so riddled with crashes, that the SBA had to temporarily take their site offline.

Most skeptics raising alarms are not referring to the SBA’s staff as being unprepared, but rather the systems the SBA has in place.

A March 25th tweet by the SBA reported that the site was undergoing “scheduled” improvements and maintenance.

The website is currently undergoing continued scheduled improvements and maintenance. For more info on SBA #COVID19 resources, visit https://t.co/yG2N17KF63

— SBA (@SBAgov) March 25, 2020

This all while the demand for capital is surging. Blake reported in the webinar that loan applications had just recently increased by 5x at the same time that around 50% of non-bank lenders they work with have suspended lending.

Some informal surveying by AltFinanceDaily of non-bank small business finance companies is finding that among many that still claim to be operating, origination volumes have dropped by more than 80% in recent weeks, mainly driven by stay-at-home and essential-business-only orders issued by state governments.

It’s a circular loop that puts further pressure on the SBA to come through, none of which is made easier by the manual application process they’re advising eager borrowers to take on. The SBA’s website asks that borrowers seeking Economic Injury Disaster Loan Assistance download an application to fill out by hand, upload that into their system and then await further instructions from an SBA officer about additional documentation they should physically mail in.

Perhaps there’s another way, according to letters sent to members of Congress by online lenders. 22 Fintech companies recently made the case that they are equipped to advance the capital provided for in the stimulus bill.

“We seek no gain from this crisis. Our only aim is to protect the millions of small businesses that we are proud to call our customers,” the letter states.

Members of the Small Business Finance Association made a similar appeal in a letter dated March 18th to SBA Administrator Jovita Carranza. “In this time of need, we want to leverage the experience and expertise we have with our companies to help provide efficient funding to those impacted in this tough economic climate. We want to serve as a resource to governments as they build up underwriting models to ensure emergency funding will be the most impactful.”

How fast things come together next will be key. The House is scheduled to vote on the Senate Bill today. If a plan to distribute the capital cannot be expedited and the crisis drags on, the consequences could be dire.

“Hundreds of thousands of businesses are going to be out of business,” Urrutia warned in the webinar.

$2 Trillion Senate Relief Bill to Pass Vote, Includes Small Business Funds

March 26, 2020 Senate leaders Mitch McConnell and Chuck Schumer have come to an agreement over a stimulus package that would inject $2 trillion into the US economy. With senators debating the bill at the time of writing, it is expected to pass. Said to be the largest and most robust rescue package in American history, the bill would see $300 billion go to the SBA for its 7A loan program.

Senate leaders Mitch McConnell and Chuck Schumer have come to an agreement over a stimulus package that would inject $2 trillion into the US economy. With senators debating the bill at the time of writing, it is expected to pass. Said to be the largest and most robust rescue package in American history, the bill would see $300 billion go to the SBA for its 7A loan program.

“At last we have a deal,” McConnell said after negotiations wrapped up at 1:30am on Wednesday morning. McConnell later described the bill as “a war-time level of investment into our nation.”

According to Stephen Denis, Executive Director of the SBFA, who was closely engaged with the language being placed into the bill, certain small businesses who receive SBA loans may have their loan converted to a grant, depending upon how they aim to spend the financing. As well as this, Denis made clear that small businesses will be able to use these funds to pay any charges linked to an online small business loan or MCA.

“There’s different things that you can use the SBA money for,” Denis explained in a call. “Payroll support, obviously, including paid sick leave, medical, or family leave; costs related to health care; employees salaries; mortgage payments; rent payments; utilities. And then this is another thing that we got inserted into the bill, we wanted to make sure that businesses had the flexibility to use this funding to pay existing debt obligations that were incurred before the covered period. What this means is that if a business had taken out an MCA or a loan, that they could use this money to pay off the obligations.”

As well as allotting funds for the SBA, the bill provides for cash payments of up to $1,200 to be made available directly to individuals, $2,400 for married couples, and an additional $500 per child, which will be reduced if the individual makes more than $75,000 annually or if the couple makes over $150,000. $350 billion will also be made available to help small businesses mitigate layoffs and support payroll.

The most recent example of something akin to this bill is the Troubled Asset Relief Program (TARP) that was established to help financial institutions in the aftermath of the ’08 financial crisis. And with there being some surprise in retrospect to how TARP’s funds were ultimately used, there is concern about supervision of these funds.

When asked on Monday who would provide oversight for the program to fund businesses, President Trump replied with, “I’ll be the oversight.” However, since then White House officials have agreed in closed-door negotiations that an independent inspector general as well as an oversight committee will be instated to supervise the loans.

Despite stalling in the Senate several times throughout Wednesday, Denis is confident that the bill will be voted through the Senate, and following this, through the House.

“Never make a guarantee in Washington. That’s something I’ve learned in my career. But I think this is something that both sides, both Democrats and Republicans, recognize needs to get done right now. And I can’t imagine anymore political games after the agreement this morning.”

As well as this, Denis was eager to highlight that many funders and broker shops fall under the classification of a small business, and would be eligible for some of the funds promised by this $2 trillion bill; and that if you are wondering how you might access some of the relief package upon its passing through government, to reach out to him.