Participate in Alternative Finance? You Might Want to Start Watching the Supreme Court

August 19, 2015 A trio of cases before the Supreme Court could have far reaching effects on alternative small business finance. Here’s a rundown of what to watch.

A trio of cases before the Supreme Court could have far reaching effects on alternative small business finance. Here’s a rundown of what to watch.

1. Texas Department of Housing and Community Affairs v. The Inclusive Communities Project, Inc. (Decided June 25, 2015)

In this case, the Court was asked to decide whether a disparate impact claim—a legal theory that allows regulators to bring discrimination claims against a defendant even where no intentional discrimination is alleged—could be brought under the Fair Housing Act. Many observers hoped the Court would find that such claims could not be brought under the FHA and nearby limit their use under other federal statutes such as the Equal Credit Opportunity Act. The Court, however, found that disparate impact claims could be brought under the FHA.

How does this affect alternative lenders?

The Dodd-Frank Act gave the CFPB authority to enforce ECOA, which is one of the few fair lending laws that apply to small business lenders. Some legal observers believe that the CFPB could potentially bring disparate impact claims under ECOA against alternative funders that the Bureau believes have engaged in policies that have resulted in discrimination. The Court’s decision may embolden the agency to bring future actions.

2. Hawkins v. Community Bank of Raymore (To be argued October 5, 2015)

ECOA prohibits lenders from discriminating against applicants on the basis of race, color, religion, national origin, sex, marital status, or age. It also requires lenders to provide applicants notice of any adverse actions taken by the lender in relation to the applicants’ request for credit. The Hawkins case asks the Court to decide whether guarantors should be included in the definition of applicant.

How does this affect alternative lenders?

If the Court determines that personal guarantors are included in the definition of applicant, guarantors would be entitled to the same protections and disclosures as business applicants. Lenders would be required to provide the primary business applicant as well as each guarantor with the appropriate adverse action notices in the event of a decline. Implementing procedures to comply with this requirement could require significant investment from alternative lender.

3. Madden v. Midland Funding, LLC (Appeal expected soon)

This case has been widely followed given its potential effects on marketplace lenders that use banks to originate their loans. The Madden court held that the usury preemption provision of the National Bank Act did not apply to non-bank assignees. Midland requested that the 2nd Circuit rehear the case en banc but that request was denied last week. Midland now has 90 days from the date of the denial to petition the Supreme Court to review the 2nd Circuit’s decision.

How does this affect alternative lenders?

As it stands now, Madden is binding in the 2nd Circuit. If the Supreme Court declines to hear the case, the denial will confirm that Madden is settled law. In that event, observers will be closely watching to see what effect Madden has on litigation involving marketplace lending as well as the purchase and sale of bank originated debt in the larger secondary markets. A recent case out of California may provide some early indications.

Madden vs. Midland Funding, LLC: What does it mean for Alternative Small Business Lending?

August 13, 2015 On Friday, May 22, 2015, while the rest of us were gearing up for the long Memorial Day weekend, three judges of the United States Court of Appeals for the Second Circuit quietly issued their decision in Madden v. Midland Funding, LLC. Though issued to little fanfare, the decision, if upheld on appeal—may lead to significant changes in consumer and commercial lending by non-bank entities.

On Friday, May 22, 2015, while the rest of us were gearing up for the long Memorial Day weekend, three judges of the United States Court of Appeals for the Second Circuit quietly issued their decision in Madden v. Midland Funding, LLC. Though issued to little fanfare, the decision, if upheld on appeal—may lead to significant changes in consumer and commercial lending by non-bank entities.

Loans that were previously only subject to the usury laws of a single state may now be subject to more restrictive usury laws of multiple jurisdictions. Commercial transactions that could be affected include short-term loans by a number of alternative small business lenders.

The Case

The plaintiff, Saliha Madden, opened a credit card account with a national bank in 2005. Three years later, Madden’s account was charged off with an outstanding balance. The account was later sold to Midland Funding, LLC, a debt purchaser.

In November 2010, Midland sent a collection letter to Madden’s New York residence informing her that interest was still accruing on her account at the rate of 27% per year. In response, Madden filed a class action lawsuit against Midland and its servicer. In her complaint, Madden alleged that Midland had violated state and federal laws by attempting to collect a rate of interest that exceeded the maximum rate set by New York State’s usury laws. Midland countered that as a national bank assignee, it was entitled to the preemption of state usury laws granted to national banks by the National Bank Act (the “NBA”). The district court agreed with Midland and entered judgment in its favor. Madden appealed to the Second Circuit.

After reviewing the record, the Court of Appeals reversed the district court’s decision. The appellate court found that the NBA’s preemption provision did not apply to Midland as a mere bank assignee. Instead, the court held that in order “[t]o apply NBA preemption to an action taken by a non-national bank entity, application of state law to that action must significantly interfere with a national bank’s ability to exercise its power under the NBA.”

The court explained that the NBA’s preemption protections only apply to non-bank entities performing tasks on a bank’s behalf (e.g. bank subsidiaries, third-party tax preparers). If a bank assignee is not performing a task on a national bank’s behalf, the NBA does not protect the assignee from otherwise applicable state usury laws. Therefore, as Midland’s collection efforts were performed on its own behalf and not on behalf of the national bank that originated Madden’s account, the appellate court found that New York’s usury laws were not preempted and that Midland could be subject to New York’s usury restrictions.

Usury Law Compliance

The Madden decision undermines a method of state usury law compliance that I’ll refer to as the “exportation model”. In a typical exportation arrangement, a non-bank lender contracts with a national bank to originate loans that the lender has previously underwritten and approved. After a deal has been funded, the bank sells the loan back to the lender for the principal amount of the loan, plus a fee for originating the deal.

1F.3d —, 2015 U.S. App. LEXIS 8483 (2d Cir. N.Y. May 22, 2015).

The exportation model allows non-bank lenders to benefit from the preemption protections granted to banks under the NBA. Specifically, the NBA provides that a national bank is only subject to the laws of its home state. This provision allows a bank to ‘export’ the generally less restrictive usury laws of its home state to other states where it does business. As bank assignees, lenders that have purchased loans from a bank are only subject to the laws of the originating bank’s home state. This exemption saves these non-bank lenders from having to engage in a state-by-state analysis of applicable usury laws.

The Madden decision, however, casts doubt on the ability of these non-bank assignees to benefit from the NBA’s preemption protections. The Second Circuit’s decision makes clear that non-bank assignees that are not performing essential acts on a bank’s behalf—which would seem to include alternative small business lenders—are not entitled to NBA preemption and are subject to the usury laws of the bank’s home state as well as any otherwise applicable state’s

usury laws.

Aftermath

While the Court of Appeals’ decision foreclosed Midland’s preemption argument, other issues remained unresolved. Specifically, the circuit court did not decide whether the choice-of-law provision in Madden’s cardholder agreement—which provided that any disputes relating to the agreement would be governed by the laws of Delaware—would prevent Madden from alleging violations of New York State usury law.

In the district court proceeding, both parties had agreed that if Delaware law was found to apply, the 27% interest rate would be permissible under that state’s usury laws. The district court, however, did not address the choice-of-law issue because the court had found that the NBA’s preemption protections were sufficient grounds upon which to resolve the case. As the issue had not been addressed, the circuit court remanded the case back to the district court to decide which state’s law controlled.

In the district court proceeding, both parties had agreed that if Delaware law was found to apply, the 27% interest rate would be permissible under that state’s usury laws. The district court, however, did not address the choice-of-law issue because the court had found that the NBA’s preemption protections were sufficient grounds upon which to resolve the case. As the issue had not been addressed, the circuit court remanded the case back to the district court to decide which state’s law controlled.

But before sending the case back down, the appellate court made two points worth noting. First, the court stated that “[w]e express no opinion as to whether Delaware law, which permits a ‘bank’ to charge any interest rate allowable by contract…would apply to the defendants, both of which are non-bank entities.” The court’s statement suggests that it may not have completely agreed with the parties that 27% would be a permissible interest rate under Delaware law.

Second, the court highlighted a split in New York case law on the enforceability of choice-of-law provisions where claims of usury are involved. Generally, courts will refuse to enforce a choice-of-law provision if the application of the chosen state’s law would violate a public policy of the forum state. As usury is sometimes considered an issue of public policy, the enforceability of such clauses is commonly a point of contention in usury actions. The cases cited by the Court of Appeals show that some courts in New York have enforced choice-of-law provisions—even where the interest rate permitted by the chosen state would violate New York’s usury laws—while other New York courts have refused to enforce such provisions in light of public policy concerns.

New York, however, is by no means the only state with usury laws that are less than straightforward. The general complexity of state usury laws is evidenced by the circuit court’s hesitation to agree with Madden’s concession that a 27% interest rate would be permissible under Delaware law. The court made clear that an argument could be made that the rate was usurious under both New York and Delaware law.

Madden’s Impact

An important legal principle that was not addressed in either the district or circuit court proceedings is the ‘valid when made’ doctrine of assignment law. The ‘valid when made’ doctrine provides that a loan that is valid at the time it is made will remain valid even if the loan is subsequently assigned. This doctrine may have led to a different outcome in the case had Midland argued it before the district or circuit court. Midland is now appealing the Second Circuit’s decisions and many expect a ‘valid when made’ argument to be a primary point of Midland’s appeal (SEE NOTE BELOW). If this argument is successful, the practical impact of Madden would be greatly diminished.

NOTE: The Second District Court rejected a request to rehear the case. Read that decision here.

In the meantime, the Madden decision will likely increase the importance of choice-of-law analysis in relation to usury law. Assignees that previously relied on the NBA’s preemption provision as a method of state usury law compliance will now need to address the enforceability of their contractual choice-of-law clauses where claims of usury may become an issue. This analysis is often a complex undertaking because states take varying views of what constitutes usury as well as whether or not usury is an issue of public policy.

While the Madden decision may have been published before the long Memorial Day weekend, analyzing its consequences will likely keep many non-bank lenders (and their attorneys) busy, even on their days off.

New Funding Brokers Struggle As Industry Grows

August 3, 2015 Here’s a few things that will have you scratching your head.

Here’s a few things that will have you scratching your head.

1. A new sales agent recently took to an industry forum to ask for help with ACH processing. According to him, he charged a closing fee on a loan that closed and then realized that he had no idea how to collect the fee. His problem was perplexing because he had the merchant sign an agreement that authorized him to debit the funds out despite not having an ACH processing account.

Some sympathetic veterans advised him to have the merchant write him a check, but others were too dumbfounded by his use of an ACH agreement when he did not know anything about ACH. The agreed fee was probably too large to write off as a mistake so hopefully the merchant will understand and write him a check for services rendered.

The lesson: If you don’t know how to do something, don’t guess. The agent would’ve been in a much better situation if he had asked how to collect fees prior to drawing up an agreement that referred to a methodology he had no familiarity with.

2. A semi-seasoned sales agent griped about a recent experience on an online message board about a business lender that stole his deals and turned out to be a repeat felon. The broker community was not sympathetic when they learned that the “lender” used a gmail address to communicate. What’s worse is that a perfunctory Google search revealed a record of violent crime.

The lesson: At the very least, do not send deals to anyone using a free email address. This was item #3 on my Advice to New Brokers list, published back in February. This also violated item #4 on my list, which says, don’t send your deal to some random company just because they went around posting on the web. A simple Google search for this broker would’ve showed that the “lender” was a serial criminal.

3. One broker e-mailed me to say that a lender had stolen his syndication money and disappeared. Another told me that they had stopped receiving their syndication deposits for their entire portfolio and wasn’t sure what was going on. This situation often doesn’t make the public forums because the aggrieved parties are sometimes too embarrassed to tell others that they got hustled. I recommended a lawyer to one of them.

The lesson: Refer to #4 on my Advice to New Brokers list. Even if others claim to be having a positive experience, there are a few red flags to look out for when it comes to syndication:

- Were they too eager to accept your money?

- Did they have an Anti-Money Laundering process in place?

- Would your funds be co-mingled with their operating funds or isolated in a separate account?

- How is their system structured? Will you get paid even if they declare bankruptcy?

- Was the owner of the company ever charged or convicted with fraud? This is probably the most important and for some reason the most overlooked. If the owner was previously charged with fraud and your money eventually gets stolen, you can only blame yourself. And if you don’t know if someone has a past criminal history, you should probably ask around in addition to conducting a formal background check.

Syndicating brings me to item #1 on my Advice list, hire a lawyer. If you can’t afford a lawyer, you definitely can’t afford to syndicate.

Strategic Funding Source Increases Borrowing Capacity to $90 Million with New Revolving Credit Facility Led by CapitalSource

July 15, 2015 Strategic Funding Source, Inc., a leading provider of direct financing to small and midsize businesses, today announced that it has closed on a $90 million revolving credit facility. Led by CapitalSource, a division of Pacific Western Bank, the loan agreement includes continued participation from East West Bank and the addition of BankUnited to the lending group.

Strategic Funding Source, Inc., a leading provider of direct financing to small and midsize businesses, today announced that it has closed on a $90 million revolving credit facility. Led by CapitalSource, a division of Pacific Western Bank, the loan agreement includes continued participation from East West Bank and the addition of BankUnited to the lending group.

“Gaining access to the capital needed to grow continues to be an issue for many of America’s hard working small business owners and our industry plays a crucial role in addressing that need,” said Andrew Reiser, Chairman and Chief Executive Officer, Strategic Funding Source. “With the support of our outstanding bank partners we have now more than doubled our borrowing capacity. Coupled with the $110 million line of equity financing we secured from Pine Brook in August 2014, we are poised to significantly expand our footprint in the robust and evolving small business lending space.”

Strategic Funding Source provides loans and cash advances to small businesses by combining advanced technology and insight based on years of experience as small business owners and financial industry experts. The company works directly with small business owners to identify their capital requirements and creates flexible, tailored financing options that suit their individual business models.

About Strategic Funding Source, Inc.

Strategic Funding Source finances the future of small businesses utilizing advanced technology and human insight. Established in 2006, the Company is headquartered in New York City and maintains regional offices in Virginia, Washington state, and Florida. Strategic Funding Source has served thousands of small business clients across the U.S. and Australia. Visit www.sfscapital.com to learn more about the Company, its financing products and partnership opportunities.

A Decade of Funding

July 7, 2015Next month is my 9 year anniversary in the merchant cash advance industry, which means I’ll be starting my 10th year. A decade of merchant cash advance… holy shit. I’ve had the opportunity to view it from many different angles and have accrued my fair share of adventures, plenty of which I’ve written about and others I’ll have to take to my grave.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

Looking back now, there weren’t many people keeping a live diary of events as the industry dove headfirst into the financial crisis. Who would’ve bothered to report on an industry that was arguably made up of only a thousand people?

In April 2009, even before AltFinanceDaily launched, I submitted a story to the only merchant cash advance magazine of its kind. It didn’t have a very clever name, just Merchant Cash Advance Publication. My story, titled, An Underwriter in Salesman’s Clothing, rambled on about the end of the industry’s glory days, the wave of declined deals in the recession, and how funders should be more appreciative of ISOs.

Here’s a summary of what I wrote more than six years ago:

Here’s a summary of what I wrote more than six years ago:

I was complaining about stacking as far back as 2007 apparently. I addressed it as a merchant problem. Merchants were taking advantage of funders, not the other way around like some frame the argument in 2015.

I left my post as Director of Underwriting in late 2008 because “I wanted the ringing phones, the commotion, the markerboards with stats, the glory, the $20,000 [monthly] checks.”

Funding companies became super conservative during the financial crisis and all my deals were being killed (25 deals declined in a row at one point.)

I had recently charged my first closing fee, felt bad about it, and got in trouble for it.

I said 1.40 factor rates wouldn’t last (I was wrong about this!)

I bitched about algorithmic declines (I apparently thought computers underwriting files was a good way to upset ISOs.)

I acknowledged my own hypocrisy when I realized how hard it was to be a sales rep after thinking sales reps were overpaid and overrated in my previous years as an underwriter.

I continued on as a sales rep for another two and a half years after I wrote that. That means that in 2010 when I started AltFinanceDaily, I was still calling UCCs, closing deals and boarding merchant accounts while sitting in a windowless room rented by a startup ISO.

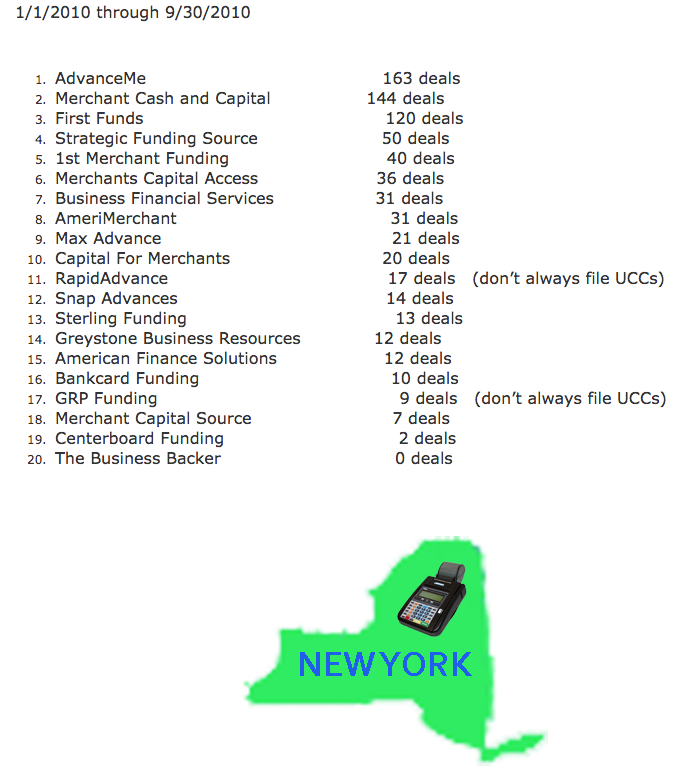

But what was there to blog about in 2010? Oh little stuff like who the biggest funding companies were at the time by checking UCC filings since almost everyone filed UCCs back then. Notably, the third largest merchant cash advance company of 2010, First Funds, is no longer in business.

I also wrote about shopping deals around and the impact that might have on a merchant’s credit report. That was the day-to-day stuff though, information I was just putting out there hoping someone on the Internet might see it. What got everyone excited was the 2010 New York State leaderboard which eventually prompted me to spend my nights and weekends investigating the industry on a wider level.

I began talking to people at other funding companies about their monthly numbers. It wasn’t that hard to get information as an industry insider, especially if you had deals to send somebody’s way. I also spent money to acquire secured party lists to count the number of UCC filings by funders in all 50 states rather than just look at one free state like I did with New York originally. I think I was the only person in the industry at the time running up their personal credit card bill to conduct such research. I had also been in the industry for four years at that point and had a great network of contacts who could clue me in on their volume.

While I said that I also looked at census records and department of labor records, I’ll admit that data wasn’t extremely useful. The end result was a best guess estimate that in 2010, there were approximately 21,000 merchant cash advances transacted for $524 million.

My data would go on to be republished in ISO&Agent Magazine, The Scotsman Guide, and Leasing News, and also end up in many other places I didn’t expect, like in the business plans of merchant cash advance companies that were looking to raise capital. In fact, in a private meeting I had with an MCA company months later in South Florida, the CEO let me take a peek at the docs they had just submitted to a bank for a credit facility. Included was a printout of these numbers with my name on it and all. Apparently there was something to this writing thing…

My last day as a sales rep was in the Fall of 2011. I left the commission-only life (oh what, you 2015 pansy closers actually get a base salary?) for something even more risky, an entrepreneurial life. For a couple years, I played underwriting consultant to a handful of merchant cash advance companies and industry expert to institutional investors interested in the space. I learned how to code in my spare time and spent more than a year in online lead generation.

I never stopped writing.

Along the way I’ve visited the offices of dozens of ISOs and funders, syndicated in deals, and test-drove new technology.

None of this makes me particularly special, especially when I hear about how much some of my old sales buddies are making these days on deals. “Are you SURE you don’t want to come back?” they ask. It’s enticing no doubt. A part of me wants to grab the phone out of their hand and attempt to shatter their record on the markerboard this month even though I’m pretty sure I’m rusty as hell.

One thing noticeable between now and 9-years ago is that my hair turned grey. This industry will do that to you (or at least it did to me.) And I still get a kick out of meeting folks who got into the industry years before I did. The 90s/early 2000s AdvanceMe crowd likes to tell me that they were funding merchants while I was still in diapers. They are practically right.

As I enter my own tenth year in the biz however, it’s exciting to think that the industry is just now getting started. OnDeck was the first IPO in the space and the general public is learning about short term business funding for the first time. There’s no shortage of news to report and that keeps me plenty busy these days.

And so even after a decade of MCA, it’s never too late to put on your Funded pants. Opportunity awaits and I hope you’ll continue to ride the wave with me. Thanks for reading since 2010!

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after AltFinanceDaily sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on AltFinanceDaily’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as AltFinanceDaily’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Legal Brief: Madden v. Midland Funding

June 11, 2015Madden v. Midland Funding, 2015 U.S. App. LEXIS 8483 (2nd Cir. May 22, 2015).

This is an interesting case for the alternative lending industry that deals with the interplay between the National Banking Act and New York State’s usury laws.

This is an interesting case for the alternative lending industry that deals with the interplay between the National Banking Act and New York State’s usury laws.

The plaintiff borrower opened a credit card account with a national bank, Bank of America (“BoA”). BoA sold the account to another national bank, FIA. FIA subsequently sent a change of terms notice stating that, going forward, the plaintiff’s account agreement would be governed by the law of Delaware, FIA’s home state. FIA later charged off the account and sold it to a third-party debt purchasing company, Midland. FIA did not retain any interest in the account after selling it to Midland and Midland was not a national bank.

Midland attempted to collect on the account and sent the plaintiff a demand letter indicating that there was a 27% interest rate on the account. Plaintiff sued Midland, alleging violations of the Fair Debt Collection Practices Act and New York’s criminal usury laws. New York law limits effective interest rates to 25 percent per year. The parties agreed that FIA had assigned plaintiff’s account to Midland and that the plaintiff had received FIA’s change in terms notice. Based on the agreement, the trial court held that the plaintiff’s state law usury claims were invalid because they were preempted by the National Bank Act.

The National Bank Act supersedes all state usury laws and allows national banks to charge interest at the rate allowed by the law of the bank’s home state. Midland argued that, as FIA’s assignee, it was permitted to charge the plaintiff interest at a rate permitted under Delaware law. FIA was incorporated in Delaware and Delaware permits interest rates that would be usurious under New York law.

On appeal, The Second Circuit Court of Appeals noted that some non-national banks, such as subsidiaries and agents of national banks, might enjoy the same usury-protection benefit as a national bank. However, third-party debt buyers, such as Midland, are not subsidiaries or agents of national banks. Midland was not acting for BoA or FIA when it attempted to collect from the plaintiff. Midland was acting for itself as the sole owner of the debt. For this reason, the Second Circuit held that Midland could not rely upon National Bank Act preemption of New York State’s usury laws.

STRATEGIC FUNDING SOURCE NAMES ALAN NUSSBAUM VICE PRESIDENT OF BUSINESS DEVELOPMENT

April 20, 2015NEW YORK (April 20, 2015) – Strategic Funding Source, Inc., a leading provider of small business financing, today announced that Alan Nussbaum has joined the company as Vice President of Business Development.

In his role, Nussbaum will be responsible for developing untapped affinity relationships and other industry opportunities including the opening of new channels in emerging markets, which seek access to capital. He will report to David Sederholt, the Chief Operating Officer of Strategic Funding Source and will be based at the company’s New York City headquarters.

Nussbaum is one of the early entrants to the small business alternative financing industry and spent over 16 years leading sales initiatives with CAN Capital, the largest company in the industry. During his tenure at CAN Capital, he contributed to the growth of the company by developing diverse sales channels and will now bring his years of experience to Strategic Funding Source. As with several executives of Strategic Funding Source, Nussbaum started his career as the owner operator of small businesses, which included restaurants and a food service supply company.

“We’re pleased to welcome Alan to the management team at Strategic Funding Source,” said Sederholt. “I have known him for over 20 years as a respected member of the industry and look forward to him contributing his vast experience and insights to our company.”

“Over the course of my career, I have seen alternative finance products evolve into the mainstream direct solution for small businesses,” said Nussbaum. “I’m excited to join Strategic Funding Source, which has never forgotten the importance of people in their relationships. The company has a proven record as a leader and innovator that combines technology with a human touch. I look forward to helping both Strategic Funding Source and the small businesses we serve continue to grow.”

Nussbaum is a graduate of Pratt Institute in Brooklyn, N.Y.

About Strategic Funding Source, Inc.

Strategic Funding Source finances the future of small businesses utilizing advanced technology and human insight. Established in 2006, the company is headquartered in New York City and maintains regional offices in Virginia, Washington state, and Florida. The company has served thousands of small business clients across the U.S. and Australia, having financed over $800MM since inception. Visit www.sfscapital.com to learn more about Strategic Funding Source, its financing products and partnership opportunities.