Commission Chargebacks: The Good, the Bad and the Ugly

August 10, 2015 Imagine you’re a 20-something-year-old broker who’s just, in good faith, referred a merchant to a funder. You walk away with a few thousand dollars in your pocket, and you promptly spend it on rent and a celebratory steak dinner. Then all of a sudden…BAM! Just like that the merchant goes belly up and the funder’s knocking on your door to clawback your hard-earned commission money, which, of course, you’ve already spent.

Imagine you’re a 20-something-year-old broker who’s just, in good faith, referred a merchant to a funder. You walk away with a few thousand dollars in your pocket, and you promptly spend it on rent and a celebratory steak dinner. Then all of a sudden…BAM! Just like that the merchant goes belly up and the funder’s knocking on your door to clawback your hard-earned commission money, which, of course, you’ve already spent.

For many brokers, it’s a familiar-sounding story—with an ending they’d like to rewrite. Their thinking goes like this: underwriters, not brokers, are the ones who are supposed to dig into a company’s finances before approving a deal. Underwriters, not brokers, are the ones who make the financial decisions about whether or not a deal can go forward. Therefore, underwriters, not brokers, should be responsible when deals implode.

“There are a lot of people who think there should not be commission clawbacks—that they’re unfair,” says Archie Bengzon, who runs the New York sales office for Miami-based Rapid Capital Funding, a direct funder. Bengzon was previously the president of Merchant Cash Network, an ISO in New York.

While there’s a fair amount of closed-door grousing by brokers, most funders are standing their ground—with only a select few companies kicking these controversial policies to the curb. More commonly, funders claim clawbacks, despite being hated by brokers, are a necessary evil. These funders say that without them, they’d stand to lose too much on bad deals and that they need a way to protect themselves from rogue brokers.

“There is a group of people out there who are trying to game the system,” says industry attorney Paul Rianda, who heads a law firm in Irvine, California.

The Case for Scrapping Clawbacks

Brokers in favor of changing the status quo understand the need to prevent bad apples from smelling up the entire industry. But even so they believe that chargebacks are patently unfair to the honest majority of brokers who often make just enough to scrape by. In most cases, the brokers are typically young—18-to-26-year-olds trying to make money and learn the industry. They don’t have the financial resources that the funders do and the onus shouldn’t be on them if the deal they brought in—with good intentions—goes bust in a short time, according to the owner of a top-tier ISO/Hybrid in Staten Island, New York, who requested his name not be used.

This is especially true in cases where the underwriter took risks they shouldn’t have or decided to fund merchants in cases where they shouldn’t have. “It’s the underwriter’s job to protect the money that their company is lending out,” he says. “[Chargebacks] shouldn’t be going on in this industry.”

One solution might be for more ISOs to stand up to funders and refuse to send them future deals. That’s exactly what the Staten Island executive did a few years ago when a funder he repeatedly worked with tried to claw back his commission on a particular deal. He made a big stink and told them he’d never send them business again. It was enough of a threat to convince the funder to back off. “If more ISOs start saying that…then the funders will start sweating and change their contracts. Because it really isn’t fair,” he says.

For some brokers, however, taking such a strong position with funders is a risky strategy in a cottage industry where all the major players know each other and there’s no shortage of hungry young brokers willing to do business. So while these brokers don’t like losing money, they aren’t necessarily loudly crying foul either.

Matthew Ross, managing member of Go Ahead Funding, a broker and funder in Basalt, Colorado, has been in the business for nine years. He’s only had one commission clawed back once in this time period—it was a commission for $1,500 on a $25,000 deal that went sour within a month, he recalls. He was upset at the time and felt the underwriter should have done more to vet the merchant who went belly up. “Why didn’t the underwriters catch this?” he remembers asking at the time.

Matthew Ross, managing member of Go Ahead Funding, a broker and funder in Basalt, Colorado, has been in the business for nine years. He’s only had one commission clawed back once in this time period—it was a commission for $1,500 on a $25,000 deal that went sour within a month, he recalls. He was upset at the time and felt the underwriter should have done more to vet the merchant who went belly up. “Why didn’t the underwriters catch this?” he remembers asking at the time.

Nonetheless, Ross was a lot calmer than some brokers might have been under the circumstances. For instance, he says he never threatened to stop sending the funder business as many brokers might have done. “I don’t necessary like it, but I understand it. I’m not going to fight it,” he says.

Some brokers are making their displeasure with the practice known by declining to sign contracts that contain clawback clauses. Nathan Abadi, founder and president of Excel Capital Management, a New York-based funder and ISO, says he either refuses to do business outright or he comes to a verbal agreement with a funder that he’ll wait two weeks for payment to make sure the deal has legs. “I meet them in the middle,” he says.

The reason he likes this approach is that it’s more palpable for brokers to lose paper commissions versus actual money that they’ve already been given and possibly spent. Otherwise, as a business owner working with numerous agents, it’s bad for business. “It causes an internal conflict because now you have to penalize the person who’s working for you,” Abadi says.

The Flip Side of the Chargeback Coin

Meanwhile, there’s a whole other camp within alternative funding—including some brokers—who feel chargebacks are important as a fraud-deterrent. Given the fact that the industry is still largely unregulated, many believe that funders need some type of fire retardant to prevent being burned by unscrupulous brokers.

“We think that they serve an important role,” says Stephen Sheinbaum, founder of Merchant Cash and Capital, a New York-based funder. “Most of our stronger referral partners do not object to it. It’s a way of aligning our interests with the sales force.”

About 60 percent of the company’s funding business comes from third-parties including ISOs; its direct sales force accounts for the other 40 percent.

Even some brokers concede that clawbacks can serve a valuable purpose. Sure, it’s aggravating to lose money, but they feel that without clawbacks the industry would be even more of a free-for-all than it already is.

“I can see both sides,” says Bengzon, the funder and broker. Wearing his broker hat, Bengzon has felt the sting of losing a commission once or twice in the 100 or so deals he’s done. But he still understands why funders—who take a big monetary hit when deals go sour—would want to protect themselves and require brokers to have some skin in the game.

“If we’re going to reap the rewards of a nice commission, we should also understand that it can still be taken away if a deal goes bad,” he says.

When he sends leads to funders, Ross of Go Ahead Funding says he does his best to make sure he’s sending only high quality merchants. He tries to vet them upfront—to the limited extent he can—in order to avoid problems later on. Clawback provisions serve as “an incentive for [brokers] to keep their eyes open,” he says.

Know What You’re Signing

About 80 percent of the agreements that come across the desk of Rianda, the industry attorney, have a 30-day clawback provision. But he’s seen some agreements that have longer time frames—60, 90 or even 120 days. Those types of contracts aren’t as common, but they’re out there.

It’s important for brokers to carefully read the fine print of a contract before signing on the dotted line. “It sounds obvious, but a lot of people don’t do that,” says Bengzon.

The shorter the clawback time frame, the less brokers tend to balk. “People don’t want to be paid on a deal and three months later they lose that commission, which they’ve already spent,” he says.

Bengzon believes a clawback that extends any more than a month is excessive. “I would never sign something greater than 30 days,” he says.

According to Sheinbaum of Merchant Cash and Capital, 30 days is an appropriate time frame to help weed out fraud without putting unnecessary burden on brokers who are sending legitimate business. “The purpose of the provision is to try and stop people from committing fraud at the outset,” he says.

According to Sheinbaum of Merchant Cash and Capital, 30 days is an appropriate time frame to help weed out fraud without putting unnecessary burden on brokers who are sending legitimate business. “The purpose of the provision is to try and stop people from committing fraud at the outset,” he says.

David Sederholt, executive vice president and chief operating officer at Strategic Funding Source Inc. in New York, says clawback provisions in the contracts Strategic uses range from 30 to 45 days depending on the contract. He says he understands brokers don’t like them, but that it’s nonetheless important to have the provision in order to protect the funders. “There’s got to be some partnership involved here,” he says.

Clawbacks Not A Free-For-All

Many funders recognize that there’s a fine line between protecting their business and cutting off potential revenue sources.

“You start clawing back commissions on every default, a broker will stop sending business,” says Ross of Go Ahead Funding.

Sheinbaum of Merchant Cash and Capital notes that clawbacks aren’t used as often as some brokers might think. He says out of 800 deals in a 30- or 31-day period, his company enforces its clawback policy only a handful of times each month.

He also points out that while the clawback policy is on the books, Merchant Cash and Capital looks at each situation individually. If it’s clear that the broker tried to defraud the funder, that’s one thing, he says. But, if for instance, a merchant has a heart attack and dies 20 days into a deal and can’t pay back the funds, Merchant Cash and Capital wouldn’t try to clawback the broker’s commission in that situation, he says.

Strategic Funding has only clawed back commissions once or twice in the past nine years, says Sederholt, the EVP.

The company works with a variety of brokers. Some have less than a 1 percent default rate and others have 12 percent to 14 percent default rates. As extra protection with brokers who have bad track records, Strategic Funding either declines to work with them at times, or has in place a stronger underwriting procedure with these deals.

Being more careful upfront is a better tactic than trying to go after commissions, which is extremely hard, Sederholt says.

Changing the Modus Operandi

While it’s not the industry norm, there are a few funders who have stopped using clawbacks, or are considering doing so, given all the headaches they can cause. Isaac D. Stern, chief executive of Yellowstone Capital LLC, a New York-based funder, says his company no longer tries to clawback commissions when deals go bust. The few times they tried to clawback commissions several years back, the brokers they went after were upset and threatened not to do business with them anymore. Yellowstone decided this approach was bad for business and that it would be more prudent to try something else.

“There’s too much competition, and if we were going to do clawbacks it would decimate our business,” he says. “It’s the broker’s job to bring in the deals. It’s our job to underwrite it. If something goes wrong on the deal, that’s on us. It’s not the broker’s fault.”

As protection, the contracts Yellowstone uses with brokers contain a provision allowing it to seek damages when fraud’s alleged. But in cases where brokers send what seems to be a legitimate deal that goes bad for something other than fraud, Yellowstone turns the other cheek. Yellowstone can afford to eat the $5,000 or $6,000 commission to ensure ongoing—and hopefully more positive leads—or so the thinking goes, according to Stern.

Overtime—if peer pressure continues to mount—it’s possible that more even more funders will decide chargebacks just aren’t worth the trouble. “I think the reason why some funders are moving away from [clawbacks] is because people are afraid of losing volume. Once one funder acquiesces, others will follow suit,” says Sheinbaum of Merchant Cash and Capital.

A Decade of Funding

July 7, 2015Next month is my 9 year anniversary in the merchant cash advance industry, which means I’ll be starting my 10th year. A decade of merchant cash advance… holy shit. I’ve had the opportunity to view it from many different angles and have accrued my fair share of adventures, plenty of which I’ve written about and others I’ll have to take to my grave.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

Looking back now, there weren’t many people keeping a live diary of events as the industry dove headfirst into the financial crisis. Who would’ve bothered to report on an industry that was arguably made up of only a thousand people?

In April 2009, even before AltFinanceDaily launched, I submitted a story to the only merchant cash advance magazine of its kind. It didn’t have a very clever name, just Merchant Cash Advance Publication. My story, titled, An Underwriter in Salesman’s Clothing, rambled on about the end of the industry’s glory days, the wave of declined deals in the recession, and how funders should be more appreciative of ISOs.

Here’s a summary of what I wrote more than six years ago:

Here’s a summary of what I wrote more than six years ago:

I was complaining about stacking as far back as 2007 apparently. I addressed it as a merchant problem. Merchants were taking advantage of funders, not the other way around like some frame the argument in 2015.

I left my post as Director of Underwriting in late 2008 because “I wanted the ringing phones, the commotion, the markerboards with stats, the glory, the $20,000 [monthly] checks.”

Funding companies became super conservative during the financial crisis and all my deals were being killed (25 deals declined in a row at one point.)

I had recently charged my first closing fee, felt bad about it, and got in trouble for it.

I said 1.40 factor rates wouldn’t last (I was wrong about this!)

I bitched about algorithmic declines (I apparently thought computers underwriting files was a good way to upset ISOs.)

I acknowledged my own hypocrisy when I realized how hard it was to be a sales rep after thinking sales reps were overpaid and overrated in my previous years as an underwriter.

I continued on as a sales rep for another two and a half years after I wrote that. That means that in 2010 when I started AltFinanceDaily, I was still calling UCCs, closing deals and boarding merchant accounts while sitting in a windowless room rented by a startup ISO.

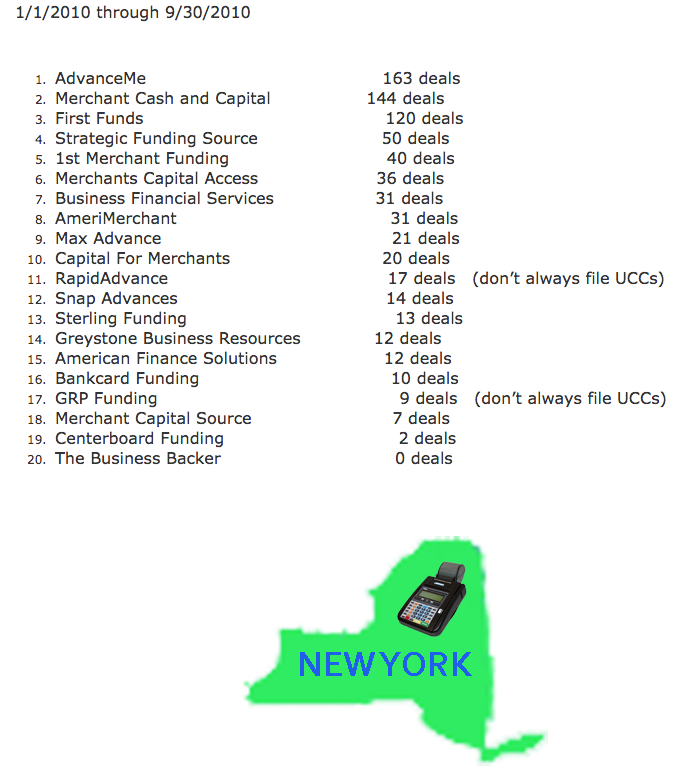

But what was there to blog about in 2010? Oh little stuff like who the biggest funding companies were at the time by checking UCC filings since almost everyone filed UCCs back then. Notably, the third largest merchant cash advance company of 2010, First Funds, is no longer in business.

I also wrote about shopping deals around and the impact that might have on a merchant’s credit report. That was the day-to-day stuff though, information I was just putting out there hoping someone on the Internet might see it. What got everyone excited was the 2010 New York State leaderboard which eventually prompted me to spend my nights and weekends investigating the industry on a wider level.

I began talking to people at other funding companies about their monthly numbers. It wasn’t that hard to get information as an industry insider, especially if you had deals to send somebody’s way. I also spent money to acquire secured party lists to count the number of UCC filings by funders in all 50 states rather than just look at one free state like I did with New York originally. I think I was the only person in the industry at the time running up their personal credit card bill to conduct such research. I had also been in the industry for four years at that point and had a great network of contacts who could clue me in on their volume.

While I said that I also looked at census records and department of labor records, I’ll admit that data wasn’t extremely useful. The end result was a best guess estimate that in 2010, there were approximately 21,000 merchant cash advances transacted for $524 million.

My data would go on to be republished in ISO&Agent Magazine, The Scotsman Guide, and Leasing News, and also end up in many other places I didn’t expect, like in the business plans of merchant cash advance companies that were looking to raise capital. In fact, in a private meeting I had with an MCA company months later in South Florida, the CEO let me take a peek at the docs they had just submitted to a bank for a credit facility. Included was a printout of these numbers with my name on it and all. Apparently there was something to this writing thing…

My last day as a sales rep was in the Fall of 2011. I left the commission-only life (oh what, you 2015 pansy closers actually get a base salary?) for something even more risky, an entrepreneurial life. For a couple years, I played underwriting consultant to a handful of merchant cash advance companies and industry expert to institutional investors interested in the space. I learned how to code in my spare time and spent more than a year in online lead generation.

I never stopped writing.

Along the way I’ve visited the offices of dozens of ISOs and funders, syndicated in deals, and test-drove new technology.

None of this makes me particularly special, especially when I hear about how much some of my old sales buddies are making these days on deals. “Are you SURE you don’t want to come back?” they ask. It’s enticing no doubt. A part of me wants to grab the phone out of their hand and attempt to shatter their record on the markerboard this month even though I’m pretty sure I’m rusty as hell.

One thing noticeable between now and 9-years ago is that my hair turned grey. This industry will do that to you (or at least it did to me.) And I still get a kick out of meeting folks who got into the industry years before I did. The 90s/early 2000s AdvanceMe crowd likes to tell me that they were funding merchants while I was still in diapers. They are practically right.

As I enter my own tenth year in the biz however, it’s exciting to think that the industry is just now getting started. OnDeck was the first IPO in the space and the general public is learning about short term business funding for the first time. There’s no shortage of news to report and that keeps me plenty busy these days.

And so even after a decade of MCA, it’s never too late to put on your Funded pants. Opportunity awaits and I hope you’ll continue to ride the wave with me. Thanks for reading since 2010!

Coming to the Rescue: Consolidation Can Save Merchants

June 24, 2015 In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

“Consolidations are a way to help merchants avoid defaulting,” said Chad Otar, managing partner at New York-based Excel Capital. Consolidation works if the buyout price is low enough and the terms allow enough room to handle the obligation.

“It can free up some cash and give the merchant some room to breathe, sustain the business and avoid taking on more debt,” he noted.

It’s helpful to think of consolidation as the equivalent of refinancing a house, according to Stephen Halasnik, managing partner at Payroll Financing Solutions, a Ridgewood N.J.-based direct lender. Payroll has been offering the service for about six months, he said.

Brokers and funders can benefit from consolidation because it puts a merchant back on track towards long-term sustainability, said a broker who requested anonymity. Moreover, the broker said that one in three of the potential deals he sees have multiple advances outstanding, which means companies could lose an alarming chunk of market share by declining too many potential funding candidates. “That’s what I believe the catalyst was to opening the doors to consolidation,” he contended.

SECRET TO SUCCESS

Success in consolidation lies in finding merchants worthy of another chance, said Otar. Clients who have taken two or three advances but stick to the new plan and stop stacking advances from other brokers have a reasonably good chance of succeeding, he said. His company can work with a merchant that has as many as three advances outstanding if they have sufficient revenue.

Otar provided the example of a merchant who’s diverting 20% of his gross revenue to three advances. Together, the advances have led to a total of $50,000 in future revenues sold. If the merchant generates enough monthly revenue to qualify for $100,000, Excel can buy out the three advances, provide the merchant with $50,000 in cash, and lower the payment to 8% to 12% of gross revenue. “All of a sudden they have all this cash flow to play with that really wasn’t there,” he said of merchants in that situation. “They tend to do really well.”

Halasnik of Payroll Financing Solutions offered the example of a trucking company that had taken three advances and was delivering a total of $1,138 a day on average to the funders. Payroll bought out the three funders and is charging the trucker $615 a day.

One of Payroll’s clients needed to repair a commercial vehicle but already had too many advances and couldn’t get another, Halasnik said. Payroll consolidated the positions and lowered the payment, enabling the merchant to save enough money in two weeks to have the vehicle fixed.

To qualify for a consolidation, the merchant has to meet the “50% Rule” by netting 50% of what Excel is offering, Otar said. Between 40% and 50% of the distressed merchants that the company considers for consolidation meet that criterion, he said. An additional 30% of the merchants can meet that standard in the near future, once they’re further along on their agreements.

Under the 50% Rule, a merchant that is still obliged to deliver $70,000 and qualifies for $100,000 would not be a candidate for consolidation, Otar said. In that situation, a merchant can wait until he has delivered more of the sold revenues to the funders and then get a consolidation, he said. “In the meantime, don’t take on any more debt,” Otar tells the merchants. That too could impact their ability to sell additional revenue streams in return for cash upfront down the road.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Brokers should also bear in mind that every deal’s different, cautioned Steven Kamhi, who handles business development and ISO relationships at Nulook Capital, a Massapequa, N.Y.-based direct funder. “It has to be the right deal,” he advises.

Brokers can identify distressed merchants within the first two minutes of a phone conversation when they say things like, “I need the money right now,” Otar said. Looking at the paperwork, the broker can see within 10 minutes whether the potential client is hard-pressed.

Asking the right questions helps reveal distress quickly, sources said. That can include asking how many advances the merchant has outstanding, how much in future sales they still have to deliver and how much revenue they’re grossing monthly. Asking what company advanced them cash can reveal a lot if they’re working with less-reputable companies.

Listening’s under-rated, too. Merchants sometimes explain that they’re coming up with more ways of making money and are, therefore, making themselves a better bet for sustainability, Otar said.

OTHER WAYS OF HELPING

Brokers can make deals more palatable to some distressed merchants by deducting payments weekly instead of daily, Otar said. “It’s something I’m seeing a big migration toward,” he noted. “It’s a big selling point.” Manufacturers and contractors don’t have customers swiping cards every day and especially appreciate the change. More widely spaced payments can also fit better with some clients’ seasonal cash flow.

Besides consolidation, brokers can help distressed merchants by providing traditional accounts-receivable financing, which can prove particularly helpful for manufacturers and construction companies, Otar said.

Suppose Customer A owes a contractor $100, Otar said by way of example. The contractor can get $90 from the factor, and the factor collects the $100 from Customer A. The client pays the cost of the financing upfront but reduces the waiting time to receive the cash and avoids daily or monthly payments.

Accounts-receivable financing costs merchants much less than a cash advance, Otar noted. But putting the deal together takes longer than approving an advance, and merchants in immediate need of cash might not be able to wait.

In another example of helping merchants, Payroll had a client who was a bicycle shop owner with good credit and equity in a home, so it granted him an advance that gave him time to go to a bank and get a home equity loan. “I counseled him to do that and then buy us out,” Halasnik said.

PREVENTING DISTRESS

On the sales side of the business, brokers can help distressed merchants by preventing stacking from occurring in the first place, sources said. Otar recommended, “listening to the customer, understanding the business and offering a product that is going to benefit the customer in the long run.” That way, the broker positions himself to work with the client for years, not two or three months. “At the end of the day, they appreciate that,” he said.

Halasnik relies on his experience as a small-business owner who has operated a printing company, staffing company and nurse registry to help him understand aspects of a client’s business that people from a purely financial background might not fathom.

Brokers seeking long-term relationships should know a client’s business well enough to advise against taking on more financial obligations when the time isn’t right, agreed Payroll’s Halasnik. However, after the broker urges caution, the decision rests with the business owner, he maintained. “We are on the same page as the client,” Halasnik said. “We are looking out for their best interest because, ultimately, we have to get paid back.”

THE CASE AGAINST CONSOLIDATION

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

When a merchant’s overextended, he should wait before taking another advance, Stern said. But when some merchants are denied another advance, they immediately seek out another funder, he maintained.

Yellowstone has put together a few consolidations but chooses not to create too many, Stern said. Some merchants find themselves a month or two away from going out of business unless they can find a source of cash, he observed. “They’ve been declined for that last credit card, and things are getting really rough,” he said.

Some members of the industry advocate coming together to improve standards and provide training. Wall Street’s testing and licensing could serve as an example, suggested one source. Background checks could also help root out unethical players, he noted.

But creating a training and certification infrastructure would prove a formidable task, according to Stern. The industry would have a hard time agreeing upon who should head a trade association to administer the standards, he said. He views the industry as a collection of Type A personalities – sometimes defined as ambitious, over-achieving workaholics – who would resist consensus. “It’s a nice idea, but I don’t see it working,” he said.

REASON TO BELIEVE

Though industry players are contending with some distressed merchants, Stern noted that the average credit score of his company’s clients is beginning to rise as the economy improves.

Though statistics on distressed merchants aren’t readily available, other industry veterans feel they’re not encountering as many now as a year ago. However, they said they may see fewer cases of distress because bigger players are beginning to offer consolidations.

“A year ago, nobody would consider doing it,” a broker said of consolidation. But as funders become more open to the product when they see competitors using it to gain market share. “It’s becoming more mainstream,” he said.

How brokers market their services can also determine how many distressed merchants they encounter, sources said. Using the same prospect lists that competitors use can lead to calling on overextended clients, they maintained.

Whatever the number of distressed merchants may be, stacking sometimes makes sense, said Halasnik. What if a client needs $30,000 to win a contract, and a funder is willing to provide only $15,000, he asked rhetorically. Perhaps another funder will put in $15,000, too.

Problems arise, however, if the two funders don’t know the merchant has made two deals because they happened the same day. It’s the kind of situation that sours some members of the alternative-funding community to consolidation. As Halasnik put it: “You’re dealing with somebody who’s in trouble. It’s the highest risk a lender could take.”

Is the Premium Gone in Peer-to-Peer Lending?

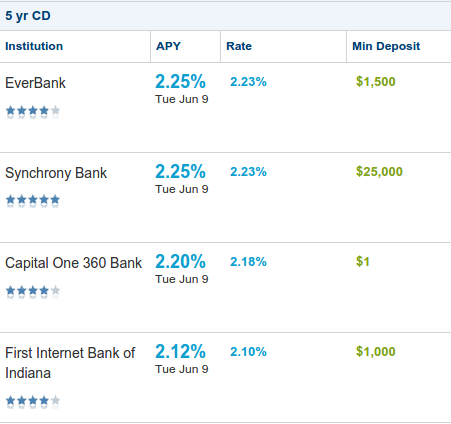

June 10, 2015FDIC insured 5-year CDs are now paying as high as 2.25% APR. Compare that against 5-year notes offered by Lending Club and Prosper that will pay ___________.

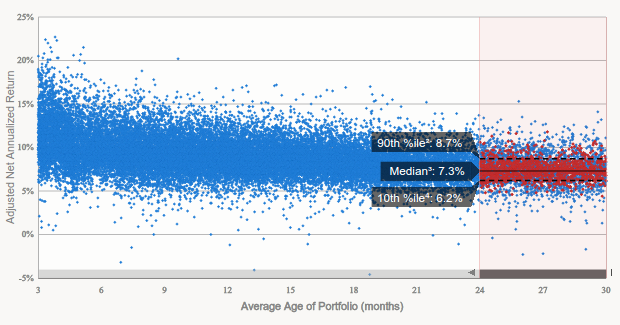

According to Lending Club, the average 2-year aged portfolio is yielding an average return of 6.2% to 8.7%. On loans maturing in 5 years, the numbers will be even lower. With peer-to-peer (P2P) lending being all the rage over the last few years, these returns look surprisingly benign.

Did something change?

According to Simon Cunningham’s LendingMemo analysis, investor returns have fallen almost 2% in two years. Cunningham wrote, “In 2014 something changed. Lending Club began to lower interest rates without adjusting FICO at all. Basically, for the first time in their company’s history they began to decrease the reward for investors without decreasing the risk.”

FICO stayed the same and rates came down, a move that was intentional and rationalized by Lending Club CEO Renaud Laplanche when he said, “By [lowering interest rates] we believe we can generate more positive selection. For example, this means people who now take a 10% loan offer, but who would have rejected a 12% offer, are typically also higher quality borrowers. So the belief is that part of the rate cut will be absorbed by lower defaults.”

Ironically, online business lender OnDeck, who has also lowered interest rates, might disagree with that psychology. Back on their Q4 2014 earnings call, OnDeck CEO Noah Breslow reported that their borrowers were basically taking the first offer they could get because of the time and stress associated with continuing the search.

For Lending Club, their gamble could mean that someone that would’ve taken a 12% offer is now taking a 10% offer even though they would’ve taken a 12% offer or a 15% offer or an 18% offer. Instead they are worried that borrowers will choose nothing if a loan is perceived to be too expensive. This experiment has wreaked havoc on investor yields.

“Folks shouldn’t enter this investment assuming a 7% return when they actually go on to receive 5.5%,” wrote Cunningham. He goes on to explain that average investor returns could go as low as 3.7%.

The price of risk

If you’ve been earning 0% in your savings account for the last few years, the returns in P2P have likely been a welcome reprieve. But as the probability that that Fed will soon raise rates increases, so too have riskless yields. According to bankrate.com, FDIC insured 5-year CDs are now paying as high as 2.25%, a figure that’s only 1.45% to 3.25% lower than Cunningham’s P2P estimates. Is the spread commensurate with the risk?

If you’ve been earning 0% in your savings account for the last few years, the returns in P2P have likely been a welcome reprieve. But as the probability that that Fed will soon raise rates increases, so too have riskless yields. According to bankrate.com, FDIC insured 5-year CDs are now paying as high as 2.25%, a figure that’s only 1.45% to 3.25% lower than Cunningham’s P2P estimates. Is the spread commensurate with the risk?

Previously, I’ve explained that Lending Club is not actually a middleman in a marketplace. No matter which notes an investor buys, they are in fact lending money to Lending Club itself. None of the notes matter if Lending Club goes bankrupt. An investor might as well be buying stock in the company.

Furthermore, none of the yield projections take into account a swift and brutal recession or a landmark legal ruling that could jeopardize an entire portfolio overnight. The loss of risk in Lending Club notes is your entire investment. It’s not just about the potential for low yield or negative yield. There is an inherent risk of total loss.

On a $100,000 investment, the added premium for a very risky asset over a riskless asset is potentially about $1,450 to $3,250 a year. Or is it?

Taxing away the premium

As loans default, investors might think they can offset the interest with their losses. That’s not the case because the interest is counted as normal income and the losses as capital losses. That means the losses can only be offset by capital gains income from other investments.

As loans default, investors might think they can offset the interest with their losses. That’s not the case because the interest is counted as normal income and the losses as capital losses. That means the losses can only be offset by capital gains income from other investments.

Therein lies the problem for an investor that has no capital gains. In that case, the IRS only allows individuals to deduct up to $3,000 in losses*. If someone is not investing outside of P2P lending, they’re at a big disadvantage.

Without capital gains, an investor could end up with this situation:

$10,000 in Lending Club interest income and $5,000 in Lending Club losses would result in being taxed on $7,000 in income (3k deduction limit). Talk about a yield killer.

With capital gains, any amount of losses can be offset against them.

On the Lend Academy forums, investors have hypothesized scenarios where the $3,000 limitation could lead to net yields below 1%!

To a relatively serious investor, the premium earned for investing in a very risky asset can be entirely wiped out by a tax limitation. Strangely then, the net dollar reward in a 5-year FDIC insured CD could potentially be the same as buying exotic consumer lending notes where total loss is very plausible. In that case, the notes offer no rational sense to invest in.

Indeed many P2P investors on the Lend Academy forums have reported plans to close their accounts or to invest only through IRAs where the tax rules are different.

Another tax

With P2P lending still a relatively young and confusing industry, a small retail investor may require the help of an accountant to prepare their returns, especially if they used folio where notes can be traded. Be aware that the hourly rate of tax preparation will cut into gains earned in P2P.

What’s in it for investors?

2.25% isn’t a very enticing offer, but neither is 5.5% if that’s the estimated figure barring any legal setbacks, bad recession, company failure, and tax consequences. As the economy prepares itself for an eventual increase in rates, the returns on savings accounts and CDs will rise over time. And yet Lending Club is curiously moving in the opposite direction. That’s great for borrowers, bad for investors.

The point at which it will no longer make economic sense to invest in P2P is eerily just around the corner if it’s not here already…

There’s No Room for More Competition

June 2, 2015 In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

There are basic facts that we can take from the “Broker Boom”

– Not enough beginning knowledge about this industry and how the Merchant Cash Advance process works.

– No time to make strong relationships: The concept of having “more” is usually more harmful than having a handful of trusting relationships.

– Overhead costs: the make-up costs from the spending on dead leads and the “start-up” costs of having an office, staff, draws – gave the wrong perception of what a “MCA” is when the rate mark ups pay for those expenses.

– Quick turnover when the top dog can’t fool the sales rep out of commissions any longer: Rep goes out into the world and starts their own company. This can lead to recycled bad practices or the few who want to do right.

– Co-Brokering: Everyone’s done it. I’ve done it. Edited agreements taken from other brokers/funders don’t always cover everything leading to many debacles that turn into “Jerry Springer” Forum threads. P.S. Don’t think merchants can’t see the forum either.

It’s absolutely exhausting to explain to someone from the mortgage industry or any industry that comes into the MCA space the “Rights” and “Wrongs” and the teachings. Most new Broker Company Owners and their sales come from those who don’t believe in “Best Practices” anyway.

Marketing and Leads in the Broker Space is affecting Brokers and Funders Alike – Are brokers ruining leads as well?

So, your questions about Marketing and Leads have the same answer- It does not matter what type of leads you get, it’s all about your presence, knowledge, and your “Handle”. These are the answers from actual merchants who get calls from UCCs. (This information came from old merchants that I had, I shortened the answers and stuck to the points).

- They don’t trust you because of your approach

- They tried before and was promised “X” and got a bunch of “Y” with excuses on how so many “Y’s” = “X”

- Backdoor calls- Sometimes the money isn’t the biggest savior- it’s the relationship that goes with it

- They don’t need it that bad to pay 30%. If they do need it- they want something structured to build their credit and keep their business afloat

When people think of getting money for their business- they used to think “Go to the Bank”. Professionalism, a structure that is always the same for each type of program, and knowledgeable staff they can rely on. They made the choice to come to your bank because of what is offered. Now, all but the “Capital” part is missing from this equation, but merchants still want to have that one consistent place to go to for their business needs.

I think we all lost sight of this Industry.

Brokers = Resellers and Marketers of Direct Funding programs. The Broker takes the programs from these Direct Funders and builds a portfolio of which each tier and industry and credit rating is satisfied by which funders he can qualify them to. The options are given to the merchant to satisfy their need for working capital.

You work for the Funder – Your Sales Target is the Merchant.

The Merchant has put everything into starting and maintaining their business. Most of them wanted the “American Dream” of owning a business since childhood. They have it now, and you come in and try to tell them what they need. Some believe you- some are money hungry and know the game. It’s all a numbers game no matter what kind or type of leads you buy.

All that am I saying is, the way this industry is looked at from a “Brokers” and “New-Age Funders” point of view vs. a “Veteran Broker” or “Veteran Funder” is two totally different aspects.

Unfortunately, there is no immediate solution for new “Brokers” and many solutions for the “New-Age Funders” to be on the path of “Best Practices” and less shenanigans.

There is no room for competition as we don’t know what we are competing for and rather than creating a solution so those leads can understand the growth and structure of what we are offering, we are too busy trying to find out how to get leads that won’t stick.

A Q&A With LendingRobot

April 12, 2015 SEAN MURRAY (SM): I’m a casual Lending Club investor that has purchased more than 2,000 notes. I like to think that I’ve been pretty good with my picks but I feel like the rush to get the most attractive notes has only gotten more competitive. I’ve also got a perennial issue of idle cash and the pressure to put it to work on the platform can feel like a burden when I’m busy with everyday life. I feel like I can do better but I have reservations about relinquishing control.

SEAN MURRAY (SM): I’m a casual Lending Club investor that has purchased more than 2,000 notes. I like to think that I’ve been pretty good with my picks but I feel like the rush to get the most attractive notes has only gotten more competitive. I’ve also got a perennial issue of idle cash and the pressure to put it to work on the platform can feel like a burden when I’m busy with everyday life. I feel like I can do better but I have reservations about relinquishing control.

I noticed in January that you raised $3 million from Runa Capital, which caught my attention.

So for both myself and our readers, can you explain in a nutshell what LendingRobot does?

EMMANUEL MAROT (EM): First off, that ‘burden’ is the exact reason why we started LendingRobot, as my partner and I were feeling it as well! We automate the whole investing process (decision and execution) to simplify access to marketplace lending for individual investors.

EMMANUEL MAROT (EM): First off, that ‘burden’ is the exact reason why we started LendingRobot, as my partner and I were feeling it as well! We automate the whole investing process (decision and execution) to simplify access to marketplace lending for individual investors.

(SM): I think one of the biggest concerns for casual investors is the question of who physically possesses the cash. Obviously they have already come to accept that Prosper or Lending Club will hold their cash, but what about a service like yours? Do investors send you the money to invest it on those platforms?

(EM): That’s a very valid point. As of today, we do not have what the regulator calls ‘custody’ of the money. Our clients wire the money on the platform, they give us a programmatic access to their account there so we manage it for them. There is no way we can touch their money, and when the money is wired outside of the platform, it has to go back to the original bank account anyhow.

(SM): How do you bill for your fees? Do you need to provide bank account information? Credit card?

(EM): Since we cannot touch our client’s money, we need another way to charge our fees. We use credit card. Up to $10,000 we do not charge anything and clients don’t even have to enter a credit card.

(SM): What is the difference between your service and Lending Club’s Automated Investing?

(EM): As the issuer of the notes, Lending Club cannot offer an ‘unfair’ advantage to some investors, therefore their automated investing cannot be used to get access to the most popular assets. Obviously, it’s also entirely based on their own credit model, and one cannot benefit from a second layer of risk modeling. At last, we tend to offer more features, such as additional filtering criteria, cascading investment rules or cash-flow forecast. We posted a comparative explanation a while ago that is still somewhat valid: http://blog.lendingrobot.com/post/69219879518/lendingclub-re-introduces-prime

(SM): If I use your service, can I cancel it at any time?

(EM): Absolutely, no setup or entry fees, no exit fees, no minimum usage period.

(SM): There seems to be correlation between a borrower’s home state and the default rate, can I filter out certain states with your service?

(EM): Yes, not only do we offer over 25 different filtering criteria, but it’s possible to mix them freely. Some clients start with our own proprietary model, then add extra criteria, such as ‘36-months’, or ‘Exclude Nevada’.

(SM): What did you guys do before founding LendingRobot?

(EM): Tons of stuff! My partner and I met at Microsoft, which we both joined after selling our respective startups. We decided to create something together even before knowing what to do. Incidentally, we started the company with a very different project (see http://www.eventiles.com/). As mentioned above, we started LendingRobot out of personal need.

(SM): What’s the smallest amount someone can allow LendingRobot to manage if they just wanted to try it out?

(EM): Right now, our smallest client has… $66.49 invested! That being said, we recommend people to invest at least $5,000 to be diversified enough.

Background on Emmanuel Marot

Emmanuel Marot is a polymath and serial entrepreneur. A French ‘grandes école’ graduate with a major in Computational Finance, Emmanuel started his career in product marketing at Apple. He also worked for the French intelligence agency to modernize the handling and presentation of highly classified information and acted as freelance graphic designer.

At age 26, he created his first company, a Web agency that he grew up to 15 people while keeping the net operating margin above 30%. The company created the first virtual reality cd-rom (Guinness book of records, 1995) and produced mobile Internet services as early as 1996. After selling it, he co-founded a larger communication agency, with 400 employees and an annual turnover of 30 million Euro. In 2000, Emmanuel patented a novel way to access mobile sites and created his 3rd company, which Microsoft acquired six years later. Emmanuel orchestrated the move of the entire operations to Redmond, WA, and became Director, Mobile Search at Microsoft.

He left in 2008 to research algorithmic trading, predicting market reversals from search engine queries. In parallel, Emmanuel did multiple executive consulting engagements for startups and corporations. He began to focus his work on the design of algorithms to automate decisions, and co-created Eventiles, an iPhone application that crafts meaningful stories from bulk pictures.

In 2013, he combined his interests in finance and algorithms and co-created LendingRobot, a solution for marketplace lenders to automate and optimize their investments. Emmanuel passed the Series 65 Investment Adviser law exam in January 2014.

From Lowes to Loans: Meet William Ramos

April 12, 2015Non-bank financing changed William Ramos’ life. Not as a borrower, but as a mover and shaker in the competitive world of financial deal-making. As an ambitious 20-year old, Ramos was working at both Lowes and ShopRite to try and put himself through Staten Island Community College. These were stepping stones, he told himself. He was dedicated to bettering himself, or more aptly to be the best at whatever he did.

Already on a path to success, he found himself growing impatient. The life of two jobs and school was a slow grind. Ramos wanted to do something big. He wasn’t sure what it would be, but he was confident that his attitude combined with his strong work ethic would eventually lead him to great success.

And so one day, he made a promise to himself to go out and find that big thing rather than wait for it to find him. It’s a bit of an American Cliché to say that his lucky break coincided with a sudden bout of adversity, but that’s exactly how it played out. Raised in the tough neighborhood of Brownsville in eastern Brooklyn, he didn’t have the connections to step right into the business world. Instead, Ramos had to start his search on the ground floor with millions of others on Craigslist.

His luck began with an interview for a job in telemarketing, a role that meant being connected to an autodialer nine hours a day as an opener. Undeterred by the challenge, Ramos had a feeling that this is where it would all begin. “I’ll do it,” he said.

There was only one problem, they didn’t want to hire him. The firm, which sold mostly financing products to small business owners, was very selective, even with cold callers. His interviewer at the time, who later became his boss, confirmed to me that he didn’t think Ramos was the right fit after they first met. But Ramos was determined to change his mind.

After calling the firm repeatedly over the next week to convince them that he was up to the task, they finally acquiesced. It didn’t mean he was in. It just meant it was time to put up or shut up. “They gave me a three-day trial period,” Ramos said.

After calling the firm repeatedly over the next week to convince them that he was up to the task, they finally acquiesced. It didn’t mean he was in. It just meant it was time to put up or shut up. “They gave me a three-day trial period,” Ramos said.

His former boss confirmed this relentless persistence.

39 working hours, 3,000 calls, and 3 days later, Ramos brought in two deals, one for $100,000 and another for $35,000. They both went through.

It was more than good enough to survive the trial and he was offered a job to work full time.

With a starting compensation of only $250 a week + commission, he still had a long way to go. “I would be the first one in and last one out,” Ramos shared with me. “I kept my head down and I wouldn’t leave my seat unless I needed to use the bathroom or eat. All I would do is make my calls.”

His former boss explained to me that Ramos had a knack for bringing in the firm’s larger deals even from the very beginning. He was too junior early on to be making a lot of money, but they were very focused on developing his skills. The firm saw his potential and was committed to nurturing him.

Within the first three months he managed to save $700 and he used it to buy a Mercedes-Benz C240 from a co-worker. After a life of taking the bus to work, Ramos had reached his first milestone of success.

While it was obvious that he still harbors pride in that first car, it sadly became all that stood in the way of homelessness. He had sacrificed everything for this job including college. Unfortunately there would be just one more thing to lose.

Adversity struck when a series of unfortunate events suddenly left him without a place to live. Ramos’ car was now both his ride and his home, though with the long hours he was putting in at the office, he might as well of lived at his desk. His boss took a special interest in his life and soon discovered just how much his young protégé was struggling.

“He was literally sleeping in his car,” his former boss told me. “I offered to let him sleep on my couch or at the very least let him stay in the office,” he added. Ramos took him up on the latter and began sleeping at the office. At the same time his commission percentage was bumped up, which sweetened the potential and only encouraged him to keep going.

Always looking for an edge, he sometimes pretended to be a customer himself. “I would call up lenders as a merchant to hear what pitches their sales teams were using,” he said. “I would then take that pitch, tweak it and make it my own.”

Always looking for an edge, he sometimes pretended to be a customer himself. “I would call up lenders as a merchant to hear what pitches their sales teams were using,” he said. “I would then take that pitch, tweak it and make it my own.”

Soon he was regularly closing more than $500,000 a month in deal flow and his financial situation and lifestyle began to improve significantly. A little more than a year later, Ramos had risen up to become a sales manager and was overseeing a team of five members.

Now some people in his shoes might’ve decided not to press their luck. He had taken a major gamble and it had paid off, so why do anything to jeopardize it?

But Ramos didn’t leave everything behind to settle for pretty good and a middle class lifestyle. After two years, he gave his boss and mentor some bad news.

“I’m going off on my own,” he explained. They parted on amicable terms and to this day still do business with each other. Ramos’ last commission check there was for $15,000, an amount he had never imagined back in his Lowes days.

In 2013 he founded Supreme Capital Group, a firm that primarily brokers merchant cash advances but will fund A paper deals on its own. With only two years in business, they are already on pace to generate more than $1.5 million in revenue over the next 12 months. He excitedly recalled a recent deal that generated $66,000 in commission. And that was just one deal!

He attributes part of his success to strong organizational skills. “I don’t think brokers realize how important keeping track of all their data is,” he said. He went on to explain that he can email the list of all his old leads and turn that into six to ten closed deals easily. He doesn’t have to work as much as he used to, but he still does.

With 10 callers working for him now, he’s not content with just being the boss. “I am still currently pounding the phones, doing email marketing, and sending out mailers,” he said. “We use the mailers to follow up with merchants, and we get a great response from it,” he added.

After working incredibly hard for several years, Ramos has at least found the time to play hard too. In the summer of 2014, he had made enough money to buy a white Maserati GranTurismo MC Sport Line, of which he shared several photos with me. He’s since upgraded to a 2013 Ferrari California in a color he described as Pepsi blue. And while that might be the kind of car some people would dream of sleeping in, Ramos has said those days are long over.

After working incredibly hard for several years, Ramos has at least found the time to play hard too. In the summer of 2014, he had made enough money to buy a white Maserati GranTurismo MC Sport Line, of which he shared several photos with me. He’s since upgraded to a 2013 Ferrari California in a color he described as Pepsi blue. And while that might be the kind of car some people would dream of sleeping in, Ramos has said those days are long over.

He just bought a house in Mesa, Arizona where his fiancée grew up and he plans to relocate his office there. “It’s already in the process of being built,” he said.

Ramos is now just 25 years old. He said he regrets not finishing school and he plans to go back. But he wouldn’t change everything that happened to him. He stressed more than once that asking questions is something he considers to be very important to success, especially in the business he’s in. “For all the newcomers in the industry, my advice would be to work hard and ask a lot of questions,” he said.

He was certain he had found the right opportunity almost from the beginning. “I knew that if I made those commissions the first week that I could make more,” he said.

It wasn’t easy.

William Ramos is the President of Staten Island, New York-based Supreme Capital Group.

Year of the Broker

April 4, 2015 Many of the newcomers are fleeing hard times in the mortgage or payday loan businesses. Others are abandoning jobs selling insurance, car warranties or search-engine optimization.

Many of the newcomers are fleeing hard times in the mortgage or payday loan businesses. Others are abandoning jobs selling insurance, car warranties or search-engine optimization.

“You have wandering souls trying to find their place in this industry, whether it be as a company or on their own,” said Amanda Kingsley, CEO of Sendto, a Florida-based company that assists new brokers.

Though exact counts appear difficult to obtain, Kingsley professed amazement at the volume of new entrants. “I’m swamped,” she said. “It’s crazy.”

Some of the new brokers discovered alternative financing in December, when OnDeck Capital’s initial public stock offering raised $200 million and valued the company at $1.3 billion. The Lending Club IPO that raised $1 billion the same month also raised public awareness of alternative loans.

Mesmerized with those whopping figures, salespeople from other businesses began committing themselves to a new career in alternative finance. In a business with virtually no barriers to entry, it’s easy to get started. To call themselves brokers, they just need a phone, someplace to sit and a list of leads they can buy online.

Virtually all of the entrants are pursuing dreams of lucrative paydays. Many even expect to make a fast buck with minimum effort.

If only it were that simple. Too often, the untutored new players are making mistakes simply because they don’t know any better, industry veterans maintained.

“A lot of people think you can just walk in and be successful,” said the sales manager of an established New York-based brokerage who asked for anonymity. “They don’t know what it takes to run a company. They don’t know what it takes to get a deal done.”

Worst of all – either unknowingly or with evil intent – new brokers are stacking deals. In other words, inexperienced salespeople pile second or third loans or advances on top of original positions. It’s an approach that clearly violates the industry’s standards, observers agreed.

In fact, virtually all contracts for a first loan or advance prohibit the merchant from taking on another similar obligation, noted Paul Rianda, an Irvine, Calif.-based attorney who specializes in payments and financing.

“I can’t remember one agreement I’ve seen that didn’t have that provision in it,” Rianda said.

Violating that stipulation could provide grounds for a lawsuit, and litigation is underway, according to David Goldin, president and CEO of New York-based AmeriMerchant and president of the North American Merchant Advance Association (NAMAA).

Bigger funders would sue smaller funders because the latter appear more likely to take on riskier, more problematic multiple-position deals, said Jared Weitz, CEO at United Capital Source LLC, a New York-based broker.

Plaintiffs have a case to make because stacking harms the broker and funder of the first position by increasing the risk that the merchant won’t meet the resulting financial obligations, Weitz said. “The guys going out 18 and 24 months to make this a more bankable product are being hurt by the people coming in and stacking those three-month high-rate loans,” he noted.

Deducting fees for more than one advance also impedes cash flow, adding another risk factor, Weitz said.

To further complicate matters, the company offering the second or even third deal sometimes moves the merchant’s transaction services to another processor, Rianda said. That forces the firms that made the first advance to approach the new processor to stake a claim to card receipts, he noted.

So the companies with the original deal suffer from the effects of stacking, but the practice’s shortcomings will haunt the stackers, too, observers maintained.

“It’s not a model that’s going to allow them to succeed,” a broker who asked to remain anonymous said of stackers’ long-term prospects.

Many hardly give a thought to staying power, according to Weitz. “A lot of people entering this space think it’s about fast money and not longevity,” he said.

Longevity requires that brokers build relationships with merchants, a process stacking undermines because too much credit can drive merchants out of business or merely prop up merchants already doomed to fail, sources said.

Yet stacking has become so widespread that it constitutes a business plan for some brokerage shops, said a broker who asked that his name and company not appear in the article.

It can begin when brokers buy lists of Uniform Commercial Code filings to find out what merchants have already taken out term loans or advances, said Zach Ramirez, vice president of sales and operations at Orange, Calif.- based Core Financial Inc.

The brokers then contact those merchants, many of whom are already over-extended financially, to offer additional credit or advances, Ramirez said.

Inexperienced brokers often resort to stacking because they don’t know how to generate leads that can bring alternative lending vehicles to merchants who weren’t aware of them.

Referrals from accountants or other business owners who deal with merchants can provide some of those greenfield prospects, Ramirez noted.

And leads aren’t the only area of cluelessness among newcomers, a broker who requested anonymity maintained.

And leads aren’t the only area of cluelessness among newcomers, a broker who requested anonymity maintained.

“They don’t know why a bank declines a deal or approves a deal,” he said. “They don’t know what’s the basis for a good deal.”

To teach new brokers those basics of alternative business financing, the industry should establish standard policies and technology, according to Kingsley.

A credential, perhaps something similar to the Certified Payments Professional designation created by the Electronic Transactions Association, sources said. To earn the credential, candidates would pass an exam to show they’ve mastered the basics of the business, they proposed.

NAMAA is considering such a credential, said Goldin, the trade group’s president. It’s the kind of self-regulation that could forestall federal oversight, industry sources agreed.

But that might not matter, according to Tom McGovern, a vice president at Cypress Associates LLC, a New York-based advisory firm that raises capital for alternative lenders and merchant cash advance companies.

After all, McGovern noted, Barney Frank, former Democratic U.S. representative from Massachusetts and co-author of the Dodd-Frank Wall Street Reform and Consumer Protection Act, has gone on record as saying that piece of legislation focuses on consumers and does not govern business-to-business dealings like loans or advances to merchants.

That lack of regulation over B2B deals seems likely to continue, “especially in the world we’re in now with a Republican Congress,” said a broker who asked to remain nameless.

However, some members of the industry would welcome federal regulation as a way of barring incompetent or unscrupulous brokers. An agency patterned after the Financial Industry Regulatory Authority, know as FINRA, could do the job, suggested a broker who requested anonymity.

Whether a government regulator or an industry- supported association should police the market, problems could remain stubbornly in place, some said.

Many doubt an association could build the consensus required for united action on some issues – stacking in particular.

For one thing, cleaning up the business could reduce profits for brokerages that profit from stacking, noted a broker who asked that his name not appear in the article.

“Everybody wants to make money,” he said. “Everybody’s out for themselves.”

Another barrier to agreement arises because some brokerages fear cooperation could expose their trade secrets, said Sendto’s Kingsley.

Moreover, unscrupulous brokers want to keep their employees uninformed of the industry’s potential for big profits, Kingsley said. That way they suppress compensation for an underclass of prequalifiers who work the early stages of deals, she noted.

Prequalifiers earn from $150 to $500 a week, depending upon the location, and don’t qualify for benefits like health insurance, Kingsley said. Once they realize what a tiny portion of the profits they’re receiving, brokers terminate the prequalifiers and many go on to become brokers themselves, she observed.

Closers who take over from prequalifiers to wrap up the sale can earn up to 50% or occasionally even 60% of a brokerage house’s commission – if the closer originates the deal and sees it through to completion unassisted, Kingsley said.

Eventually, closers realize they could keep all of the commission if they strike out on their own and become brokers, she noted.

In a way, the progression from prequalifier to broker or closer represents a market correction. And many seasoned industry participants believe market forces will also work out other problems the influx of new brokers is causing.

A large number of the new brokers simply won’t last long because they don’t understand the industry, they’re stacking deals and they’re signing up merchants that won’t stay in business.

Meanwhile, funders are beginning to perform background checks on brokers to make sure they’re dealing with reputable people, sources said.

Some funders protect themselves by simply declining to do business with new brokers, according to observers.

And many new brokers are learning the industry with the help of experienced brokerages that act as mentors and conduits and call themselves super brokers, super ISOs, broker consultants or syndicators.

“So what I’m saying is, ‘Guys, let’s not compete. Let’s grow parallel together,’ ” Weitz said of United Capital Source’s relationships with new brokers. The company began working with new brokers in October 2014.

In such relationships new brokers get advice from the more seasoned brokers. The older brokers can also provide the newcomers with services that include accounting, marketing and reporting, he said.

New brokers can also benefit from the customer relationship management platform that United Capital Source developed, Weitz said.

The new brokers also capitalize on the older brokers’ relationships with funders. Established brokers have earned better rates and terms because of reputation and volume, Weitz noted. Companies like his also know which lenders work more quickly and thus capture more deals, he added.

Older brokers can also steer new brokers away from newer funders that offer shorter terms and demand higher rates, Weitz said. Of the 30 to 40 companies that call themselves funders, only eight or 10 deserve the name, he contended.

The less-respectable funders place only a small amount of money in a few deals, he said.

Newer brokers become aware of their need for help from more experienced brokers when they see how many sales they’re failing to close, Weitz said.

The new brokers also come to realize that the puzzle of running a brokerage office has a lot more pieces than they may have thought, said Kingsley.

The new brokers also come to realize that the puzzle of running a brokerage office has a lot more pieces than they may have thought, said Kingsley.

The percentage of the commission that the older broker charges can vary, according to Weitz.

“If someone needs a lot of hand holding and a lot more resources, they would get a different structure,” he said.

While Weitz said his company plans to acquire only about 10% of its volume through new brokers, Sendto specializes in helping newcomers. Sendto’s Kingsley described the company as “a turnkey solution that provides training and placement of deals. It’s for new brokers or sales offices that do not have what they need to be part of this industry.”

There’s room for entrants because not all merchants know about alternative business financing, said McGovern.

The market can even seem like it doesn’t have enough brokers in the estimation of experienced players skillful enough to find the many merchants who haven’t been introduced to the industry, said Ramirez of Core Financial.

And the big banks don’t really want the business because the deals aren’t big enough to interest them, McGovern said.

But the potential profits look promising to outsiders disillusioned with sales jobs in other industries.

Some experienced brokers even prefer to hire salespeople from outside the alternative financing industry, noted Kingsley. That way, they avoid employees who have picked up bad habits at other brokerage houses, she said.

Long-time members of the industry sometimes enjoy belittling new entrants who can seem clueless about the business they’re trying to master, noted Ramirez of Core Financial. But he recalled the time not so long ago that he himself had a lot to learn.

And regardless of how unsophisticated they may seem, new players have a role, McGovern said.

“They are performing a service,” he maintained. “They’re like the missionaries of the industry going out to untapped areas of the market – of which there are many – and drumming up business.”

To Kingsley, brokers in general – old and new – are beginning to earn the respect they deserve.

“A lot of people are afraid of the word ‘broker,’ ” she said. “I feel that 2015 is the year of the broker, and people should embrace what a broker can actually do. It’s a great thing.”