Q&A With Noah Breslow On Replacing ACH For Realtime Funding and More

October 25, 2017 An announcement by OnDeck, Ingo Money and Visa this week at Money2020 may be more consequential than it appeared. That’s because the partnership enables OnDeck to actually fund a merchant’s bank account (not their debit card) on days, nights, weekends, and holidays. Such a feature is not possible in the realm of ACH where funding typically takes place on the next business day and only if the transaction is submitted before a predetermined cutoff time. AltFinanceDaily got to learn more about how this works in an interview with OnDeck CEO Noah Breslow on Tuesday as well as the opportunity to pick his brain about a few other things. Below is a curated excerpt of the interview that has been edited for brevity.

An announcement by OnDeck, Ingo Money and Visa this week at Money2020 may be more consequential than it appeared. That’s because the partnership enables OnDeck to actually fund a merchant’s bank account (not their debit card) on days, nights, weekends, and holidays. Such a feature is not possible in the realm of ACH where funding typically takes place on the next business day and only if the transaction is submitted before a predetermined cutoff time. AltFinanceDaily got to learn more about how this works in an interview with OnDeck CEO Noah Breslow on Tuesday as well as the opportunity to pick his brain about a few other things. Below is a curated excerpt of the interview that has been edited for brevity.

AltFinanceDaily: For this real time funding you announced, do you have to have a Visa debit card?

Breslow: You do not, but you have to have a debit card. 70% of small business owners have debit cards. And this will work with Visa or Mastercard.

AltFinanceDaily: So you’re not actually funding a merchant’s debit card, you’re funding their bank account but using the Visa network as the mechanism?

Breslow: It’s the rails, it’s the way to get the money into a small business owner’s checking account. My prediction is that every funder in the industry is going to be doing this in a couple of years. It’s going to be faster and small businesses will start to expect it. Now instead of waiting 2 days to get the money into someone’s account, it can be done on nights, weekends, holidays, 365 days a year.

AltFinanceDaily: So you can fund a merchant’s bank account on the weekend?

Breslow: Yes, it’s real time. And to be clear we partnered with Ingo Money, Visa has the rails. Ingo is our interface point, they do the PCI compliance and the rest. We looked at a bunch of different players in the market and Ingo was unique in that they had covered small business checking accounts. Some of this stuff is happening in consumer already. We’re the first lender to use these rails for either consumer or small business in the US.

AltFinanceDaily: Has this already gone into effect?

Breslow: No, it’s coming out in a couple months. Early 2018.

AltFinanceDaily: Does this system work with every bank already?

Breslow: It doesn’t work with every bank yet. It works with most of them, all of the major ones.

AltFinanceDaily: Speaking of payments… Square. PayPal. They’re both payments companies first that went into lending. Is there a potential reverse play for OnDeck to go into payments?

Breslow: Right now our product expansion stuff is very focused on additional lending products. I still feel like we haven’t lived up to our full potential there. There’s a couple other product categories that we’ve looked at and thought about. Equipment finance is one, invoice factoring, small business credit cards. And so we look to be the best small business lender in the world with the best set of products. And then we can partner with a lot of the payments companies. But right now, no we’re not going to sell merchant processing. Never say never, but not in the near future.

AltFinanceDaily: Any news on the Chase front?

Breslow: We re-upped our agreement with them in early August. The customer experience is amazing, our platform is scaling, and we’re making progress. I can’t tell you a lot of other details about it.

AltFinanceDaily: I’ve heard from folks in the industry about merchants who are being debited by Chase either daily or weekly. Is that you?

Breslow: That would be our platform. Chase’s product is more or less like the OnDeck product but cheaper obviously. It’s a daily or weekly collected loan. It goes up to 24 months for $200,000.

AltFinanceDaily: I want to ask you about brokers, or as you call them “funding advisors.” Do you anticipate reliance on them increasing or decreasing?

Breslow: Stable. I don’t anticipate it moving up or down. We really like the funding advisors that we have and we’re continuing to grow with them. We’re also adding some new ones.

AltFinanceDaily: What makes a good broker? What can they do to do things right?

Breslow: The value equation between the merchant, the lender and yourself has to be in balance. They should also be efficient and know the credit box of the lender they’re working with. They should invest in their employees, train them, and they should become more sophisticated about their online marketing and CRMs, which we’ve been seeing.

AltFinanceDaily: Everyone’s talking about blockchain at this conference. Is there a way that blockchain fits into online lending and possibly OnDeck?

Breslow: I love the technology, I’m very intrigued by it. But we’re not actively using it and it’s not like I have a secret blockchain project in the works.

AltFinanceDaily: Is there a universe in which OnDeck considers making an acquisition of a company?

Breslow: So we’re not totally opposed to that. They’re might be an opportunity for a complementary product or a complementary team. I think you’re going to see a lot of consolidation in the industry in the next 3-5 years.

OAREX Secures $10,000,000 in Funding, Strengthens Digital Media Presence

October 24, 2017

CLEVELAND, OH – OAREX Capital Markets, Inc. (“OAREX”), a leading non-bank financing institution providing financing for digital media companies, today announced that it has closed on a $10,000,000 line of credit from a group of lenders, led by Arena Investors, LP, a New York-based global investment firm.

OAREX accelerates programmatic advertising revenue for digital publishers such as websites, app developers, ad networks and supply-side platforms. Accelerated cash flow allows media companies to scale their content promotion and user acquisition campaigns, and pay supply side partners and vendors sooner.

“This transaction significantly improves our ability to fund publishers,” Hanna Kassis, founder & CEO said. “It will allow us to continue to provide liquidity in a timely and efficient manner, allowing clients to better match their income with expenses to scale rapidly,” said Kassis.

Since inception, OAREX has helped accelerate programmatic advertising revenue for hundreds of websites and apps, and has purchased millions of dollars in outstanding receivables. “We tailor our service to our clients’ individual needs, making sure they’re positioned for growth,” Kassis said.

Capital & Credit as a Service

OAREX offers a non-loan product, making it appealing to many new digital media companies that are not interested in assuming debt and providing personal guarantees. OAREX accomplishes this by financing publishers’ advertising receivables, providing immediate liquidity for growth. Clients can sign up for one-time funding, or a monthly facility between 6 and 12 months. OAREX funds clients on a weekly or monthly basis, depending on their needs and cash flow.

“We are not a lender,” Kassis said, “we are a capital partner with the aim of helping clients grow.” OAREX takes a hands-on approach to servicing its clients, despite newly developed back-end technology that allows OAREX to verify receivables instantly. “We believe human interaction is critical to our providing the best service, even in the digital age,” said Kassis. As a value-add, OAREX offers a database to clients of all payment, collection and credit data on ad networks, ad exchanges and other intermediaries in the digital media ecosystem. “If this information can help our clients, then it can only help us by sharing it with them,” said Kassis.

About OAREX Capital Markets, Inc.

OAREX Capital Markets, Inc. (www.oarex.com) provides fast, flexible funding for companies in the digital media ecosystem earning revenue from advertising, affiliates and marketplaces such as the App Store. Established in 2013, OAREX is an acronym for the “Online Advertising Revenue Exchange”, and is located in the heart of Cleveland’s historical Tremont neighborhood. For more information, please contact Hanna Kassis or Taylor Haddix at (855) 466-2739.

About Arena Investors, LP

Arena Investors, LP (www.arenaco.com) is a global investment firm and merchant capital provider that invests across the entire credit spectrum in areas where conventional sources of capital are scarce. Arena focuses on corporate private credit, real estate private credit, commercial & industrial assets, structured finance, consumer assets as well as structured private investments in public securities.

####

ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

September 28, 2017 ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

The debt settlement companies “mislead the merchants as to the services they will perform and the cost to the merchant, and they also conceal their relationships with the ISO Defendants and the fact that they or their affiliates are introducing these same merchants to merchant cash advance providers like Plaintiffs only to later induce those merchants to breach their agreements with their cash advance providers,” the complaint states.

Among the named defendants are:

- Corporate Bailout, LLC

- Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group

- PLG Servicing LLC

- American Funding Group

- Coast to Coast Funding, LLC

- ROC South, LLC

- Mark Mancino

Several defendants are already best known for running an office “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street,’” according to a salacious story that graced the back cover of the New York Post last month.

One paragraph of the complaint summarizes the allegedly collaborative scheme like this:

American Funding, Coast to Coast, […] (the “ISO Defendants”) are independent sales organizations (“ISOs”), companies that ostensibly support the merchant cash advance industry by brokering merchant agreements for companies like Plaintiffs. The ISO Defendants are anything but the proverbial “honest brokers.” As alleged below, they have partnered with companies that purport to offer debt relief services to merchants who have agreements with merchant cash advance companies like Plaintiffs. In practice, for these companies, “debt relief” is a code word for deceiving merchants to breach their existing agreements with Plaintiffs and to instead pay fees to these debt relief entities. In short, they scam merchants into believing that they can save them money when, in fact, they leave these merchants in financial shambles, while causing Plaintiffs to suffer millions of dollars in losses and future los[t] profits.

“’DEBT RELIEF’ IS A CODE WORD FOR DECEIVING MERCHANTS TO BREACH THEIR EXISTING AGREEMENTS”

Central to the plaintiffs’ claim is that they have ISO agreements with the defendants and that the defendants’ conduct is a breach of those agreements. The three causes of action alleged are tortious interference with contract, conversion, and breach of contract. Plaintiffs claim that 100 merchants with more than $3 million in outstanding balances are in breach of their contracts because of the defendants’ conduct.

The complaint was prepared and filed by attorneys at Proskauer, a 142-year old law firm founded in New York City.

Debt Relief Under Fire

The small business debt relief industry has been marred by scandal in recent years. In an unrelated criminal matter being handled in the Western District of New York, the owner of Corporate Restructure Inc. (no ties to Corporate Bailout) is currently residing in the Niagara County Jail awaiting trial on charges of conspiracy to commit mail fraud, wire fraud, bank fraud and money laundering for failing to deliver the debt relief services it charged for. In that case, United States vs. Sergiy Bezrukov, Bezrukov advertised that he could reduce a merchant’s short term debt by up to 75%. He is facing up to 30 years in prison. He was also previously a merchant cash advance ISO.

Two other MCA funding companies, Pearl Gamma Funding and Pearl Beta Funding, filed a lawsuit last November against another debt relief company that calls itself Creditors Relief. The complaint in that case also alleges tortious interference with contract and is still pending.

Meanwhile, a lawsuit filed in May by famous TCPA litigant Craig Cunningham against Corporate Bailout and Mark D Guidubaldi & Associates LLC went unanswered, according to court records. Cunningham, who alleged violations of telemarketing laws, filed for a default judgment against Corporate Bailout on September 12th.

Taking Advantage

Both Yellowstone Capital and Everest would not comment on the lawsuit they filed, citing pending litigation. Sources close to them, however, contend that both companies take matters that involve merchants being taken advantage of very seriously.

“When our own ISOs work directly in concert with companies that induce merchants to breach our contracts, that’s a problem,” said one source who did not wish to be named and was speaking generally about the recent introduction of debt relief service companies to the industry. “They’re taking advantage of businesses that can’t afford to be taken advantage of.”

An email sent by AltFinanceDaily to Mark Mancino early Thursday afternoon, an individually-named defendant alleged to be affiliated with the other defendants, has not yet received a response. This story may be updated if a reply is received.

A COPY OF THE COMPLAINT CAN BE VIEWED HERE.

LeaseQ and ARF Financial Partner to Automate Hospitality Equipment Financing

September 12, 2017BOSTON (Sept. 12, 2017) – LeaseQ, an online marketplace connecting business owners, equipment sellers, and lenders to make selling and financing equipment fast and easy, today announced a national partnership with ARF Financial, the only FDIC-compliant financial lender that provides short-term, unsecured business loans and lines of credit for restaurant/hospitality business owners and retailers nationwide.

“We are unique in having our own sales organization, and LeaseQ gives our loan consultants around the country a lease product with instant quotes,” ARF Financial CEO Steve Glenn said. “Now we are a one stop lender offering additional products to satisfy our customers funding needs for their businesses.”

Innovations in the equipment finance industry will continue to increase flexibility and convenience for customers, according to the Equipment Leasing and Finance Association’s (ELFA) Top 10 Equipment Acquisition Trends for 2017. Automation fuels advances in instant quotes, soft credit pulls, same-day approvals, one-day funding and blockchain for secure, multi-party transactions – many of which are available today through LeaseQ and ARF Financial.

“You can finance a car in an hour, but not a walk-in freezer to start or expand a restaurant,” said Vernon Tirey, co-founder and CEO of LeaseQ. “One-day funding is a trendy thing to say in equipment financing, but when the restauranteur or hotel manager presses the button to get financing, it has to work. We’re advancing our technology and partnering with lenders like ARF Financial who understand the value of automation to make it happen.”

LeaseQ and ARF Financial offer automated, flexible equipment financing for hospitality merchants who are frustrated with the time it takes to get a bank loan, or who cannot get a bank loan at all, including those:

- Expanding a facility

- Upgrading equipment

- Adding a location and renovating the property

- Managing working capital, and more

There are currently 150 lenders on the LeaseQ platform serving 28 vertical markets. Learn more at www.leaseq.com.

About LeaseQ

LeaseQ is an online marketplace connecting businesses, equipment sellers, and equipment finance companies to make selling and financing equipment fast and easy. The LeaseQ platform is a free, cloud-based SaaS solution with a suite of on-demand software and data solutions for the equipment leasing industry. LeaseQ provides business process optimization (BPO) and information services that streamline the purchase and financing of business equipment across a broad array of vertical industry segments. Learn more at www.leaseq.com.

About ARF Financial

ARF Financial LLC is a California licensed lender that sources short-term business loans and lines of credit for restaurant/hospitality and retail merchants nationwide. Since 2001, ARF has filled the void between traditional bank financing and less attractive venues of obtaining capital, giving merchants the ability to maintain control of their business, be more profitable and meet their financial goals. The company is managed and staffed by industry veterans with extensive experience in restaurant finance and small to medium retail industries.

For more information on their services, visit their website at www.arffinancial.com. You may fill out their contact form at www.arffinancial.com/contact, call 1-866-702-4430, or send an email to funding@arffinancial.com for inquiries.

Revisiting Funding Circle

July 21, 2017Funding Circle’s SME Income Fund delivered profits last year not only in the UK segment, but also in the US segment, according to sources. As the UK is Funding Circle’s home market, it naturally generated more revenue from it, but the margins were actually a lot higher in the US. The Fund’s 12-month calendar year ended on March 31st. The performance doesn’t reflect Funding Circle’s operations as a whole, just the publicly traded fund used to make loans through the company’s platform.

The fund’s Net Asset Value has reached £164.8M, Peer2Peer Finance News reported. Investors received dividends equal to 6.5 pence per share over the last year.

Funding Circle the company, has not filed its year-end 2016 financials yet. As a private limited company in the UK, they’re still a couple months away from the deadline to do so. In 2015, they lost £18M on £23.8M in revenue, which they attributed to their growth strategy.

Unlike with Lending Club and Prosper, anyone investing in a Funding Circle loan in the US must be accredited. Funding Circle Securities is the affiliated broker–dealer of Funding Circle USA. Lending Club and Prosper have a special arrangement with the SEC to work with retail investors. As part of that, every single loan on their platforms must be filed with the SEC as an individual security complete with a full prospectus.

Earlier this month, Funding Circle hired a new Global CFO, Sean Glithero, who was previously the CFO at Auto Trader.

CAN Capital Resumes Funding

July 6, 2017

CAN Capital is back in business, thanks to a capital infusion by Varadero Capital, an alternative asset manager. Terms of the capital arrangement were not disclosed.

CAN Capital stopped funding late last year and removed several top officials after the company discovered problems in how it had reported borrower delinquencies. The discovery also resulted in CAN Capital selling off assets, letting go more than half its employees and suspending funding new deals, among other things.

Now, however, the company has a new management team and its processes have been revamped and staff retrained in anticipation of a relaunch, according to Parris Sanz, who was named chief executive in February. He was the company’s chief legal officer before taking over the helm after then-CEO Dan DeMeo was put on leave of absence.

As of today (7/6), CAN Capital has resumed funding to existing customers who are eligible for renewal. Within a month, the company plans to resume providing loans and merchant cash advance to new customers. It will have two products available in all 50 states—term loans and merchant cash advances with funding amounts from $2,500 to $150,000.

To be sure, getting back into the market after so many months will be a challenge. “I think we’re absolutely going to have to work hard, no doubt about it. In many ways, given our tenure and our experience, the restart may be easier for a company like us versus others. Based on the dynamics in the market today, I see a real opportunity and I’m excited about that,” Sanz said in an interview with DeBanked.

Since its founding in 1998, CAN Capital has issued more than $6.5 billion in loans and merchant cash advances. It’s one of the oldest alternative funding companies in existence today, and, accordingly, it shook the industry’s confidence when the company’s troubles became public late last year.

Since its founding in 1998, CAN Capital has issued more than $6.5 billion in loans and merchant cash advances. It’s one of the oldest alternative funding companies in existence today, and, accordingly, it shook the industry’s confidence when the company’s troubles became public late last year.

The new management team includes Sanz, along with Ritesh Gupta, the chief operating officer, who joined CAN Capital in 2015 and was previously the firm’s chief customer operations officer. The management team also includes Tim Wieher as chief compliance officer and general counsel; he initially joined the company in 2015 as CAN Capital’s senior compliance counsel. Ray De Palma has been named chief financial officer; he came to CAN Capital in 2016 and was previously the corporate controller. The management team does not include representatives from Varadero.

Varadero is a New York-based value-driven alternative asset manager founded in 2009 that manages approximately $1.3 billion in capital. In the past five years, Varadero has allocated more than $1 billion in capital toward specialty finance platforms in various sectors including consumer and small business lending, auto loans and commercial real estate. In 2015, for instance, Varadero participated in separate ventures with both Lending Club and LiftForward.

Varadero began working with CAN Capital as part of its efforts to pay down syndicates. Varadero bought certain assets from CAN Capital last year and provided enough funding to allow CAN Capital to recapitalize. “The recapitalization enabled us to pay off the remaining amounts owed to our previous lending syndicate and provided us with access to additional capital to resume funding operations,” Sanz says. He declined to be more specific.

“We were impressed with the overall value proposition of CAN’s offerings as evidenced by the strength of its long standing relationships, the company’s core team, sound underwriting practices, technology and the strong performance of their credit extension throughout the cycle,” said Fernando Guerrero, managing partner and chief investment officer of Varadero Capital, in a prepared statement. “We’re confident the company’s focused funding practices will allow it to serve small business customers for many years to come.”

Guerrero was not immediately available for additional comment.

DLA Piper served as legal counsel for, and Jefferies was the financial advisor to, CAN Capital, while Mayer Brown was legal counsel to Varadero Capital, L.P.

Since its troubles last year, CAN Capital had been working with restructuring firm Realization Services Inc. for assistance negotiating with creditors. It also worked with investment bank Jefferies Group LLC for advice on strategic alternatives.

Sanz declined to discuss other options CAN Capital considered, noting that the Varadero deal provides the firm the opportunity it needs to jump back into the market—this time with “tip top” operations in place.

He declined to say how many employees the firm still has, other than to say it is now “appropriately staffed.” In addition to getting rid of the prior management team, CAN Capital reduced staffing in numerous parts of its business. That includes nearly 200 positions at its office in Kennesaw, Ga, according to published reports.

The company will still be called CAN Capital. “We feel that that brand has a recognition in the market, in particular with our sales partners,” Sanz says.

CloudMyBiz and Ocrolus Announce Ground-Breaking FinTech Partnership

June 4, 2017

June 4, 2017 – CloudMyBiz, a leader in Salesforce development and implementation, is pleased to announce a new partnership with Ocrolus, an emerging innovator in bank statement review automation. The integration of the PerfectAudit API, powered by Ocrolus, into the Fundingo lending platform by CloudMyBiz, has created the industry’s first turnkey solution, revolutionizing Alternative Lending.

“For years, lenders have relied on inefficient and lengthy procedures for bank statement review, a critical part of the loan underwriting process. This is no longer the case. Combining the PerfectAudit API with our Fundingo Underwriting automation, we are taking the slowest part of the lending process and supercharging it. This partnership will have a huge impact on FinTech.” said Henry Abenaim, Founder and CEO of CloudMyBiz.

The PerfectAudit API analyzes uploaded bank statements with 99+% accuracy, replacing manual review with automation. Ocrolus technology enables lenders to review every borrower’s bank statement data automatically, regardless of whether or not the borrower provides sensitive bank login credentials. Through the partnership with CloudMyBiz, the PerfectAudit API will be integrated directly into Salesforce.

“Until we started plugging in the PerfectAudit API, even the elite, technology-driven lenders could not review every application digitally,” said Sam Bobley, Co-founder and CEO of Ocrolus. “Partnering with CloudMyBiz is a groundbreaking moment because it’s leveled the playing field, allowing lenders of all shapes and sizes to transition to a hyper-accurate loan determination process within days. CloudMyBiz takes on all the implementation work, so achieving greater accuracy and automation than firms who’ve invested millions into technology is now just a phone call away.”

About CloudMyBiz

The CloudMyBiz team, via the Fundingo suite of apps, empowers business through the Cloud and encourages streamlined collaboration between departments, clients, customers and partners. CloudMyBiz focuses on Salesforce Implementation, Migration, Integration and Development, Third Party Applications, and Custom App Development, all specializing for the lending industry.

About Ocrolus

Ocrolus is a technology company that automates the review of bank statements. The Company’s PerfectAudit platform analyzes statements from every financial institution with 99+% accuracy, generating account information, summary analytics and a comprehensive database of transactions. By replacing one of the few remaining manual underwriting procedures with hyper-accurate automation, Ocrolus strives to strengthen the FinTech ecosystem.

Contact Information:

Dennis Mikhailov

Business Development | CloudMyBiz, Inc.

P 818.732.4316 | M 818.419.7339

dennis@cloudmybiz.com

Sam Bobley

CEO, Ocrolus Inc.

o: 646.850.9090 Ext. 1

c: 516.233.4293

sbobley@ocrolus.com

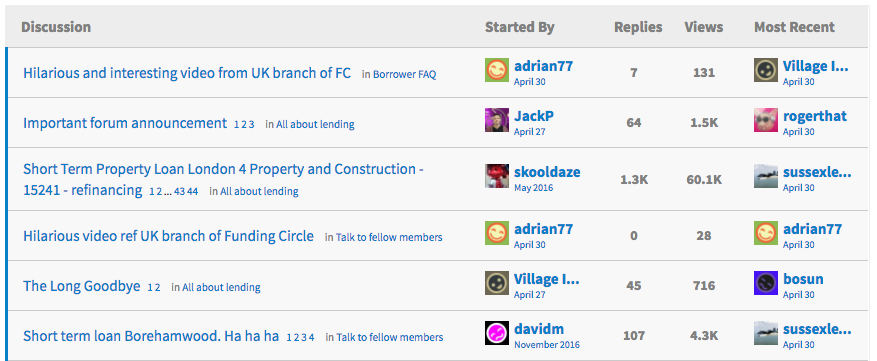

Funding Circle is Closing its Forum

May 1, 2017 One notable remaining aspect of Funding Circle’s peer-to-peer roots has been its own online forum. If you haven’t been part of that community, you’re too late, since it’s shutting down on Tuesday.

One notable remaining aspect of Funding Circle’s peer-to-peer roots has been its own online forum. If you haven’t been part of that community, you’re too late, since it’s shutting down on Tuesday.

According to a forum admin, “there has been a developing trend towards a small number of investors asking questions about a narrow range of technical topics – most of which are better dealt with through our Investor Support team. Therefore we have taken the decision to close the forum at 6pm [UK time] on Tuesday 2nd May. We hope you will all continue sharing your views on Funding Circle over on the P2P Independent Forum, which we will continue to monitor.”

One forum user jokingly theorized that the move was really about silencing investors who use the forum to complain about delinquent borrowers, going so far as to create a humorously custom-captioned movie clip.

According to P2P Finance News, a Funding Circle spokesperson said, “The closure has nothing to do with the performance of Funding Circle property development loans over the last three years which continue to outperform expectations. Investors have earned an average of seven per cent since launch and more than £22m in interest on property loans alone.”

Update 5/2: The Funding Circle Forum has officially been taken down. The URL now just redirects to a general FAQ page