The Top Small Business Lending Platform Finalists Named By LendIt

January 20, 2017The LendIt Industry Awards has named six finalists for the Top Small Business Lending Platform. They are:

- OnDeck

- Kabbage

- SmartBiz

- StreetShares

- Ascentium Capital

- iwoca

OnDeck you should know by now. They are publicly traded on the NYSE under ticker ONDK. We last sat down with them in October, shortly before they announced a $200 million credit facility with Credit Suisse.

Kabbage was one of the first online small business lenders to truly experiment with complete automation. In the last year the company has partnered with banking giants Santander and Bank of Nova Scotia.

SmartBiz ranked as the number one provider of non-Express, SBA 7(a) loans under $350,000 for fiscal year 2016. An online platform, they generated $200 million in funded SBA 7(a) loans through its bank lending partners during that period.

StreetShares has a strong focus on funding veteran small businesses. The company is also one of a very few to get approved for Reg A+ under the JOBS Act, which allows them to accept investments from unaccredited retail investors (with some limitations).

Ascentium Capital actually funded nearly $900 million to small businesses in 2016 and was acquired by PE firm Warburg Pincus just a few months ago.

iwoca is based in the UK but also operates in Germany, Spain, and Poland. They offer lines of credit to small businesses up to £100,000 with repayment terms of up to 12 months. Interest rates range from 2% to 6% per month. iwoca has raised £46 million through debt and equity.

According to LendIt, finalists for this category were awarded to the top small business lending platform based on a combination of loan performance, volume, growth, product diversity and responsiveness to stakeholders.

A similar category, the greatest Emerging Small Business Lending Platform also had six finalists. They include:

- ApplePie Capital

- Capital Float

- Credibility Capital

- Lendio

- Lendix

- Wunder Capital

More than 30 industry experts will judge and select award winners. You can view all categories, finalists and judges here.

You can also get 15% off the LendIt Conference registration with promo code: AltFinanceDaily17USA.

Brief: LendIt Brings First Fintech Awards to the Industry

November 28, 2016

Marketplace lending conference LendIt, has announced the first fintech industry awards and is inviting nominations to recognize top-performing companies and executives.

Nominations are now being accepted (closes December 21st) for 18 different categories including executive of the year, fintech woman of the year, emerging consumer lending platform and most innovative bank. The award ceremony will be held during LendIt’s 2017 conference in March.

“The lending industry is entering its 2.0 phase, after maturing in 2016,” said Peter Renton, co-founder and chairman of LendIt in a statement. “As we seek to connect the global online lending community and foster innovation and industry growth, we must recognize those that are making the biggest contributions and innovations and moving our industry forward.”

The entries will be judged by a panel of 30+ industry experts including Gilles Gade, CEO of Cross River Bank, Glenn Goldman of Credibly, and Angela Ceresnie, COO of ClimbCredit.

LendIt’s Peter Renton is Still Earning 8.72%

August 25, 2016

LendIt, speaking to LendIt USA 2016 conference in San Francisco, California, USA on April 11, 2016. (photo by Gabe Palacio)

LendIt Conference founder Peter Renton made more from his marketplace lending investments in the last twelve months than some people earn in a year just from their nine-to-five job. $54,936 to be exact, according to his latest blog post detailing his performance. That’s a result of investments on the Lending Club platform, Prosper, P2Binvestor (which requires you to be an accredited investor), the LendAcademy P2P Fund (which includes Funding Circle, Upstart, Lending Club and Prosper), and the Direct Lending Income Fund managed by Brendan Ross (which invests with lenders such as Quarterspot and IOU Financial).

Unsurprisingly, his business loan performance through the Direct Lending Income Fund has earned the highest yield, a TTM return of 12.77%.

While reporters and critics seem to be planning the funeral for several lending platforms, Renton remains steadfast in his optimism. “Eventually, I plan to have a diversified seven-figure portfolio made up of consumer, small business and real estate loans,” he wrote on his Lend Academy website.

Though Renton is reaping the benefits of being a platform investor, it’s the platforms themselves that may be in trouble, according to a recent op-ed by Todd Baker, a senior fellow at the Mossavar-Rahmani Center for Business and Government at Harvard University’s John F. Kennedy School of Government. On American Banker, Baker wrote, “Almost all [Marketplace Lending] revenue is generated from ‘gain on sale’ fees earned from new loan sales. This dependence on origination volume and gain-on-sale margins makes MPL results exquisitely sensitive to macro and micro trends in investor demand and risk appetite.”

And if a platform isn’t sustainable, the theory is that future investment opportunities may not be as available as they have been historically.

“MPLs need to shift to a more sustainable mode — either as banks or as nonbank balance-sheet lenders — before the end of the current credit cycle brings on a real shakeout and the MPL experiment becomes a financial failure,” Baker wrote.

Renton himself acknowledged a downward trend in his yield, conceding that it may never return to previous levels. “While I would love to be earning more than 10% again I don’t expect to get back there any time soon,” Renton wrote.

He also recently rebutted a Bloomberg article that argued Lending Club was being shady with repeat borrowers.

LendIt Recap: News Headlines You Need to Know

April 13, 2016

Al Goldstein of Avant speaking at the LendIt USA 2016 conference in San Francisco, CA, USA on April 11, 2016. (photo by Gabe Palacio)

As the industry wrapped up one of the biggest conferences of the year, here are some notable company announcements worth filing away:

Chicago-based online lender Avant named former UBS executive Raj Vora to lead the company’s capital raising efforts. Vora will lead strategy for its investment vehicles.

New York-based Student loan refinancer Lendkey crossed $1 billion in origination and deployment

Small business lender National Funding appointed first female president Torrie Inouye. Inouye headed data and analytics for the firm where she drove customer acquisition and underwriting.

Another millennial lender on the block raised Series A funding. New York-based online lender Pave Inc raised $8 million from Maxfield Capital that included existing investors C4 Ventures and Seer Capital. The four year old company lends unsecured personal loans to millennials.

Small business lender Streetshares won SEC approval to launch business bonds to the masses. The product will pay a fixed 5 percent interest (regardless of the performance of a particular underlying loan), is ensured by a provision fund, and provides liquidity as investors can access their funds at a 1 percent fee.

Prosper decided to end its loan sale agreement with Citi and might be in talks with Goldman Sachs. This move comes after a lukewarm reception on a batch of Prosper bonds after investors demanded as much as 5 percent points higher compared to last year.

Is Alternative Lending An Illusion? (LendIt 2015 Summary)

April 18, 2015More than 2,400 people packed into the LendIt conference last week in New York City and everywhere you turned, startups were boasting of their ability to lend billions of dollars to underserved consumers and businesses. Companies not even old enough to have attended last year’s LendIt conference had reportedly lent tens of millions or hundreds of millions of dollars already. Is it all an illusion?

Investors circled like hawks to try and grab an opportunity into this exploding market. Alternative lenders were practically being tackled by VCs, Private Equity firms, and specialty finance lenders:

Technological innovation is disrupting the status quo, attendees echoed. Surely banks can afford to develop new technology to compete, so why haven’t they? Lendio’s Brock Blake wasn’t afraid to challenge the Short Term Business Lending Panel on this. “Is there real innovation happening or is there regulatory arbitrage?” he asked.

The panelists mostly agreed that it was a combination of both. Stephen Sheinbaum, founder of Merchant Cash and Capital (MCC) and BizFi, said “regulation is not something that scares us in any way.” That’s not surprising considering MCC has survived more than ten years in business and fellow panelist CAN Capital has survived more than seventeen.

But for the newer players entirely reliant on third party brokers or dependent on a Reg D exemption to issue securities, their success may indeed be regulatory arbitrage. And time is on their side.

Karen Mills, the former head of the Small Business Administration asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

It’s the brokers that worry some folks most, an issue that PayPal and Square Capital do not have to contend with at all. OnDeck CEO Noah Breslow stated, “there is always going to be a set of customers that want to shop and want to have help.”

Kabbage’s Kathryn Petralia explained that only 2% of their business comes from brokers and their fees are capped at 4%. CAN Capital’s Jason Rockman argued that it’s about working with brokers that share their values. MCC’s Sheinbaum said, “you have to be willing to not do business with some of the unscrupulous players out there.”

But while these industry captains minimized the role that brokers play, 2015 is already being dubbed the Year of the Broker.

The regulatory environment isn’t the only issue to be worried about, skeptics argued. There was cautious alarm about the market’s viability when interest rates rise or the economy takes a turn for the worse.

“I think there’s going to be a shakeout,” said Steve Allocca of PayPal. MCC’s Sheinbaum explained that when he sees other funders doing deals that don’t appear to make sense, to not feel pressured to do them as well. “Stick to your disciplines. Stick to your guns,” he preached.

Fundation CEO Sam Graziano argued that small business lending is already very risky. The lifetime default rate on 7(a) SBA Loans is 20%, he said. Graziano, who hates the term alternative lending prefers to refer to the industry as digitally enabled lending.

And digitally enabling is something that OnDeck has focused on. In Breslow’s presentation, he said that applying offline for a loan takes 33 hours of work on average. Banks are shuttering branches at a record rate, he added.

Banks are dead, said many in attendance. Kathryn Petralia of Kabbage disagreed. “The death of banks has been greatly exaggerated,” she argued on a panel.

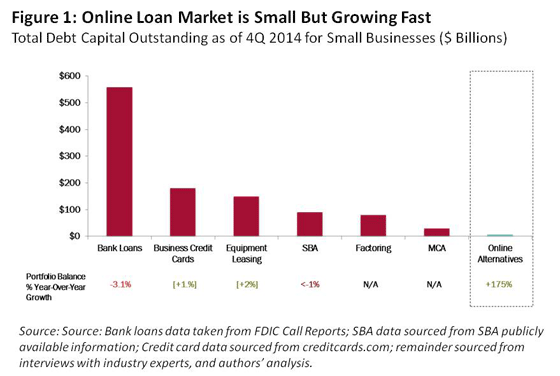

Indeed, Mills’ report shows that total outstanding debt on business loans by banks dwarfs the alternatives by more than 50 to 1.

But former U.S. Treasury Secretary Larry Summers is convinced the tide is turning.”The conventional financial sector has, in important respects, let all of its main constituents down over the last generation, and technology-based businesses have the opportunity to transform finance over the next generation,” he said during the keynote speech.

With conference sessions looking and feeling like a cramped NYC subway during rush hour, the popularity of alternative lending is no illusion.

But healthy skepticism is at least creeping in while the industry marches forward. Changes in regulations, interest rates, and economic activity will separate those simply riding a wave from those that have created something real. Expect companies that exhibited at this year’s conference to be gone by 2016 or 2017, said several panelists.

The final count of LendIt attendees was 2,493 people. 150 people who tried to register at the last minute were turned away. More are expected to attend next year.

Objectively, alternative lending appears to be very real.

LendIt Conference: The State of Alternative Business Lending

May 6, 2014 Have you heard? Banks aren’t lending. Nobody at LendIt seems to mind though. Ron Suber, the President of Prosper Marketplace, said earlier today that banks are not the competition. That’s an interesting theory to digest when contemplating the future of alternative lending. If banks are not the competition, then who is everyone at LendIt competing against? I think the obvious answer is each other, but much deeper than that, the competition is the traditional mindset of borrowers.

Have you heard? Banks aren’t lending. Nobody at LendIt seems to mind though. Ron Suber, the President of Prosper Marketplace, said earlier today that banks are not the competition. That’s an interesting theory to digest when contemplating the future of alternative lending. If banks are not the competition, then who is everyone at LendIt competing against? I think the obvious answer is each other, but much deeper than that, the competition is the traditional mindset of borrowers.

The biggest challenge the wider alternative lending industry faces is awareness and understanding. Those happen to also be two of Suber’s three edicts for growth. The third is education. Just because alternatives are available today doesn’t mean that potential borrowers know about them or feel comfortable enough to use them. Today we are competing against the old way of thinking.

Revolution?

Other products in the new “share economy” have encountered a similar struggle. Several presenters today cited Uber as having revolutionized the way people use taxis. “A long time ago, people used to stand on corners and hold out their hand to get a cab, but that’s all changed,” was the oft-paraphrased proof that age-old industries were falling like dominoes. But as a New York City resident, I hadn’t quite noticed a change at all. Hailing cabs off the street is still very much the norm. It is only by sheer coincidence that I used Uber for the very first time to travel to JFK airport on my way to this conference.

I first encountered Uber a year ago when an acquaintance dazzled me with his ability to summon a car using an app on his phone. It was then that I became aware, but I did not understand how it worked. It took me 12 months to get comfortable enough to try it myself, and the experience was okay I guess if you discount the fact that my driver went through the E-ZPass lane without actually having an E-ZPass. Needless to say, that led to a major holdup that caused me to almost miss my flight.

If it took me a year to get past the confusion of hailing a cab from my phone, I can only imagine what potential borrowers must think when told they can raise money from their peers, the crowd, or a lender that requires payments to be made every single day.

Perhaps most telling about the awareness challenge, is that many people I’ve spoken to at LendIt had never heard of a 16 year old product known as merchant cash advance. That speaks volumes about how much more work merchant cash companies still have to do in order to gain mainstream awareness.

Even those fully aware were not entirely certain about how to define the product. In the Online Lending Institutional Investors Panel, merchant cash advance was briefly discussed as a topic but it was almost entirely spoken in the context of being something that OnDeck Capital does. That would come as disheartening news to OnDeck since they have spent considerable resources in positioning themselves as anything but a merchant cash advance company. Confusion over what somebody is or isn’t will probably increase especially as alternative lenders from different industries start to compete for the same clients.

Funding businesses instead of people

Brendan Ross, the President of Direct Lending Investments, and the moderator of the Short Term Business Lending panel pointed out that a dentist could pursue two different loan options and get completely different results. With excellent credit a dentist could expect to land a 3-5 year personal loan at 7-8% APR on a P2P platform. If he were to apply for the loan using his dental practice though, he could expect to incur costs over 25% and get nothing longer than 2 years.

Ross, who was a very active moderator, subscribes to the belief that businesses are overpaying for credit. Unlike the consumer loan space, there hasn’t been price compression. The cost of business capital remains high, perhaps higher than what is necessary to turn a reasonable profit. Ross argued that the padded cost serves as a hedge against defaults and economic downturns. “The asset class works even when the collection process doesn’t,” Ross said. “The model works with no legal recovery.”

Building on that premise, Ross asked the panelists if an increase in defaults were simply the cost of doing business towards automating the underwriting process.

Stephen Sheinbaum, the CEO of Merchant Cash and Capital argued that just the opposite had occurred, that automation had led to a decrease in defaults. Others on the panel confirmed a similar outcome, though Rob Frohwein of Kabbage admitted they could potentially weather higher defaults through automation by offsetting it against decreased infrastructure costs.

Noah Breslow of OnDeck echoed something similar to Frohwein in the Small Business Term Lending Panel. He asked this question, “Do underwriters add value or not?” and followed up by saying that 30% of their deals were still manually underwritten, usually the deals that are larger.

Is full automation right around the corner?

The debate between humans and computers in risk analysis is a featured segment in the third issue of DailyFunder that is being mailed out this week, but there is another angle that is seldom discussed, whether or not customers want automation. Breslow said today that, “if customers want full automation, we are prepared to deliver it.” They’ve learned over time that “many customers want someone to talk to at some point in the transaction.” Rohit Arora, the CEO of biz2credit expressed much of the same in a recent interview with DailyFunder’s Managing Editor Michael Giusti.

The only dissenting voice was Gary Chodes, the CEO of Raiseworks who seemed to be of the belief that human involvement in underwriting was nothing short of ridiculous. He stated that, “if you look back over the last 20 years, the loss rates on business loans under 24 months has been really low.” To him, that data seemed to be proof enough that complete automation could and should be achieved, though he admitted to performing back-end checks such as landlord verifications. They currently have no physical underwriters however.

Is there a transparency problem?

Tom Green, a VP of LendingClub shared an interesting tale. While trying to convince potential borrowers to ditch a merchant cash advance in favor of a LendingClub business loan, they get pushback on the cost of their money. The reason being? Some borrowers think they’ve already got a great deal or at least a better deal than what LendingClub is offering. The problem stems from the borrower’s belief that the holdback percentage set up in their future revenue sale (the most common way a merchant cash advance is set up) is the APR.

Merchant Cash Advance Companies pay cash upfront in return for a specified amount of a businesses’s future sales. They collect these sales by withholding a percentage of each credit card transaction or bank account deposit until the agreement is satisfied in full. On a dollar for dollar basis, the cost of these programs typically range from 20%-49%, but on an APR basis, substantially higher. The holdback % is not even a factor in the APR. Green said they’ve learned that some small business owners are not sophisticated when it comes to finance.

Merchant Cash Advance Companies pay cash upfront in return for a specified amount of a businesses’s future sales. They collect these sales by withholding a percentage of each credit card transaction or bank account deposit until the agreement is satisfied in full. On a dollar for dollar basis, the cost of these programs typically range from 20%-49%, but on an APR basis, substantially higher. The holdback % is not even a factor in the APR. Green said they’ve learned that some small business owners are not sophisticated when it comes to finance.

Ethan Senturia, the co-founder of Dealstruck would probably agree. Earlier today he said, “you need to speak the borrower’s language.” Some understand APR, some don’t. “Dealstruck offers more than just APR comparisons to borrowers,” Senturia said. “Whatever helps them understand.”

When the OnDeck Capital model and merchant cash advance model were questioned as possibly being bad for borrowers, Tom Green was quick to clarify. “There are different capital needs that small businesses have,” he said. And “there is a trade-off between the length of the term and the risk.”

OnDeck Capital’s clients are not entrepreneurs born yesterday. “The typical customer has been in business for 10 years,” Breslow said. Their deals are “structured to protect through daily and weekly payments in addition to the interest rates we charge,” something he reminded everyone was “not single digits.”

Still, transparency issues remain in business lending. Sam Hodges, the Managing Director of Funding Circle explained that when he was previously a small business owner, there were hardly any lenders willing to provide him with an amortization schedule. Ashees Jain, a managing partner of Blue Elephant Capital Management admitted he would find it hard to justify the high rates of merchant cash advance if asked by a regulator, so he’d rather not invest in that market. When it comes to those types of transactions, they “don’t want to have to explain themselves” at some point in the future.

Scott Ryles, the managing member of Echelon Capital Strategies, LLC commented on OnDeck capital’s model as unbelievable. “The arbitrage is huge,” Ryles said. And Eric Thurber the managing director of Three Bridge Wealth Advisors believes that alternative business lenders are at odds with themselves. “They always talk about their risk management,” Thurber said, but he feels that players in that industry are concerned with how much market share they have. That conflicts with risk management in his opinion.

They pay or they don’t

At the end of the day Ashees Jain said as far as unsecured loans go, “borrowers pay or they don’t.” The recovery process on secured loans can be 12-18 months Jain said, a statistic cited by Brendan Ross earlier in the day.

It’s clear at LendIt that there are a lot of products available, but Ryles summed it up nicely. In the consumer space, all the volume is in the 36 month installment loans, he reckoned. For businesses it’s merchant cash advance. “It’s an awareness thing,” Ethan Senturia said in regards to getting businesses to use alternative lending sources.

It is indeed. Awareness, education, and understanding…

Fintech Nexus Files for Chapter 7

June 23, 2024 As mentioned on the Fintech Nexus blog last week, the former conference company turned fintech digital media operator is shutting down. On Friday, Lendit Conference LLC DBA Lendit DBA Lendit Fintech DBA Fintech Nexus, filed for Chapter 7 bankruptcy.

As mentioned on the Fintech Nexus blog last week, the former conference company turned fintech digital media operator is shutting down. On Friday, Lendit Conference LLC DBA Lendit DBA Lendit Fintech DBA Fintech Nexus, filed for Chapter 7 bankruptcy.

Fintech Nexus ran conferences from 2013 – 2023, originally under the name LendIt. It exited the conference business last year as part of a deal with Fintech Meetup. It then focused primarily on online news.

“The website will also remain online for at least the next few months, subject to the judgment of the Chapter 7 Bankruptcy Trustee,” the company said.

How Much Fintech News Are You Consuming On The Internet?

December 22, 2020LendIt Fintech distributed a marketing flyer via email yesterday to its subscribers and it got us thinking about how much online fintech news people are consuming, especially in this era of 2020.

LendIt reported 65,000+ monthly page views for its LendIt Fintech News and that it had 800,000+ podcast downloads.

Meanwhile, AltFinanceDaily and DailyFunder combined are recording 311,000+ in average monthly page views. Visitors are also spending 7,300 hours on our sites combined each month on average.

These figures are enormous. Thanks for reading!