Lend Us An Ear: Women in the Industry Speak Their Mind

August 11, 2016

The majority (52.5 percent) of employees in the banking and insurance industries are women — if this sounds strange, that’s because it is, considering only 1.4 percent eventually go on to become CEOs. While the male dominance is not apparent at the mid-management executive level, the sex ratio is rather skewed on top. Needless to say?

AltFinanceDaily grabbed the opportunity to speak to three women in the alternative business financing industry, charting their journey, reliving their experience, knowledge and the lessons that got them to where they are. Here are excerpts from the interviews.

Back to Roots

For some, their careers are not a deliberate choice, but a serendipitous stumble.

Heather Francis, CEO of Florida-based Elevate Funding, who went to college to become a healthcare professional entered finance by happenstance. “I went to school for health promotion and education at the University of Florida and graduated in 2007,” said Francis, who comes from a family of entrepreneurs and is a fifth generation Floridian. “I found that the position I was looking for was not a necessity for companies, it was a luxury like setting up gyms, that people were not willing to pay for at that time.”

Francis landed her first job in finance with a private equity firm called Strategic Funding in Gainesville, Florida where she set up the firm’s merchant cash advance business. After spending seven years there, in 2014, she set up Elevate Funding which in a short span of 16 months has made over 1,000 advances to businesses.

For Kabbage Loans cofounder Kathryn Petralia too, fintech was a far cry from wanting to be an English professor. A graduate from Furman University, Petralia’s tryst with finance was when she got roped into a project, valuing companies using data compression tools. Riding on building her tech expertise, she founded her first company at 25 which made store catalogues digital. “I was a kid and did not know anything about marketing or sales, so I ended up selling the startup to the company which helped me build it.” The venture however gave her an in into finance and she went on to work for Revolution Money and eventually built Kabbage Loans.

But for Danille Rivelli, VP of Sales at United Capital Source, however, the jump wasn’t as big or unusual. Although finance was not originally on her mind as an art major, it was a natural path from what she began doing to acquire real-world work experience during school, selling mortgages. Rivelli changed her academic focus and went on to get a business degree from Briarcliff College, where she also played on the softball team.

“A year or two into college, I started doing mortgages, making 5 percent commissions. It was natural and it just kinda flowed,” said Rivelli whose first job out of college was on the sales floor at Merchant Cash Capital, now Bizfi. “I wanted to get out of mortgages and I was hooked when I saw the sales floor, it was fun and upbeat.” She was also one of the company’s youngest salespeople at the time.

Women Can Do No Wrong. Or Can They?

When we asked what women need to do differently at workplaces? The answer was quick, resounding and not surprisingly – be more assertive.

“Women think from the heart more than the mind,” said Rivelli. “I find myself in situations sometimes where I know that I should be ‘leaving the emotions out of it’ so that I’m not second-guessing myself as much.” But it’s what helps her build lasting relationships with clients. “I think most effective sales people will agree that the most important part of our job is listening. You want to really know and understand who your client is and what they’re looking for before you try to sell to them.”

According to Petralia, who thinks of herself as ‘one-of-the-guys,’ the problem lies in overplaying the differences between men and women. “I think we perpetuate the stereotype that men are supposed to behave a certain way and women aren’t. I notice that when men crack a joke or use a curse word, they immediately apologize to the women in the room. We are making that happen,” she said. Petralia’s strategy in such scenarios is to swing to the other side and initiate banter. “I am very comfortable with dirty jokes and f-bombs.”

“Men are really good at faking it ’til they make it. They position themselves as experts when they are not but women are unsure of jumping into the deep end when they are not sure they can swim and that’s a big part of what we have to overcome,” Petralia said.

Francis is on the same page, “Men have no problem tooting their horn, but women don’t do that. We cannot expect anyone to stand up for us. If you think you’re getting looked over for a promotion, walk up to your boss and say it,” she said. Francis talks about most of the struggle being personal rather than operational. “I will admit to us having a need to be right… right about decisions, right in arguments and right about where the furniture goes,” she says jokingly. “A lot of what led me to start Elevate was my belief in that you could service the risky credit market without taking advantage or putting insane demands on the performance of the portfolio and still be successful… having that theory validated and accepted and in the end, being right.”

What’s the hurdle, what’s the race?

And the assertiveness comes from one’s belief in their struggle and the value of that struggle. Petralia reminisces of a time when as a scrimping 25-year-old entrepreneur, she pitched a tent and stayed on a campsite in San Francisco while raising money for her startup. Two decades later, she runs a billion dollar lending company. Petralia recognizes that not all women have the same opportunities.

“When I was raising money for Kabbage, I realized that I had only been in one or two meetings where a woman wasn’t bringing me water,” said Petralia who believes that bringing diversity requires work and companies should set targets and find qualified diverse candidates.

Kabbage allows for 12 weeks of maternity leave but that pales in comparison with other countries, says Petralia. “The problem with women is, we have the babies. Women have to choose between their careers and personal life and we are not even close to making that situation better. The key time in their 30s when they are having kids, they come back to compete with younger people who are cheaper.”

The movement to make it better, according to her should begin with creating a system of incentives like better child care, easy commute to work etc. where women don’t have to choose between advancing their career and having a child.

And her other gripe is limp handshakes from men. “Shake women’s hands better. Men give this limp, deadfish like handshake at conferences to women and it’s the worst.”

According to Francis, equal footing comes from striving for professional equality and representation. She says being a woman opens many doors but that’s where it stops. “People will talk to you nicely if you’re a woman but they don’t think you are the person making the decision. You have the ability to start the conversation but no one thinks that you can finish it.”

And for Rivelli, that means giving it your all. “The point is to keep being so good that no one can ignore you,” she said.

CommonBond Raises Equity, Debt and Acquires Personal Finance Startup, Gradible

July 19, 2016

Did someone say trouble in (online lending) paradise?

CommonBond has raised $30 million in equity, $300 million in debt and acquired a personal finance startup, Gradible.

The New York-based online student loan lender that specializes in higher education loans raised $30 million in series C equity round from new investor Neuberger Berman along with existing investors August Capital, Tribeca Venture Partners, Social Capital, Nyca Partners and Victory Park Capital. Individual investors in the round included finance veterans like former Citigroup CEO Vikram Pandit, former Thomson Reuters CEO Tom Glocer and former Barclays Private Wealth CEO Tom Kalaris.

The company plans to use the funds towards hiring folks in finance, sales and technology, building new technology platforms and scaling its loan operations. Founded by Wharton graduates David Klein, Michael Taormina, and Jessup Shean in 2012, CommonBond started as many startups do, with a founder’s problem of lack of affordable graduate student loan options. Today the company has crossed $500 million in funded loans and provides MBA loans, refinances student loans and offers personal loans.

Non-bank student loan providers make up just a sliver of the market, says CEO David Klein. “Over 99.99 percent of the student loan market is driven by the federal government and private banks and the the tiny piece of the market is made up by CommonBond and SoFi,” he said. “And as big as that sounds, relative to the largesse of the market, we don’t even make up a percent of that.”

The Gradible acquisition should answer some of that for CommonBond, giving it access to 40 million students and a network of employers. It plans to build a portal for employers who can contribute directly to their employees’ monthly student loan payments, through a student loan contribution platform similar to a 401(k) matching program.

CommonBond competes with rivals like SoFi which has made news for everything from being offensive, offering dating services, selling mortgages and its purported plans to become a bank. And CommonBond isn’t shying away from other loan products either. “Our long term vision is to provide our customers with their evolving needs and we are well positioned to provide other products and services over time.”

In terms of its lending operations, CommonBond uses a hybrid model of funding by holding half of the originated loans on its balance sheet and selling the other half on a marketplace. “To weather any storm, it’s important to diversify capital sources and we think the hybrid model will end up being the only option,” Klein said.

Looking Back & Forging Ahead: A Dialogue With David Goldin

June 23, 2016 DeBanked Magazine recently caught up with David Goldin, the founder, president and chief executive of Capify, a New York based alternative funder. Goldin, who started his business in January 2002 as a credit card processing ISO, has been an outspoken and active participant in the alternative funding space since that time. He is also president of the Small Business Finance Association, the industry trade group that he helped found in 2006. The following is an edited transcript of our discussions.

DeBanked Magazine recently caught up with David Goldin, the founder, president and chief executive of Capify, a New York based alternative funder. Goldin, who started his business in January 2002 as a credit card processing ISO, has been an outspoken and active participant in the alternative funding space since that time. He is also president of the Small Business Finance Association, the industry trade group that he helped found in 2006. The following is an edited transcript of our discussions.

DeBanked: Since you started the business, Capify has grown from a credit card processing ISO into a global company with more than 200 employees in the U.S., U.K., Canada and Australia. Please talk a little about where Capify is today and your future growth plans for the company.

The key here is responsible growth and the responsible providing of capital. Anyone can fund deals. The hard part is collecting the money back, so you have to know how to operate during a down economic cycle. Capify did it very successfully in the last economic downturn. As we move into uncertain times, it seems there’s a greater possibility that the economy is going to get worse over the next 18 months. Even so, we’re working on several new products and new partnerships that we’ll be announcing shortly. Again, the trick is to be responsible about growth. We’re staying laser focused on our business right now and being very selective about where to invest capital in new projects during these uncertain times.

DeBanked: Continuing on the subject of growth, what do you think has been the most significant contributor to the company’s upward progression over the past several years?

I think our underwriting model is what has helped us the most. Our performance data has allowed us to make decisions in tough times and automate our processes further based on historical trends. We have 10-plus-years of performance data in the U.S. and 8-plus-years overseas. Most companies have only three to five years of experience, and most importantly, they haven’t been through an economic downturn.

DeBanked: How has the competitive landscape in the industry changed in the past few years?

Lenders are a different quality now. There is more variation in lenders than ever before—from lower-risk providers of capital to higher-risk providers of capital. Higher-risk providers of capital tend to charge a lot more. They also tend to have very aggressive business practices. The public perception is that all funders are the same—but we all have different business models and ethics in the way we operate our companies. It can be challenging at times to help customers, the media, partners and investors understand the difference between Capify and less scrupulous players.

DeBanked: What do you think the industry will look like in five to 10 years?

I think you’re going to see a lot of consolidation, and I think you’re going to see a whole new variety of products being offered to customers. The customer acquisition cost is too high to only offer one type of product. Similar to banks, alternative funders are going to start offering multiple products, if they aren’t already, and that will help make for a stickier customer and increase the bottom line.

Also, there will be significantly fewer funders than there are today and many ISOs will not be able to survive. I think more and more companies are going to start building their own internal sales forces. There are lower default rates and higher renewal rates in the direct model; the ISOs don’t have skin in the game. I think some of the stronger ISOs over time will become part of the larger funding companies.

DeBanked: There seems to be a consensus in the industry that more regulation of alternative financing is inevitable. How is regulation going to change how alternative funders operate and how might it change the competitive landscape?

I think you’ll see a lot more self-regulation before you see actual regulation when it comes to business-to-business lending. Funders are taking self-regulation more seriously and there have been more associations formed to educate policy-makers about the performance rates, default rates, renewal rates, customer satisfaction levels and how the products work.

The one area there could be potential regulation is in providing capital to sole proprietorships. The argument is that tiny businesses may need more assistance than larger companies, and some make the argument that these micro businesses are quasi-consumers. We disagree. We feel that if a sole proprietor is using the capital for his business, it should be considered a business transaction. However, several factors— including rampant media attention, more publicly traded alternative financing companies, tremendous growth of marketplace lending over the past several years and an election year—provide a recipe for all the regulation noise.

DeBanked: What are the biggest risks our industry is facing right now?

We’ve seen the movie before—in 2007 and 2008—when alternative funders didn’t factor in the severity of how an economic downturn could affect their business. The risk is there again. Funders have to be even more responsible. It’s not about how much you fund, it’s about much you collect back. You can’t be super-aggressive during times you think you may be

going into a down period. There could be significant industrywide fallout from irresponsible underwriting.

DeBanked: What advice would you give to new funders entering the market now?

I think the boat has left the dock; I don’t think they will be able to compete with established players in a meaningful way. Someone who really wants to be in the business should look at acquiring several small to medium-sized companies and rolling them up to get scale. It would be very challenging and require many years of investment to start from scratch at this point to build a substantial company. It’s harder now than it was in the past.

DeBanked: Can you talk a little about where you see the future of banks and alternative funders and how they will work together?

I think some banks will want to acquire platforms for speed to market or partner with platforms where the banks provide the capital and the funders service the loans. The latter is the model that J.P. Morgan and On Deck chose. The challenge is that the banks aren’t going to want to take a risk on applicants that don’t fall within the certain credit profile that they are comfortable lending to. While the partnership model will help banks make decisions faster about lending to small businesses, many small businesses will continue to be underserved. This could, in turn, provide an opening for independent funders who are willing to provide capital, albeit at higher rates because you can’t make a profit providing working capital (typically unsecured) at bank rates to the credit and risk profiles of businesses that most alternative funding companies work with today.

DeBanked: Please address the major technology trends shaping the alternative financing industry and what this means for industry players?

My opinion is the technology is ahead of the typical business brick-and-mortar business owner. Whilethe technology exists for business owners to go to a website and provide their personal and business data, we have found most business owners want to speak with a salesperson first, get a comfortable level and then apply online. (Compared with going right to a website and applying without a human involved). However, each year that goes by more and more business owners get more comfortable with technology and a greater percentage of them will look for a completely online experience. Being that it costs millions of dollars and years of time to build these platforms, you have to constantly evolve your platform to stay relevant. You can’t just snap your fingers and have it up and running.

I think the trend for our specific industry is being technology-enabled rather than being pure-bred tech companies. Customers still want to speak to people,but you also have to have viable backend technology so your business is scalable. Technology, such as digital bank statement transmission via various platforms, also helps cut down fraud compared with reviewing manual documents that can easily be forged or “Photoshopped.”

DeBanked: How can alternative funding companies best meet the challenges they are likely to face over the next few years?

I think alternative funders need to focus on more responsible providing of capital. This means really focusing on business owners’ ability to repay, taking a hard look at overburdening them with debt through stacking, for example, and further evaluating the referral sources of business they are getting their deal flow from in order to ensure that business owners get the best possible experience. Furthermore, I think as more alternative funding companies focus more on profitability and not just growth, coupled with the tightening of available institutional capital with an appetite for our industry, you will see some of the recent trends potentially reverse such as extremely high approval rates and industry margin compression.

‘We Serve a Fragmented Market That is Ripe for Disruption,’ says Patch of Land CEO

June 3, 2016$484 million: That’s how much real estate crowdfunding platforms attracted in 2015, which was three times of that the previous year. There are an estimated 125 such portals and the new SEC rule which allows non accredited investors some leniency to invest in these projects. To demystify real estate crowdfunding, AltFinanceDaily spoke to Patch of Land’s CEO Paul Deitch to unravel the concept, measure the momentum of investor interest and the regulatory environment. Here are excerpts from the interview.

What’s on the horizon for Patch of Land this year?

Now that Patch of Land’s model is proven, we will be adding complimentary products for the real estate entrepreneur and investor, accompanied by a broadening of funding strategies. For example, we recently launched the new midterm loan product that addresses the opportunity in the $4 trillion single-family rental space.

How is the investment momentum different from that in ‘08-’09?

One of the biggest changes between then and now has been the enactment of the JOBS Act, which actually came about as a result of investment conditions in ‘08-’09. Peer-to-peer lending came into existence during the 2008 Recession when consumers and small businesses could not rely on banks for their funding needs. In 2012, President Obama signed a historic bill called the JOBS Act (Jumpstart Our Business Startups Act), allowing companies to raise working capital in the form of debt and equity via a crowdfunding model. When the SEC implemented Title II of the JOBS Act in 2013 it allowed companies to publicly solicit, via Internet marketing, their equity and debt offerings; private placements could now be advertised. Marketplace lending is an evolution of peer-to-peer lending, defined by the participation of traditional financial institutions purchasing the loans being issued by P2P lenders.

Whom do you consider your competition in the industry and how do you differentiate yourself from them?

We approach the competition question from a different perspective. One would think that other online lenders or real estate crowdfunding companies are our competition but they are not. We are all working towards creating more efficiency, transparency and access to real estate and investments. The market that Patch of Land is serving is fragmented, locally delivered, and highly manual — it is ripe for disruption. Banks are exiting the space due to capital and liquidity constraints and hard money lenders are limited by a single source of capital and local footprint. Unlike these offline incumbents, Patch of Land has a national footprint, and uses proprietary software to quickly and reliably make first lien position loans, pre-fund those loans, and then crowdfund the financing from thousands of investors (both individuals and institutions) on a fractional or whole loan basis.

Who regulates P2RE? And what are the challenges there?

P2RE and the real estate crowdfunding sector is regulated by the SEC. Patch of Land operates under Title II, Regulation D, Rule 506(c) whereby we can only accept investments from accredited investors, as defined by the SEC. This is a strict regulation that requires thorough diligence and vetting of the accredited status of the investor. The biggest challenge we face is that we have many retail investors who want to invest with us and we cannot accommodate them.

How are the ripples in the capital markets affected or will affect business?

Capital markets volatility has not had an adverse effect on our business. Our capital sources are very diversified and are not dependent on large capital market players. Over 90 percent of our loan volume has been, and continues to be, funded by crowd capital. We have on-boarded multiple institutions of various sizes that buy loans on a fractional basis, in addition to the whole-loan forward flow agreements in place.

How is crowdfunding for real estate different from marketplace lending specifically?

Crowdfunding for real estate, specifically when referencing debt, is a subset of marketplace lending. Patch of Land is a ‘real estate marketplace lender’ because we focus specifically and exclusively on debt and do not offer any equity projects for funding. Equity deals are crowdfunding deals, not marketplace lending deals. Therefore, a real estate marketplace lender that transacts with individual investors can be considered a crowdfunding platform, and a crowdfunding platform that does not transact in debt is not a marketplace lender. Two other elements that differentiate crowdfunding from marketplace lending are: 1) prefunding, where the platform fully funds the loans upfront and therefore is not engaging in crowdfunding that usually involves raising capital first, before disbursing it to the sponsor/borrower; 2) marketplace lending includes institutional and individual investors who participate in loan purchases, whereas a crowdfunding model is focused exclusively on individual investors.

How is crowdfunding poised to change real estate investing?

Traditional real estate (debt or equity) can be highly time consuming. We offer an alternative to have real estate debt as part of a portfolio, bringing both new and experienced investors all the data they need to make a decision. Most would never have the time to aggregate this much data on their own, through traditional methods. Crowdfunding allows capital to flow more easily to across the nation, rather than locally, to places and projects that might have been shut out or simply left behind because they were too difficult to assess, evaluate and understand, or were the purview only of local investors and gatekeepers “in the know”. Crowdfunding puts investors in the driver’s seat, giving them the power to pick and choose investments that meet their personal risk/return needs. It allows for investment strategies that are both more “bespoke,” and yet more diversified -both in the way of product type and geographies, all through fractional investments across a technology enabled, online platform. Investors not only have broader choices of where to invest, but they can do it from their mobile phones in seconds.

Lending Club Faces Pressure to Redeem An Entire Industry

May 15, 2016

In the wee early morning hours of May 3rd, I finally wrapped up the latest AltFinanceDaily story and hit the publish button. Then as I made my way off to bed, I started to second guess the headline. Titled, Is The Marketplace Lending Apocalypse Upon Us?, I fretted over whether or not it was overly sensational.

Apocalypse. Apocalypse. Apocalypse, I repeated over and over in my head.

As I tossed and turned for an hour, I worried that thousands of readers would think AltFinanceDaily was crossing over into tabloid territory. I decided to leave it up anyway, certain enough at least that the clouds forming over the horizon signaled the arrival of a dark storm.

Less than a week later, Lending Club’s famous CEO would resign in disgrace in a scandal that also brought down several other employees. The company would delay its quarterly earnings report and the stock would drop by more than 50% over the course of just a few days. Closely related companies like OnDeck would be dragged down by the news, Wall Street banks would announce suspensions of securitizations, and community banks would halt the purchases of Lending Club loans. Blackstone Group would end its planned foray into online lending and banks like Wells Fargo, smelling blood in the water, would strike at the heart of some marketplace lenders by announcing a new technology-enabled product.

Reporters from all types of media outlets would contact me to ask what I thought of it all and I spoke from my gut in some of them.

Little details would trickle out, such as a whistle-blower submission to the SEC last July over Lending Club’s disclosure practices and another board member’s stake in a little known company named Cirrix Capital would be called into question. The non-stop fearmongering headlines from the media definitely didn’t help.

Lending Club’s complete silence after Monday morning’s announcement only made it worse. Those who buy notes on their platform never received a single communication about it, a fact that might be entirely related to quiet period rules surrounding the release of quarterly earnings. For some platform users, that continued silence fed into even the most rational investors’ worst fears.

On the LendAcademy forum for example, some users argued that Lending Club could be facing bankruptcy before the end of the year. Many who were more calm but still concerned, indeed said they were refraining from purchasing new notes until they got further guidance just to be safe. Others ventured off into complete paranoia while rational minds tried to reel them back to reality. As someone who has a significant Lending Club portfolio, I found myself shifting back and forth between those roles.

Everything is fine. Or is it?! No, everything should be fine. BUT WHAT IF IT’S NOT?!!

On Monday, In what will be a semi-post-apocalyptic world, Lending Club will have a lotta ‘splainin to do. New CEO Scott Sanborn will be tasked with restoring order to the world of marketplace lending. His predecessor, Renaud Laplanche, was the face of peer-to-peer finance. He was an icon. As the four-time keynote speaker of LendIt, Laplanche’s persona assured a skeptical public that disruption in lending was true Silicon Valley innovation, not Wall Street engineering. This lending marketplace could not possibly be risky, one might have supposed, because it looked so charmingly French. The intellectual in the red vest with a degree from école des Hautes Etudes Commerciales de Paris did not look and sound like Dick Fuld from New York City. And yet Lending Club’s offense that led to Laplanche’s departure, opened it up to comparison to the shoddy mortgage origination market in the early 2000s that led to Lehman Brothers’ collapse and the Great Recession.

This week, Scott Sanborn will have to make a most convincing argument to restore belief in the movement. Regulators, legislators, investors, and borrowers alike, have pegged at least some of their perceptions surrounding fintech to Lending Club. What happens this week may very well decide the future of online lending altogether. For Sanborn, those are some very big shoes to fill, or in Lending Club’s case, it will all depend on how good he looks in his red vest.

Autres temps, autres mœurs

Godspeed.

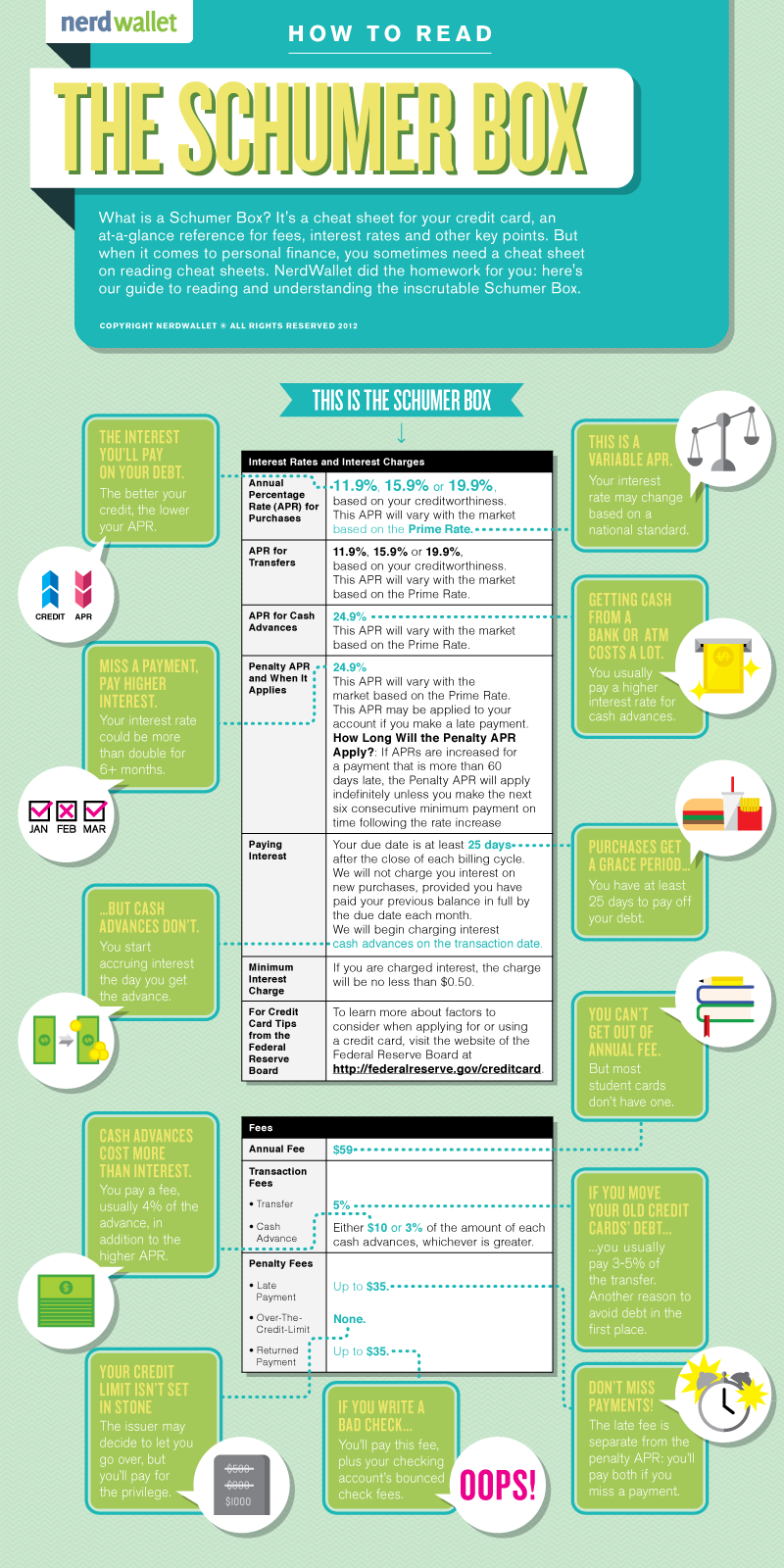

Online Lending APR ‘SMART Box’ To Apply To Loans, Not Merchant Cash Advances

May 5, 2016

OnDeck, Kabbage and CAN Capital have launched an initiative to make online loan shopping easier. Dubbed the SMART (Straightforward Metrics Around Rate and Total Cost) Box, these lenders plan to present small businesses “with a chart of standardized pricing comparison tools and explanations, including various total dollar cost and annual percentage rate metrics that enable a comprehensive pricing comparison of loans of equivalent duration.”

The Box, clearly meant to increase transparency, was explained in an ironically confusing way, particularly where it said it would include annual percentage rate metrics. An Annual Percentage Rate (APR) is indeed a representation of several metrics and thus it wasn’t clear if the Box would just include some of these individual metrics and conveniently leave out the APR itself.

OnDeck CEO Noah Breslow for example told Forbes only six months ago that annual terms don’t make sense. “The APR overstates the actual cost of the loan to the borrower,” he said. He was not alone in thinking that way. Several studies have concluded too that merchants don’t always even know what APR represents. Lendio for example, found that two-thirds of small businesses selected the total dollar cost of a loan as the easiest to understand. Only 17.4% said the APR was the easiest.

And there’s another thing, the fact that CAN doesn’t just do loans, they also do a significant amount of merchant cash advances. What role could an APR have there? While the Box’s final system won’t be decided until after the conclusion of a 90-day national engagement period that begins next month, one can only imagine that it might have a Schumer Boxer feel to it.

A Schumer Box explained:

Via: NerdWallet

The syntactic ambiguity in the announcement however was unintentional. A spokesperson for the group (Known as the Innovative Lending Platform Association) said that the SMART Box will indeed include Annual Percentage Rates.

But that’s where loans are concerned…

When AltFinanceDaily asked about merchant cash advances, Daniel Gorfine, vice president and associate general counsel of OnDeck; Parris Sanz, Chief Legal Officer of CAN Capital and Azba Habib, assistant general counsel of Kabbage, submitted the following joint response:

“As part of the SMART Box initiative, we are interested in engaging with providers of MCA products. Based on consistent assumptions about a small business’s future sales volumes and its ability to deliver the contracted amount of receivables within the period of time estimated during underwriting, the SMART Box could apply to MCA products.”

So long as SMART Box disclosure is voluntary, an MCA company could perhaps employ their own version of it. It just might come sans APR given the product’s history with state regulations. The Association is emphatic however that this concept could be used by MCA companies and others in the small business financing space. After all, the initiative is rooted in transparency for the small business owner, they say.

In September, the Association “will encourage those interested in promoting the responsible development of the small business lending industry to voluntarily adopt or support the model disclosure.”

Given the level of influence these companies have on the industry, the voluntary nature of the SMART Box has the potential to spark an industry-wide box revolution. MCA companies however would need to structure transparent disclosure around their contractual frameworks. But even that could be a good thing. One commercial financing broker for example, posted a redacted service fee agreement to the DailyFunder forum earlier this week that purported to show another broker trying to charge a merchant a 26% premium (26% of the funding amount) for their work. Despite this unusually high cost, the charge itself was hard to find, hidden among fine print on an otherwise benign looking page. Naturally, others in the industry did not respond kindly to it. Even other brokers referred to it as “outrageous,” “nonsense,” or “bs.”

Their reactions make clear that there is a desire for transparency even among the group most often blamed for the lack thereof. Some of the industry’s forward thinkers have told AltFinanceDaily that a system like a SMART Box is the future of the industry whether one agrees with it or not. And if not for the sake of small businesses and regulators, then for the sake of being able to compete fairly against companies that may be relying on truly hidden fees.

SMART Box. All aboard the transparency train?

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”

Is That a Bird, a Plane or a Recession in the Wings?

April 26, 2016

The R-word has been rearing its ugly head with more frequency in recent months, propelled by falling stock prices, higher borrowing rates and the dollar’s ascent.

While a recession—typically defined as a fall in GDP in two consecutive quarters—is far from certain, it would most definitely be a double whammy for an industry that many believe is already ripe for a pullback due to multiple years of unfettered growth. Indeed, many funders have experienced great success riding on the coattails of the long-running favorable market. Some industry participants fear these funders are masking loss rates behind strong volume—a particularly problematic strategy if the volume were to taper off due to an economic downturn.

“It’s no different than what happened in the housing market in 2008,” says Andrew Reiser, chairman and chief executive of Strategic Funding Source Inc. in New York. If and when a recession occurs, several industry participants expect there will be a culling of the weakest firms. They say inexperienced and less-diverse funding companies are particularly at risk, as are MCA funders that don’t keep close tabs on their business dealings. They also believe that venture capital funding will be even harder to come by and regulation will rain down more heavily on the industry.

RISK FACTORS THAT SPELL TROUBLE IN RECESSIONARY ENVIRONMENT

For a variety of reasons, Glenn Goldman, chief executive of Credibly, a New York-based small business lending platform, believes that fewer than 50 percent of the funders today are prepared to weather a recession. Many don’t have strong data science and risk management, for example. Some newer platforms also don’t have the seasoned management to help guide them appropriately, he says.

Another red flag is when funders rely too heavily on a single source of funding. Goldman points back to 2008 when the commercial paper market disappeared. Companies that had on balance-sheet funding capacity were able to weather that storm because they weren’t exclusively relying on commercial paper or securitization, he says.

Goldman believes the prudent way to manage an alternative funding business is to utilize a combination of on-balance sheet financing, whole loan sales and securitization. “If the market moves sideways and you rely only on a single source of funding, you are at risk. It’s an incredibly obvious statement, but it becomes more acute when the economic environment comes under pressure,” he says.

Notably, there are very few sizable alternative funders who successfully survived the last big recession, meaning there are hundreds of companies now doing business in this space that don’t have years-worth of data to help them make more prudent underwriting decisions. Strategic Funding, for example, had the highest loss rate in its history in the third quarter of 2008 and has used its wealth of data to learn from past mistakes. “There’s no doubt that it is critical to be able to correlate events with history,” Reiser says.

Funders are also going to have to batten down the hatches when it comes to their underwriting standards. “Just because someone paid you back yesterday doesn’t mean he’s going to pay you back tomorrow,” Reiser says. “You have to be right more often in a recessionary environment.” Indeed, liquidity for originators and investors will become even more critical in a recession.

“Liquidity is king,” says David Snitkof, chief analytics officer and co-founder of Orchard Platform, a New York-based technology and data provider for marketplace lending. He points out the large number of companies that went belly-up in the last big recession for lack of liquidity. “The more that participants in this market are able to diversify their capital structure, diversify their funding sources and work with multiple providers, the better off they will be,” he says.

Another challenge will be for funders that haven’t had their servicing and collection capabilities adequately stress tested, Snitkof says. These firms should consider working with an outside provider to help them scale their collections as necessary. In this way, a company that needs additional resources can scale up pretty quickly without disrupting operations.

THE P2P OUTLOOK

To be sure, all types of companies fall under the alternative funding umbrella and each will have its own special challenges in a recession. In the P2P space, for example, having a diverse investor base and a sound credit model will become increasingly important. Peter Renton, an investor and founder of Lend Academy, an educational resource for the peer-to-peer lending industry, predicts that some of the newer P2P platforms will struggle more in a recession. That’s because they haven’t had as much time to accumulate and interpret borrower data and adapt their models accordingly.

To be sure, all types of companies fall under the alternative funding umbrella and each will have its own special challenges in a recession. In the P2P space, for example, having a diverse investor base and a sound credit model will become increasingly important. Peter Renton, an investor and founder of Lend Academy, an educational resource for the peer-to-peer lending industry, predicts that some of the newer P2P platforms will struggle more in a recession. That’s because they haven’t had as much time to accumulate and interpret borrower data and adapt their models accordingly.

Lending Club, for example, has gone through many iterations of its credit model over its multiple years in business, and it’s much better than it was even five years ago, says Renton, who had around $37,000 invested with Lending Club as of the third quarter of 2015. “The best data that anyone can get is payment history with your existing borrowing base,” he says.

Particularly in a recession, P2P players need to be extra careful about maintaining strict underwriting standards. Marketplaces may have to tighten their borrowing standards to lend to more solid companies, so the likelihood of defaults isn’t as great. So, for instance, if their standard was once borrowers with a FICO score of at least 640, they could up it to 660, Renton says.

Platforms also have to make sure they have enough investors to satisfy their borrowers, which is why having a diverse investor base is so important. In a recession if you have three hedge funds and that’s your entire investor base, they could all go away. By contrast, if a platform has five thousand individual investors, they aren’t all going away. You may lose 10 percent or 20 percent of them, but if you still have four thousand investors, you can still have your loans funded, Renton explains.

One way to do well even in a recessionary environment is for P2P players to tweak their credit model to be more restrictive so their default rates are lower. “If your default rates are only 3 percent and your competitors are at 6 percent, you’re going to get more business,” Renton says.

Certainly, alternative funding companies can get into trouble if they don’t act early enough when they see a change in activity and economic performance, says Ron Suber, president of Prosper Marketplace, a P2P lender based in San Francisco. Funders need to be able to nimbly adjust their pricing, risk models and expected default rates as needed. “Every marketplace will see a change in borrower behavior as unemployment increases and there are economic declines. Therein lies the question: what does the marketplace do?” Prosper, for instance, recently raised rates on loans, telling investors it had increased its estimated loan loss rates and therefore was updating the price of loans to reflect increased risk. Understanding risk and pricing loans accordingly is always important, but even more so in a shaky economic environment. “You always have to stay on top of it,” Suber says.

MANY MCA FUNDERS AT HIGH-RISK IN RECESSION

MANY MCA FUNDERS AT HIGH-RISK IN RECESSION

If a recession strikes, some observers believe the risk to certain MCA funders will be particularly acute. That’s because new players have entered the MCA space over the past several years, and a sizable number of them don’t have a good handle on their business. Higher default rates could force many of them to shutter operations. Certainly merchants especially those with bad credit—will need more access to capital during a recession and MCA is a natural place for these businesses to turn. But MCA funders have to do a better job of adjusting for risk and keeping adequate records if they hope to weather an economic downturn, says Yoel Wagschal, a certified public accountant in Monroe, New York, who has worked with a number of struggling MCA funders. “A small recession could lead to big failures if you don’t take the right steps,” he says.

To avoid business-threatening issues, Wagschal recommends that MCA funders take steps now to develop stronger underwriting systems to vet merchants better. He believes it’s more prudent to do fewer deals with higher rated merchants than to continue taking on risky businesses as customers. If they see more defaults are coming in, funders should also consider raising their factor rates, he says. Another option is to halt new funding for three to four months to re-energize the business. “It’s much harder to make money than to lose money,” he notes.

If they don’t already have them—and many don’t—MCA funders also need to invest in a good accounting system that can flag their profits, losses and defaults on a real-time basis. This information allows funders to make swift decisions about the business so they can take necessary steps at the right time, he says. “You don’t wait for months, or year end, to analyze all the facts. You might have already lost your business and lost your money because money is just turning around so quickly.”

UNCERTAINTY ABOUNDS FOR VENTURE CAPITAL INVESTMENT

Existing funders won’t be the only ones to struggle in a recession; the well of venture capital funding for new entrants could easily dry up as well,like it did in the last big recession. That’s not to say VC firms will lose interest entirely, but new funders will have to work even harder to get noticed. “There are so many originators, for any new entrants, the bar gets higher and higher to prove that you have something truly unique,” says Snitkof of Orchard Platform. Reiser of Strategic Funding already sees this scenario playing out. “I don’t think the market [lately] has been very favorable to our space,” he says, noting the dearth of exit strategies that have made it riskier for VC firms to invest. “It’s always easy to get in; it’s hard to get out,” he says.

GET READY FOR MORE REGULATORY ACTION

Industry watchers also believe the alternative funding industry will become more heavily regulated in a recession and its aftermath.

Reiser points to all the additional restrictions placed on the mortgage industry in the wake of the housing market bust in 2008. At a time when the housing market was restricting, you had more compliance placed on it as well. “I think you’ll have more compliance in our industry too. That’s just another cost that will have to be absorbed,” Reiser says.

In a recession, there’s more likelihood that harm can come to customers and that will drive regulatory action as well, he adds.

THE ART OF MAKING TOUGH DECISIONS

If the economy turns south, many alternative funders will be forced to make tough underwriting decisions. It can be hard if your analysis of data tells you that things are going to turn downward and your competitors don’t take the same stance, says Stephen Sheinbaum, founder of Bizfi, a New York-based online marketplace.

In that case, funders have to decide whether they are willing “to tighten and pivot while the rest of the players in the space are going full steam ahead,” he says. “That’s where you have to have some conviction and trust your data and do the right thing.”

Of course, even as the rest of the economy is faltering, recessionary times can also be a boon for enterprising companies. For example, the 2008 recession turned out to be positive for Bizfi, which at the time was called Merchant Cash and Capital. Using housing starts, consumer spending and other data, the company correctly predicted the economy was going to take a severe turn downward. It therefore made tweaks to its underwriting guidelines, moving into certain industries and away from others it deemed riskier. “Change can be hard, but it can be for the better,” Sheinbaum says.

Indeed, alternative funders that embrace new opportunities can be successful even in a broad economic downturn. “It’s about having the foresight to be able to discern good from bad and just being really disciplined about it,” says Snitkof of Orchard Platform.