Mel Chasen, Founder of Rewards Network and a Merchant Cash Advance Visionary, Has Died

March 15, 2017 Melvin Chasen passed away on Monday. He was 88. Chasen founded Rewards Network in 1984 as Transmedia Network, Inc. and it went on to become the world’s largest dining rewards program. As part of that, the company pioneered the use of future sales to facilitate working capital to restaurants.

Melvin Chasen passed away on Monday. He was 88. Chasen founded Rewards Network in 1984 as Transmedia Network, Inc. and it went on to become the world’s largest dining rewards program. As part of that, the company pioneered the use of future sales to facilitate working capital to restaurants.

Transmedia became iDine Rewards Network in 2002 but was later shortened to just Rewards Network in 2003. While Chasen had an incredibly accomplished career, a newspaper obituary paying tribute to his life says that Transmedia, a specialized restaurant financing company, was his biggest business success.

A 1991 New York Times article explained the business model as follows: “It gives the restaurant $10,000, a debt that is paid off by providing $20,000 worth of meals to Transmedia customers. The customers pay Transmedia $15,000, a 25 percent discount from face value. If the restaurant goes out of business before Transmedia’s customers eat enough meals, or if customers do not patronize a restaurant, Transmedia suffers the loss.”

To think that concept was not only being applied 26 years ago, but was already a big hit, undoubtedly makes Chasen a top player in merchant cash advance lore. He will be greatly missed.

A service will be held on Thursday, March 16 in North Miami Beach. Memorial donations may be made to the ALS Recovery Fund.

In Canada, Alternative Business Finance Industry Similar, Yet Different

March 8, 2017 David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

“We don’t view ourselves as directly competing with banks,” Gens says, suggesting that his target market is less than prime. It’s a point that his counterparts in the US have made often. But there’s a slight difference with that approach in their market, he adds. “Most Canadian consumers are prime.” And unlike the US, the banks are not necessarily portrayed as the enemy in Canada where five major ones dominate the market.

“It’s exceptionally difficult for an alternative small business lender to build a brand,” said Jeff Mitelman, CEO of Montreal-based Thinking Capital, on a panel at the LendIt Conference. Despite that, his company has funded half a billion dollars to 15,000 unique businesses over the last 10 years. A panelist besides him half-joked however, that there is such an inherent conservatism with Canadian small business owners that some don’t even want to grow and are content with running lifestyle businesses.

But of the deals that are getting done, they’re often acquired through direct marketing. “The ISO market is not like it is in the US,” Gens says. “There’s just a handful of them.” Where there are ISOs though, competitive pressures usually follow. He says that they’re competing on at least 50% of the deals they work on, in part because of these ISOs. Stacking is happening in Canada too, he admits. “It’s not as crazy as it is in the states,” he contends. “Philosophically, it doesn’t align with our business.”

Some deals in Canada are actually being facilitated by US ISOs, he acknowledges, before clarifying that they should be aware that they will get paid in Canadian dollars, which at present are worth about a three quarters of an American dollar. They are in a different country after all.

Gens and others like Bruce Marshall, vice president of British Columbia-based Company Capital, agree that OnDeck’s push into Canada has been good for the entire industry. Six months ago, Marshall said, “We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising. These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails.”

Over time, they believe alternatives will become more mainstream. For Gens, part of that is about doing right by the customer. “We pride ourselves on being very transparent,” he says. There are no hidden fees with their products and they can make things easy like use APIs to access a merchant’s bank statement history, provided an applicant wants to do it that way. “More than 50% of merchants are still submitting bank statements,” he says. That trend is still pretty much true in the US as well. “There’s a much lower incidence of fraud in Canada,” he asserts. It’s a nation of small businesses he’s content to serve.

I Got Funded, OMG I’m a Merchant!

March 3, 2017 I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced AltFinanceDaily’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, AltFinanceDaily is truly a small business first.

I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced AltFinanceDaily’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, AltFinanceDaily is truly a small business first.

Independently owned, there are no investors in the company to turn to for assistance. And that’s not such a bad thing if you know at all what it can be like to have partners. At the end of last year, we did what hundreds of thousands of small businesses around the country have done, we got funded by a marketplace lender. Through that experience, I found myself wearing a brand new hat, one that says “merchant” on it.

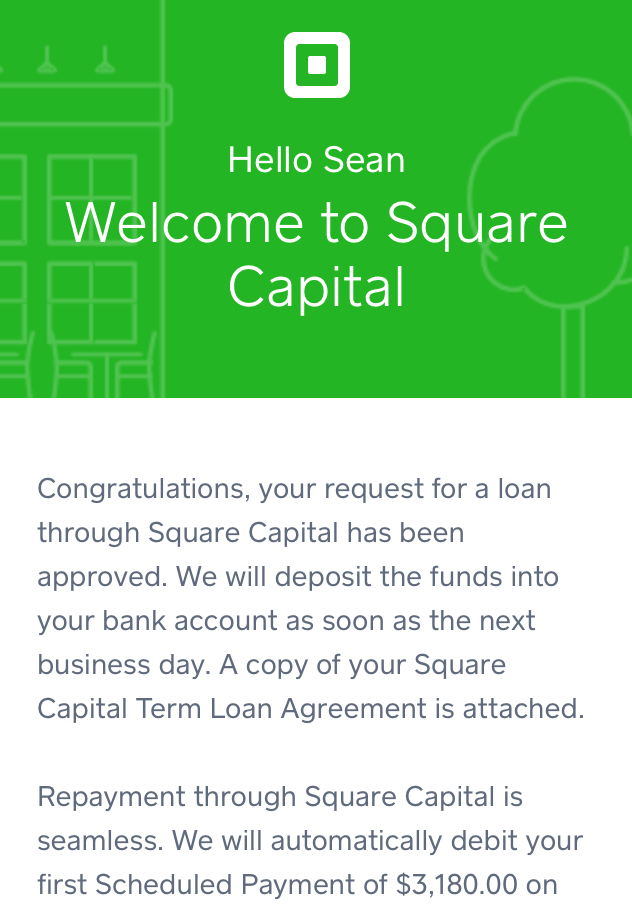

On December 1st, my company received a deposit for $35,000. It was a loan from Square Capital and I didn’t pursue it for a story, but rather to facilitate cash flow at the busiest time of the year. I was moving into a larger office on the same floor of our building and the hustle and bustle of the pre-holiday craze was upon us. The circumstances may come off a bit cliché, simulated even, but there it was at the right time and the right place, an email telling me that my business had been “selected.” If you’ve ever wondered if that kind of marketing works, it must, because a half hour after reading through the materials, I made an educated decision and applied for a loan.

The higher-ups at Square Capital, those above the underwriting department, might have no idea that they even funded us (our legal name is different from our trademark publication name). And I haven’t reached out to them for comment because I didn’t want to turn this into a PR stunt or get them riled up about my account. But if you work at Square and you’re reading this now, you don’t need to hold your breath. Everything seemed to work just as the press releases, ads, and executives claim it does. Phew! That’s good for you, but it was also very good for me.

The most pleasant surprise was that our business got approved for the maximum amount advertised in their email. Here’s how it went down:

11/29/16

1:34 PM

Received email offering a business loan up to $35,000 to repay over 12 months

2:01 PM

Applied for $35,000, which consisted of logging into my Square account and tapping a button

8:02 PM

Got approved for $35,000

11/30/16

Square sent out the funds via ACH

12/1/16

Received full loan deposit in my business bank account

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

As a small business owner, I calculated whether or not it made sense to pay a set fee for $35,000 over that time period and determined it did. An APR would not have impacted my decision, nor would I really have found it helpful in determining the supposed true cost. The true cost is already there in black and white, the total dollars I agreed to pay.

Two things guided me, speed and economics. I wasn’t motivated to shop around to try and get the absolute best deal, just one that made economic sense with the least amount of work in the shortest amount of time. It sounds ironic to write that, especially as someone who has a bachelor’s in both Accounting and Finance but if you’re someone who works 7 days a week like I do, well maybe you’d understand my thought process. If I was applying for a million bucks, then yes, I’d shop and think on it pretty hard, but in my circumstances, a few thousand dollars in fees is relatively small stakes for the company. Besides, I was using the money proactively, as a positive tool.

I knew my patience for waiting was thin. For example, an experience with one of my banks earlier in the year had already left me rattled. I had asked to extend the limit of a business credit card and I was told that in order to do so, I’d have to visit the bank branch where I had originally signed up for the card (I don’t even live near that branch anymore) and that I would have to bring financial statements with me to present for review. By the way, this was for a limit increase to an amount that was much less than $35,000.

I learned that day that the rumors about (some) banks are true. They wanted me to visit a branch… and bring paperwork… for some kind of unspecified analysis… in 2016. Lo and behold I never showed up, and was more entrenched in my belief than ever before that the world needed to become de-banked and soon.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

Alas, the entire process really all just came down to clicking a button online. I kept waiting for the catch, for them to let me down, to come up short of all the promises that the Fintech revolution has made about changing the world, but it never happened. A month later, Square withdrew their first payment from our account. Like I said earlier, I was satisfied with the entire process and it was a big help. Had I been given the option however, I might’ve opted to structure the arrangement differently and sold a portion of our future sales proceeds rather than simply borrow money. Allow me to explain.

It’s entirely possible that the next 12 months of business won’t pan out the way I project. If my sales drop, I still have to make the fixed monthly payment in accordance with my loan terms regardless. Not so when selling future sales since the delivery of those funds to the buyer is entirely tied to actual sales activity. A structure like this, what many consider a merchant cash advance, is actually what Square used to offer up until early 2016.

When the pace of sales slow down, delivery of the sales proceeds slows with it. When the pace of sales increases, so too does the delivery to the buyer. And if I went out of business, well then the buyer would get what they purchased, nothing.

Merchant cash advances are harder to bundle up and securitize though because there are no maturity dates nor is there even a guarantee the buyer will get what they purchased in full. They’re investments with loads of uncertainty built in for the buyer, and that’s probably why Square switched to loans and also probably why the cost of my loan was relatively inexpensive. They’ve minimized the uncertainties.

Nonetheless, the loan I ultimately got, is just fine. In the moment that I needed it, the process couldn’t have been any simpler or any faster. The banks have met their match. I got funded and loved it, now it’s your turn.

Equity Crowdfunding to Masses Slow Out of the Gate, But Pickup Expected

February 25, 2017

After a lackluster start, spectators are betting on more promising times ahead for equity crowdfunding to the masses.

Although it’s been talked about for years, it wasn’t until last May that the general public could buy shares of their favorite companies through equity crowdfunding. Before then, only accredited investors could be part of the crowd.

The new crowdfunding regulation, known as Reg CF, has been talked about for several years as a potential game-changer for small businesses seeking growth capital. But so far, it hasn’t gotten the fast-track reception that some industry watchers had hoped for. Between inception and January 16 of this year, 75 companies have run successful equity crowdfunding campaigns, raising $19.2 million, according to statistics compiled by Wefunder, an online funding portal for equity crowdfunding.

Even so, industry watchers aren’t discouraged, saying it takes time for any new product to catch on and to gain traction.

“Equity crowdfunding is in its infancy. It’s got to be a toddler before it can be a teenager, and it’s got to be a teenager before it can be grown up. I think in three to five years, equity crowdfunding will be all grown up,” says Kendall Almerico, a partner with the law firm DiMuroGinsberg in Washington, who represents numerous clients in Jobs Act-related offerings.

A YEAR OF TRIAL AND ERROR

Some industry watchers had hoped equity crowdfunding to the general public would take off immediately, on the heels of successful rewards-based crowdfunding sites like Kickstarter and Indiegogo. Consider that since Kickstarter launched on April 28, 2009, 12 million people have backed a project, $2.8 billion has been pledged, and 118,362 projects have been successfully funded, according to company statistics from Jan. 16.

People looked at Kickstarter’s accomplishments and projected that from day one, equity crowdfunding to the public would be an immediate success, Almerico explains.

Instead, Almerico says 2016 was a year of trial and error, in which companies seeking equity funding tested out the market and learned the process. Initially, there were several funding failures, where companies set fundraising goals that were too lofty and came away with nothing. Other companies have been hesitant to dip their toes into a market that’s still very new and unchartered.

“I’m not surprised that it has taken a little bit of time for companies to raise money this way,” Almerico says.

However, industry participants say that every success story encourages others and the market will continue to build on itself.

“We are very optimistic that 2017 will be the year it goes more mainstream in the U.S,” says Nick Tommarello, founder and chief executive of Wefunder, who expects crowdfunding levels in 2017 to reach three to four times what they were at the end of 2016.

WADING THROUGH UNCHARTERED TERRITORY

Certainly, Reg CF is still very new in practice. On October 30, 2015, the Securities and Exchange Commission adopted final rules to permit companies to offer and sell securities through equity crowdfunding for non-accredited investors. But it wasn’t until May 16, 2016 that this new type of investing actually became permissible.

Companies that want to raise money from the general public have to do it through a funding portal that is registered with the SEC. As of mid-January, there were 21 funding portals, according to a listing on Finra’s website. The bulk of the funding thus far has come through the portals Wefunder, StartEngine and NextSeed, according to statistics compiled by Wefunder. Indiegogo, best known as a leader in perks-based crowdfunding, has also gotten a fair amount of business. Indiegogo launched an equity crowdfunding portal late last year through a joint venture with MicroVentures, an online investment bank.

There are significant rules when it comes to members of the general public investing in equity deals; how much you can invest per year depends on your net worth or income. Everyone can invest at least $2,000, and no one may invest more than $100,000 per year, according to SEC rules.

Meanwhile, companies are limited to raising $1 million in a 12-month period using Reg CF. Also, they must raise enough to hit their funding target or the fundraising round is a bust. They can, however, use other avenues to raise money simultaneously, such as through accredited investors or venture capitalists. This can be an advantage for companies because it allows them to tap their customer base—a great marketing and customer-retention tool—and yet still seek growth financing from investors with deeper pockets.

Over time, as equity crowdfunding gains traction, Almerico predicts the SEC and Congress will revisit some of the regulations and tinker with the laws to make them even more user friendly. And that too, will help crowdfunding gain ground with investors and companies, he says.

For instance, under current rules, a company can’t market its offering until it goes live, at which point additional marketing restrictions set in. Congress and the SEC will likely change some of these restrictions to make the rules more similar to Regulation A, which covers offerings of larger sizes, Almerico says.

A CONSUMER-FACING PROPOSITION

For the most part, companies that are consumer-facing as opposed to B2B will have the most luck with equity crowdfunding. For one thing, consumer-facing companies often have an easier time explaining their story to the public. Also, there’s real benefit for consumer based businesses to get their customers to sink money not only into a company’s product, but behind the scenes as well. Thus far companies that have sought funding under Reg CF run the gamut from breweries to tech startups, Wefunder data shows.

When it comes to equity crowding, investment levels tend to be small. Wefunder stats shows that 31 percent of investments made through its own platform are $100 and 76 percent of investments are under $500. “The whole point is to have lots of investors investing small amounts of money and together they add up,” Tommarello explains.

One of Wefunder’s largest offerings was Hops and Grain Brewing, a microbrewery based in Austin, Texas. The company is one of three businesses to raise $1 million on Wefunder, and more than 70 percent of the money came from its own customers, according to Tommarello. “Equity crowdfunding allows customers an opportunity to back things they really care about and it’s great marketing for the company too,” he says.

Another company, Snapwire Media Inc., a start-up in Santa Barbara, California, also believes in the power of the crowd to raise funds and gain marketing traction. Chad Newell, the company’s chief executive, says Snapwire wasn’t at a point where it felt ready to solicit venture capital money, but felt confident that its users, who were already passionate about its services, would become their biggest advocates.

The company, which connects a new generation of photographers with businesses and brands that need on-demand creative imagery, was launched in 2014. It previously raised $2 million from accredited investors before raising $179,065 from the general public on the funding portal StartEngine. In December 2016, the company launched a campaign to raise additional funds on Wefunder.

“Because we had a strong community and such a large one, we felt it was a good way to raise funds. Why not raise it from the people that care about the product the most?” Newell says.

OVERCOMING THE HURDLES OF NEWNESS

Because equity crowdfunding to the general public is so new, there’s still a lot of uncertainty about how the process works—both among companies looking to raise money and potential investors.

“The biggest hurdle today is that equity crowdfunding is still underground versus rewards-based crowdfunding,” says Howard Marks, co-founder and chief executive of the online portal StartEngine. “It’s tiny. It’s small. It’s nothing. It’s not even a dot in the grand scheme of things,” he says.

At this point, many people still don’t realize they can invest, or how to invest. He likens equity crowdfunding to index funds or junk bonds that were once completely unknown products. Over the years, however, they gained broad acceptance and are now widely used investment vehicles. “Every time there’s a new financial product that comes out, it takes time,” he says.

At this point, many people still don’t realize they can invest, or how to invest. He likens equity crowdfunding to index funds or junk bonds that were once completely unknown products. Over the years, however, they gained broad acceptance and are now widely used investment vehicles. “Every time there’s a new financial product that comes out, it takes time,” he says.

In December, five new companies used StartEngine for equity crowdfunding. In January, he expects there to be more than 10. By the middle of next year, he predicts there could be 20 a month, and in two years from now he’s hopeful to be doing about 500 equity deals a month.

“Within five years, our plan is to have 5,000 companies on the platform,” he says. “The demand for capital is pretty large.”

At this point, Wefunder is the largest platform for Reg CF offerings in terms of dollars funded, successful offerings and number of investors.

According to data through January 16, forty-six of the seventy-one companies that listed on its platform, or 65 percent, had successful offerings, meaning they reached their investment goals.

Some funding portals have felt the pangs of being new to the industry and are trying to get their bearings to compete more effectively.

Vincent Petrescu, chief executive of truCrowd Inc, a funding portal based in Chicago, says his company got registered in May 2016 and spent the rest of the year learning the lay of the land. Ultimately, truCrowd decided it would be better off specializing in a few verticals than going after all types of companies. Its plan now is to focus on the cannabis industry and the HR space.

“I think that the potential is huge. There are lots of good companies out there that need capital,” he says.

THE SNOWBALL EFFECT

Wefunder data shows that investors who buy into one deal tend to do another deal shortly after, so it’s a compounding effect, Tommarello says. “It’s a snowball rolling down a hill. We’re developing a whole new class of mini angel investors,” he says.

In terms of future growth, Petrescu of truCrowd says the biggest hurdle for the industry is exposure. Lots of people still don’t know about it, and they are still in the mindset that it’s illegal because it was for so long.

He says he’s not too concerned, though, because the UK had a similar experience when equity crowdfunding to the general public first started there a few years back. As soon as the success stories start to become more publicized and people see the returns that are possible, he predicts interest will grow. “The potential is there. No doubt about it,” he says.

For companies that are giving more thought to equity crowdfunding, it may help to seek out advice from others that have already traveled this road. Newell of Snapwire says he gets calls every week from company founders to ask about his experience with equity crowdfunding and to discuss in further detail whether it might be the right option for them.

Newell tells companies that ask him about equity crowdfunding that it’s an effective way to raise funds, with certain caveats. For instance, you really have to understand the rules of what you’re allowed to do and what you can’t do because there are many more restrictions when marketing to the general public versus accredited investors. You also have to be good at marketing—or hire a company to do it on your behalf—and have a sizable group of users that you think will want to invest in your future.

“It’s been a great source of capital for Snapwire because of our passionate community. I caution any company that doesn’t have a large community to be careful about spending time and resources and have realistic expectations,” he says.

He also says companies should have realistic fundraising goals since it is unusual—at least at this juncture—to raise a million dollars from small investors through equity crowdfunding. It’s more realistic to expect to raise $200,000 to $500,000, he says.

“I think everyone gets attracted to the top number. But that’s not necessarily what happens. Equity crowdfunding should be complementary to any funding strategy. By itself, it’s not some magic bullet,” he says.

The LendIt Story

February 12, 2017

The LendIt Conference was supposed to be a smallish local meetup for New York-based members of the online lending community. But founders Jason Jones and Bo Brustkern soon discovered they had the makings of a big annual industrywide national convention. And before long, they found themselves replicating their successful American show on other continents.

To understand how the trade show was born and how it’s matured, flash back about seven years. In 2010, Jones and Brustkern were putting together venture capital deals when they happened onto the fledgling peer-to-peer lending movement. “Consumer credit was something we weren’t all that knowledgeable about, but we could see the market was large,” recalls Jones. “There was a clear opportunity that was structural in the market, and there were stable, consistent returns.” So the two of them launched one of the first P2P funds.

Their lending business soon took off, but Jones and Brustkern felt they were working in a void. The industry lacked community, and they decided to do something about it. Jones contacted his friend, Dara Albright, who had been organizing a series of crowdfunding conferences for Wall Street starting in mid 2011.

To heighten the credibility of the new confab, Jones, Brustkern and Albright decided to seek the help of Peter Renton. They didn’t know Renton personally but considered him “the voice of the industry,” Jones says. Renton had nurtured and sold off two printing businesses and used the proceeds to take up online lending as a hobby. He had also launched the Lend Academy in 2010 to teach the world about peer-to-peer lending. Somehow, he had also found the time to develop a following for himself as a blogger.

In early January of 2013, Jones and Albright cold-called Renton to gauge his interest in putting on a show. As fate would have it, Renton had just made a New Year’s resolution to launch a conference for lenders and was receptive to joining up. Together, they put a plan in action.

The originators put up their own money and worked together daily from January to June of 2013, when the first show convened. They secured space that would contain 220 people and calculated their break-even point as 200 attendees. “This was never intended to be a profitable enterprise,” Jones says of those early days. “This was something we all wanted to do for the community. We thought that if we wanted it, others would want it.”

More than 400 people registered for that first conference. “We had a line literally out the door,” Jones notes. “We had to shut off registration. We ended up squeezing about 375 people into that first event. It was completely shocking to us.” From the beginning, attendees came from all over the world. “That’s when I learned China had a P2P industry,” Jones says.

After the initial event, Jones, Brustkern and Renton formed a unified company. Renton brought in Lend Academy, while Jones and Brustkern added their investment fund. The conference also became part of the united company. Ever since, a holding company has owned all three businesses. Dara went on to launch Fintech Revolution TV and continues to support LendIt.

From the initial attendance of 375, the U.S. conference grew to 975 attendees in 2014, 2,500 in 2015, 3,500 in 2016 and a projected 5,000 for this year. About 33 percent of attendees come from the fintech industry, 23 percent are investors, 23 percent are service providers, 14 percent are banks and 2 percent come from government, the media and other backgrounds, Jones says. At first, many of the attendees come from the ranks of CEOs and managing partners, but that’s changing as the industry comes to view the conference as an annual convention where lower-ranking members of an organization can learn about the business, he notes.

Meanwhile, the exhibition floor is becoming an increasingly important component of the show. The gathering attracted 18 exhibitors in 2013, followed by 47 in 2014, 112 in 2015, 177 last year and an expected 210 this year. “We’re transforming from a conference-led event to an expo-led event,” Jones says. This year, exhibitor booths will occupy a 120,000 square-foot hall in New York’s Jacob K. Javits Convention Center.

The U.S. LendIt conferences alternate between San Francisco and New York City, renting larger spaces as the show has grown, Jones explains. Two years ago, the gathering seemed cramped in the gigantic New York Marriott Marquis near Times Square, he says, necessitating this year’s move to the Javits Center. Javits is designed for conventions with at least 10,000 attendees so the show is a little small for that venue, he admits. But the facility could become LendIt’s long-time New York home as growth continues, he predicts.

Jones traces some of the growth in exhibitors to the expansion of the fintech industry. “You have a meeting of the start-ups with the more traditional players who are rethinking their businesses and how to apply the new technology that’s being developed into their businesses,” he says.

Conferences that compete with LendIt in the fintech category are proliferating because of the nature of industry, in Jones’ view. As soon as fintech companies are launched, the internet quickly makes them national or even international in scope, he says. At the same time, the anonymity of cyberspace creates a need for gatherings that provide face-to-face meetings, he maintains. “They live online,” he says. “The spend their year online so there is a need for a convention to meet with their peers, their clients, their service-providers, their customers, their suppliers. There is a need for that physical connection.”

The increase in fintech conferences is also driven by content-related companies that provide articles on fintech innovation. Those sites have regarded conferences as money-makers that complement their journalistic endeavors, Jones says. For example, TechCrunch, an online publisher of technology industry news, puts on the TechCrunch Disrupt conferences in San Francisco, New York City, London and Beijing. In another example, Business Insider conducts the IGNITION conference.

Those forces – the internet, globalization and web-based publishing – are making themselves felt in the convention business in general, not just in fintech, Jones notes. Event-related companies trade at roughly 12 times EBITDA (earnings before interest, tax, depreciation and amortization), he says, characterizing the convention business as “a very healthy category of our economy.”

Still, the fintech field’s crowded with more than 30 conferences, but LendIt is succeeding because of its early start and an emphasis on community, according to Jones. “We come from the industry,” he contends. “People are happy with what we can produce. They love our content so they come to learn.” Because the conference has become established, the media outlets focus on covering it, which encourages businesses to use it as a stage for introducing products or announcing mergers and acquisitions, he maintains.

Jones views LendIt and Money20/20 as the largest pure-play fintech conferences. The latter, which attracts 11,000 attendees, focuses on payments and contains a “layer” of fintech, while LendIt specializes in lending and likewise offers a “layer” of fintech, he says. Payments and lending represent the two biggest categories in fintech, so the structure of the shows makes sense, he suggests. By chance, Money20/20 occurs in the fall and LendIt takes place in spring, creating what he considers a “nice balance” that encourages prospective attendees to go to both shows.

Finovate holds a rival fintech conference that focuses more narrowly on innovation than do the LendIt and Money20/20 shows, Jones says. A competing bank securitization conference offers information on lending but doesn’t address fintech in great detail, he says.

While LendIt has been coming of age in the U.S., it’s also gained siblings in Shanghai and London. The Chinese edition of the show, which made its debut in 2014, ranks as the largest fintech show in Asia. The Chinese fintech market has grown to at least five times the size of any other market in the world, and it’s home to four of the world’s five largest fintech companies, Jones says. “We were completely blown away,” he says of learning about the industry during a visit to China.

Despite the language barrier and the challenges of dealing with an unfamiliar culture, LendIt has managed to prosper in China. Through a joint venture with a local financial think tank, LendIt helped produce annual Chinese events known as the Bund Summit for two years with attendance capped at 500. For the third year, LendIt parted ways with its partner and recast the show as a larger event. After the change, the confab, now called the Lang Di Fintech Conference, attracted 1,200 attendees, making it China’s largest. “There’s a ton of future opportunity,” Jones predicts of the China endeavor. “We want to be the annual convention for the Chinese fintech industry.”

Although it’s difficult to set up operations in China, cooperation has prevailed there in at least some areas. “The government has been quite supportive,” Jones says of of Chinese officials. “They appreciate what we’re trying to do there.” In January, LendIt launched its Chinese language daily news feed.

Thousands of miles away, the European-based LendIt confab ranks second in size on that continent only to the European version of Money20/20, Jones says. Attendance at the London-based LendIt show numbered 450 in 2014, which was its initial year. It climbed to 800 in 2015 and reached 925 last year.

Putting on the European event requires much less effort than the Asian version because it’s almost an extension of the U.S. original, he says. It’s dominated by firms from the United Kingdom but draws a smattering of companies from other European nations. Crossing borders presents challenges for European fintech companies, which keeps the industry’s companies smaller there than in the U.S. and China, but that may change, he believes. “There’s a lot of innovation there, but they still have a ways to go,” he says.

To handle its far-flung operations, LendIt relies on 20 full-time employees, 11 contractors and 10 people working in a joint venture in China for a total of 41 staff members. “These events are incredibly large shows, and we constantly feel understaffed,” Jones says. That feeling prevails despite recent additions to the staff, he notes.

And additional opportunity beckons in myriad locations. “The challenge is, do you have a bunch of conferences all over the world, or do you do a beachhead and pull people to those three events?” Jones wonders aloud when asked about the future. “For the moment, we have made the strategic decision to stick with these three events and go deeper with them. But there are so many opportunities all around the world. We’re constantly being asked to come to different countries.” Then, too, LendIt could convene smaller, one-day events around the glove as feeders to the three main conventions, he allows. “That’s something we’re batting around now.”

The established two-day conferences could also grow into three-day affairs – but not right away, Jones suggests. “We’re totally running out of time,” he says of trying to cram in all the speakers and exhibitors that LendIt would like to present. Stretching the format could create conflicts because some participants attend other events immediately before or after LendIt.

Notable LendIt speakers have included Larry Summers, who’s served as Harvard president and U.S. Treasury Secretary; Karen Mills, former administrator of the U.S. Small Business Administration; John Williams, president and CEO of the Federal Reserve Bank of San Francisco; and Peter Thiel, venture capitalist and member of the Trump transition team. This year, attendees can look forward to meeting the robot that represents Watson, the IBM computer. Watson will take the stage to field questions about fintech. For Jones, however, creating a conference isn’t just about the big-name speakers be they human or mechanical. “People who are lesser-known can be really fascinating,” he says.

Whoever handles the speaking duties, the LendIt Conference executives vow that they’re in it for the long run as the fintech industry’s annual convention during both boom times and economic slumps. As Jones puts it: “We want to be a reflection of our industry.”

The New Normal

January 24, 2017 In March 2014, I wrote the following for DailyFunder.com: I think we are either currently in, or are fast approaching a “market bubble” in MCA. Bubbles never end well…When I see some of the business practices, offers, terms and other aspects of our business today, I am worried…assets are being overpaid for through higher than economically justified commissions …and [funders are] stretch[ing] the repayment term of the MCA or loan even further. I went on to say that this felt to me an awful lot like the subprime mortgage meltdown of 2008.

In March 2014, I wrote the following for DailyFunder.com: I think we are either currently in, or are fast approaching a “market bubble” in MCA. Bubbles never end well…When I see some of the business practices, offers, terms and other aspects of our business today, I am worried…assets are being overpaid for through higher than economically justified commissions …and [funders are] stretch[ing] the repayment term of the MCA or loan even further. I went on to say that this felt to me an awful lot like the subprime mortgage meltdown of 2008.

Like all good bear market prognosticators, I was a touch early in my forecast. 2014 and 2015 were continued boom years for small business alternative lenders (or “small business Alt Lender.” I don’t agree with applying the moniker “online lender” for our industry. It might be sexy, but it’s not accurate.) Loan and MCA terms got longer, loan pricing to the client dropped further, companies grew 100% year over year. And then 2016 happened.

The most shocking event for me in 2016 was the disruption at CAN Capital. They had the most data, the most experience, market dominance, and the most in-depth institutional knowledge. The granddaddy of all of us. Not far behind is the fiasco that is On Deck, the only publicly traded small business Alt Lender. In the past 12 months alone, the stock price has declined by over 40%. And that is after a roughly 50% drop in stock price in 2015. The first 9 months of 2016, driven in part because of market required changes to their business model when they could no longer profitably sell a sufficient volume of loan originations, they have a GAAP net loss of almost $50 million. There have also been a number of other lesser but still high profile failures, shutdowns, and exits from the industry in the past several months alone.

So what is driving this abnormally high rate of failure in the Alt Lending industry? Is it the “New Normal?” And what do I think lies ahead in 2017 and beyond? Before revealing my personal crystal ball again, I will share an anecdote from earlier in my business career.

I was the CFO (and eventually CEO) of a profitable, long-tenured family owned construction company. We had a working capital credit line from a major bank secured by a first position lien on our accounts receivable. The credit line was also personally guaranteed. We borrowed from the credit line for three reasons. For cash flow, when our receivables paid more slowly than expected; we had tax payments due; or we purchased a large piece of equipment. We always paid back the draw on the credit line as quickly as we could, to keep interests costs low, to impose cash management discipline, and to create future availability on the line once repaid.

The credit line was for one year. It was always renewed. But I was frustrated to have to go through an annual underwrite process with our bank, despite the personal guarantee, consistent profitability, and that we always paid back our draw on the credit line. Our banker (patiently) explained to me that economic cycles changed, and medium sized businesses – we had about 200 employees – suffered ups and downs and sometimes became financially distressed and even went out of business. The bank wanted to protect their position and not overextend the term of the credit line.

The credit line was for one year. It was always renewed. But I was frustrated to have to go through an annual underwrite process with our bank, despite the personal guarantee, consistent profitability, and that we always paid back our draw on the credit line. Our banker (patiently) explained to me that economic cycles changed, and medium sized businesses – we had about 200 employees – suffered ups and downs and sometimes became financially distressed and even went out of business. The bank wanted to protect their position and not overextend the term of the credit line.

When I started RapidAdvance in 2005, I drew on my personal knowledge and previous experience as a borrower. The products we offered made sense based on our customer profile which was main street small business. We needed to protect against economic cycles and the high rate of small business failure. The maximum term offered by any company in 2005 was 8 months, at that time only for an advance product (future purchase and sale of credit card receivables), not a loan. Payment was received daily through a credit card split, thus allowing for a future capital advance (renewal) within about five or six months as the open advance was paid down. Cash advances could be used for taxes, equipment purchases, or business expansion. The price of the product reflected the risk of the credit offered.

What many in the small business Alt Lending industry seem to have forgotten, or never learned, is that our business is fundamentally a subprime credit industry. We are either lending to subprime borrowers, because of either the personal credit of the owner or the balance sheet of the borrower, or if the credit is strong and the business is more substantial, the loan itself is a subprime risk because we are at the bottom of the capital stack – behind the bank loan, the business property mortgage loan, the other personal guarantees of the owner, the factoring company, etc. We are taking the most risk. To offer two and three year terms and to try to pretend to get to “bank like” rates is, in my opinion, committing lending suicide.

At Rapid, we were dragged kicking and screaming into slightly longer term and lower cost products in order to stay competitive with certain customers. But we have kept that pool of customers as a very small percentage of our overall receivables.

Going into 2017 and beyond, I see five major trends. First, terms will get shorter, prices will increase, and offers will become more rational. That is already happening. Second, capital to this industry will become less available. The best companies with proven data driven models, consistent underwriting, a strong balance sheet and predictable loss rates will get financed. The days of easy money chasing this space are over. Equity will be particularly hard to come by.

Third, there will be continued disruption of funding companies. Companies will consolidate and some will disappear. On Deck may be in for a big challenge. They had a tremendous cash burn converting their business model to more balance sheet financed instead of originating and selling loans. Their market cap today is approximately book value, i.e. if you could buy up all the shares of the company at today’s trading price that would be roughly equal to their cash on the balance sheet and the value of their net receivables. The next two quarters are crucial for them to show the market they have turned the corner to become a self-sustaining lender. I am not optimistic, but I am rooting for them to succeed as it is in the best interests of the industry.

Fourth, stacking will continue to be an issue. I believe that the legal system over the next few years will bring some semblance of order to this industry scourge. At Rapid we have taken an aggressive legal stance against stacking, with some success in the courts. The challenge is that each situation is fact specific, and to prevail in a claim of tortious interference, the first position lender has to prove damages. I think that an unrelated decision at the end of 2016, Merchant Funding Services, LLC vs. Volunteer Pharmacy in New York State, could be a game changer. Because of the form of contract and the business practices in Volunteer, the judge ruled that the transaction constituted criminal usury. Knowing the business practices of the stackers, specifically the practice of writing an agreement that pretends to be a sale and purchase of future receivables but is in fact a loan, which is the basis for the judge’s ruling in Volunteer, I can see lawyers seizing on this precedent to help overstressed small business owners attempt to void their stacked loan agreements. The small business would first block the stacker’s ACH, claim the contract is void because of criminal usury, and then sue the stacking company. There could also be class action lawsuits like we saw a few years ago in California – bundle together a number of these claimants and go after the deep pocketed investors and banks that finance the stacking companies. The State’s Attorney General in New York may take a public policy interest in these types of loans. Once the dominoes start to fall, the costs of stacking – litigation and unpaid loans, in addition to proactive claims for damages – could be enormous for both the stacking companies and their owners and investors.

Fourth, stacking will continue to be an issue. I believe that the legal system over the next few years will bring some semblance of order to this industry scourge. At Rapid we have taken an aggressive legal stance against stacking, with some success in the courts. The challenge is that each situation is fact specific, and to prevail in a claim of tortious interference, the first position lender has to prove damages. I think that an unrelated decision at the end of 2016, Merchant Funding Services, LLC vs. Volunteer Pharmacy in New York State, could be a game changer. Because of the form of contract and the business practices in Volunteer, the judge ruled that the transaction constituted criminal usury. Knowing the business practices of the stackers, specifically the practice of writing an agreement that pretends to be a sale and purchase of future receivables but is in fact a loan, which is the basis for the judge’s ruling in Volunteer, I can see lawyers seizing on this precedent to help overstressed small business owners attempt to void their stacked loan agreements. The small business would first block the stacker’s ACH, claim the contract is void because of criminal usury, and then sue the stacking company. There could also be class action lawsuits like we saw a few years ago in California – bundle together a number of these claimants and go after the deep pocketed investors and banks that finance the stacking companies. The State’s Attorney General in New York may take a public policy interest in these types of loans. Once the dominoes start to fall, the costs of stacking – litigation and unpaid loans, in addition to proactive claims for damages – could be enormous for both the stacking companies and their owners and investors.

Lastly, and to my great pleasure, I think we will stop hearing small business Alt Lenders calling themselves “Fintech.” I think we will see the beginning of the demise of fully automated, no manual touch funding. At Rapid we have data and risk and pricing algorithms but we have always had an underwriter at a minimum review every file. At conferences when I have presented or participated in Fintech panels I always referred to Rapid as a technology enabled, non-bank small business lender. Now even On Deck describes themselves in similar terms.

Lastly, and to my great pleasure, I think we will stop hearing small business Alt Lenders calling themselves “Fintech.” I think we will see the beginning of the demise of fully automated, no manual touch funding. At Rapid we have data and risk and pricing algorithms but we have always had an underwriter at a minimum review every file. At conferences when I have presented or participated in Fintech panels I always referred to Rapid as a technology enabled, non-bank small business lender. Now even On Deck describes themselves in similar terms.

I titled this post “The New Normal.” In the classic Mel Brooks movie Young Frankenstein, Dr. Frankenstein sends his assistant Igor to steal a brain from a cadaver to implant into his monster. But Igor accidentally drops the genius brain he was supposed to steal, and brings the doctor a different brain without telling him. When the monster awakes and has the personality of a psychotic five year old, Igor tells him he brought him a brain that was labeled “normal” instead of the one he was supposed to steal. It was, as Igor read it, “Abby Normal.” Abnormal, I believe, is the “New Normal” we will be dealing with in 2017.

A True Rapid Advance For Mark Cerminaro

December 16, 2016 In the 1999 film “Any Given Sunday,” Al Pacino plays a pro football coach whose obsession with winning has torn apart his family. He’s also plagued by a meddlesome team owner, challenged by an offensive coordinator who’s after his job, and vexed by a talented but narcissistic backup quarterback. But none of that stops the coach from reaching deep inside to deliver a stirring halftime pep talk to his dispirited losing team. Assuring his players that life and football are both games of inches, he beseeches them to look into the eyes of the men around them. “You’re going to see a guy who will go that inch with you,” he declares. “Either we heal now as a team or we will die as individuals.” The players rally and explode onto the field.

In the 1999 film “Any Given Sunday,” Al Pacino plays a pro football coach whose obsession with winning has torn apart his family. He’s also plagued by a meddlesome team owner, challenged by an offensive coordinator who’s after his job, and vexed by a talented but narcissistic backup quarterback. But none of that stops the coach from reaching deep inside to deliver a stirring halftime pep talk to his dispirited losing team. Assuring his players that life and football are both games of inches, he beseeches them to look into the eyes of the men around them. “You’re going to see a guy who will go that inch with you,” he declares. “Either we heal now as a team or we will die as individuals.” The players rally and explode onto the field.

It’s a scenario the sales staff can’t get enough of at RapidAdvance, a Bethesda, Md.-based alternative small-business finance company with more than 200 employees. Mark Cerminaro has screened a clip of the scene countless times in a company conference room to fire up his crew. Salespeople emerged from those meetings eager to make that extra phone call, provide the telling detail on an application or do whatever else it would take to taste the victory of making the sale. For Cerminaro, the movie and the sales meetings embodied his penchant for winning ethically through teamwork, dogged persistence and great customer experience. That credo has helped propel him to top management at RapidAdvance and has earned him accolades from once-skeptical financial services peers.

Cerminaro’s story begins in his hometown of Highland Park, N.J., where he experienced a small-town vibe but enjoyed easy access to New York City, Philadelphia and the Jersey Shore. He graduated in a class of 85 students from the local public high school, playing varsity football, basketball and baseball. Summers, he worked construction, did landscaping, delivered flowers and umpired Little League. “It was a great place to grow up,” he says.

In high school, Cerminaro sometimes went along for the ride when his sister, who was five years older, was choosing a college. On a visit to Georgetown University in Washington, D.C., Cerminaro stood in the student center and gazed out at the campus. “I’m going to come here and play football,” he told himself.

In high school, Cerminaro sometimes went along for the ride when his sister, who was five years older, was choosing a college. On a visit to Georgetown University in Washington, D.C., Cerminaro stood in the student center and gazed out at the campus. “I’m going to come here and play football,” he told himself.

He made good on that vow when his high school football team made a reputation for itself, and Georgetown was among the schools that recruited him. Besides, it made sense to go there because he was interested in studying politics and going to law school. Growing up with a father who was chairman of the local Democratic Party, Cerminaro had his eye on eventually becoming governor of New Jersey.

Playing for the NFL on the way to the governor’s mansion seemed like a good idea, too. But Cerminaro, a quarterback, blew out his throwing arm two years into his collegiate football career. His dreams of making the pros died, but that left more time for academics. He plunged into a series of four rigorous internships, three of them in politics. He served two in the Clinton White House and one on Capitol Hill with Sen. Robert Torricelli, D-N.J. He fondly recalls talking to President Bill Clinton for five minutes before a state dinner. Then two hours later, after spending time with heads of state, the President called out, “There’s Mark, my fellow Hoya.” Cerminaro will never forget it.

In the end, however, the fourth internship won out. Although Cerminaro hadn’t studied business or finance too much, he landed an internship in the local Washington, D.C., office of Morgan Stanley. If nothing else, it would help him manage his investments some day, he reasoned. However, he soon approached the operations manager and some senior brokers and offered to take on duties they didn’t want to fulfill. He had decided to learn about operations, and taking on extra work without additional compensation was in line with his new habit of figuring out what steps would take him where he wanted to go in life.

Cerminaro earned his managerial license with Morgan Stanley and accepted a job as associate branch manager in the Washington, D.C., office, managing and training new financial advisors. He considered the position great exposure to sales, management, operations and compliance – “elements that have paid dividends in the growth of my career,” he notes.

Early in Cerminaro’s tenure at Morgan Stanley, the company sent him for training with about 300 other new employees at 2 World Trade Center in Manhattan. The date was Sept. 10, 2001. When the trainees reported to the office the next day, they were in a 64th-floor conference room when they heard an explosion and saw shreds of paper floating past the windows. They didn’t realize yet that a terrorist-controlled jetliner had hit next door at 1 World Trade Center.

Early in Cerminaro’s tenure at Morgan Stanley, the company sent him for training with about 300 other new employees at 2 World Trade Center in Manhattan. The date was Sept. 10, 2001. When the trainees reported to the office the next day, they were in a 64th-floor conference room when they heard an explosion and saw shreds of paper floating past the windows. They didn’t realize yet that a terrorist-controlled jetliner had hit next door at 1 World Trade Center.

As they evacuated down a stairwell, the trainees heard and felt the concussion of the second plane that hit their building. “I’m 22 years old and I may be about to die,” Cerminaro remembers thinking. “Make sure my family knows I love them,” he prayed. He made it out and was greeted with smoke, debris, the flashing lights of emergency vehicles and panic in the streets. He walked to a restaurant some family friends operated in Little Italy and borrowed a working phone to call his family in New Jersey and let them know he was OK.

Returning to the D.C. office of Morgan Stanley, Cerminaro got back to work. He loved the entrepreneurial spirit at the company, but as the years passed he realized he was unlikely to amass enough power in the giant firm to dictate how it would operate, grow and change. So he was interested when someone he knew at Morgan Stanley told him about RapidAdvance, then a two-year-old company with about 20 employees. “I saw the opportunity to be part of building a company – that’s what drew me to RapidAdvance,” he recalls.

In 2007, Cerminaro interviewed with Jeremy Brown, who was RapidAdvance’s CEO at the time and has since advanced to chairman. “It was apparent that Mark had a well thought-out, well-articulated plan for sales,” Brown says of his first impression. “He had a presence about him, a command that said this guy a real leader – somebody who could make a long term component of the company.”

Cerminaro joined RapidAdvance as national sales director and began building a sales structure and team based on some of the elements of Morgan Stanley’s sales model. Developing KPIs, or key performance indicators, helped him measure progress. “You had to roll up your sleeves and get involved in every aspect of things,” he said of working for a startup in a fledgling industry. The company’s outbound call center came up with sales leads, and he cut and pasted them from an Excel spread sheet and divvied them up among the five or six account executives.

Cerminaro wanted to teach that handful of salespeople to function as business advisors and help them become the single point of contact for clients. His salespeople guided small-business owners through the application process and stayed in contact with them after the sale. He emphasized doing right by customers, teammates and the company as a whole. It was a vision that inspired the team.

Cerminaro wanted to teach that handful of salespeople to function as business advisors and help them become the single point of contact for clients. His salespeople guided small-business owners through the application process and stayed in contact with them after the sale. He emphasized doing right by customers, teammates and the company as a whole. It was a vision that inspired the team.

“Mark was a great mentor and provided me a lot of guidance and tutelage over the years,” says Devin Delany, who started as an account executive at RapidAdvance and has moved up to director of sales. “His real mission was to create a sense of family and he executed on that to the fullest extent, creating a close knit team of upward of 40 folks who really care about one another.”

That sales “family” used dialogue marketing to refocus attention on prospects who had fallen out of the sales cycle. In those days they used a product-driven sales pitch based on merchant cash advances. Third-party partners included credit card processors and credit card ISOs. Brokers came onto the scene later.

Soon after Cerminaro arrived at RapidAdvance, the financial crisis struck. The company managed to navigate the troubled times and emerged with improved underwriting skills, a better understanding of leading indicators and a truer grasp of how its portfolio performs. Something else happened, too.

As traditional lines of credit dried up during the recession, small businesses that didn’t accept credit cards began to search for working capital. In response, Cerminaro, Brown and Joseph Looney, RapidAdvance’s chief operations officer and general counsel, sat down and outlined a plan to offer small-business loans as well as MCAs. “That effort really redefined who RapidAdvance was,” Cerminaro says of the new loans. “We went from a single-product company to now being more of a solutions-based company,” he maintains. “We were able to shift from selling a product to doing needs-based analysis with our clients and focusing on what was the right solution for them.”

As traditional lines of credit dried up during the recession, small businesses that didn’t accept credit cards began to search for working capital. In response, Cerminaro, Brown and Joseph Looney, RapidAdvance’s chief operations officer and general counsel, sat down and outlined a plan to offer small-business loans as well as MCAs. “That effort really redefined who RapidAdvance was,” Cerminaro says of the new loans. “We went from a single-product company to now being more of a solutions-based company,” he maintains. “We were able to shift from selling a product to doing needs-based analysis with our clients and focusing on what was the right solution for them.”

Cerminaro found it exciting to develop the loan program and oversee sales, but he was looking for more. He turned part of his attention to business development and even expanded his purview to include marketing. The company was thinking along the same lines. In 2010, RapidAdvance promoted him to senior vice president, sales and marketing. “As the company has grown we have had different needs, and we leaned on Mark and his skill set every time we made a change,” Brown says. “Every time we made a change he has stepped up and done what’s asked of him.”

Producing one of the industry’s first national television ad campaigns highlighted Cerminaro’s period as senior vice president. “We were the pioneers in being able to market through that medium,” he says. “It was absolutely scary at the same time. It was a massive investment for us and we had no idea whether it would pan out.” The sales staff were waiting in anticipation when the phones began ringing after the public saw the commercial. “The original spot we put together still tests well and drives a lot of traffic,” he notes. Viewers find a tune featured in the ad sticks in their minds and can’t help humming it – sometimes when they’d prefer they didn’t, he adds.

Then came another promotion. In 2013, just before Detroit-based Rockbridge Growth Equity LLC acquired RapidAdvance, Cerminaro was named chief revenue officer and became responsible for all revenue-generating activities and all of the company’s front end efforts. The company had grown significantly over the years, but the merger increased financial backing and thus accelerated growth, he says. For him, that meant pursuing a new type of partner company – asset-based lenders and factoring companies. It wouldn’t be easy. “The traditional lending market had a lot of misconceptions about our industry,” Cerminaro admits. “A lot of people in that business were very critical.”

But Cerminaro made the rounds of trade shows and visited conference rooms until he succeeded in winning the hearts of bankers, according to Will Tumulty, RapidAdvance’s CEO. “Mark and his team have developed partnerships in the commercial lending space,” Tumulty says. “There are a number of companies that have historically viewed working-capital funding as a competitor. We don’t see ourselves competing with those companies. Mark and his team have worked with those companies to get merchants what they need.”

As a testament to Cerminaro’s success in that quest, the Commercial Finance Association named him to its 2016 list of “40 under 40” achievers. He was the only person from alternative small-business funding to make that venerable list of prominent young lending executives. He helped spur his company on to other awards, too. The RapidAdvance Bethesda office was chosen for The Washington Post Top Workplaces 2016 list, and the RapidAdvance Detroit office made the list of 101 firms recognized as Metro Detroit’s 2016 Best and Brightest Companies to Work For.

Meanwhile, Cerminaro was successfully courting mega retailers, says Brown. When the possibility of becoming a partner with Office Depot arose, Brown felt hopeful but remained skeptical because of the long lead time required to convince so many executives in such a large corporation. “But mark was dogged,” he says. “It took him probably a year to land and close the deal and negotiate the agreement and sign the account. He went to countless meetings down in Florida. He participated in endless conference calls, but mark got the deal done. It’s a relationship we’re proud of, and he is singularly responsible for closing that deal.”

In those encounters with Office Depot execs, Cerminaro displayed savvy and professionalism, Brown says. They’re traits that will continue to pay off not only for RapidAdvance but for the entire industry, maintains RapidAdvance’s Looney. “He’s out there with lots of big banks and other potential partners,” says Looney. “He’s a good face for the industry.”

For Cerminaro, it’s satisfying to see RapidAdvance become all he dreamed it could be. But that still comes in second for him and differentiates him from the coach played by Al Pacino. Cerminaro’s the kind of guy who asked his father to be his best man and now has a wife and two sons of his own. “Your family and your loved ones are by far more important than anything else in your life,” he says.

Alternative Funders Bid Adieu to 2016, Show Renewed Optimism for 2017

December 12, 2016

After getting pummeled in 2016, many alternative funders have licked their wounds and are flexing their muscles to go another round in 2017.

“The industry didn’t implode or go away after some fairly negative headlines earlier in the year,” says Bill Ullman, chief commercial officer of Orchard Platform, a New York-based provider of technology and data to the online lending industry. “While there were definitely some industry and company-specific challenges in the first half of the year, I believe the online lending industry as a whole is wiser and stronger as a result,” he says.

Certainly, 2016 saw a slowdown in the rapid rate of growth of online lenders. The year began with slight upticks in delinquency rates at some of the larger consumer originators. This was followed by the highly publicized Lending Club scandal over questionable lending practices and the ouster of its CEO. Consumers got spooked as share prices of industry bellwethers tumbled and institutional investors such as VCs, private equity firms and hedge funds curbed their enthusiasm. Originations slowed and job cuts at several prominent firms followed.

Despite the turmoil, most players managed to stay afloat, with limited exceptions, and brighter times seemed on the horizon toward the end of 2016. Institutional investors began to dip their toes back into the market with a handful of publicly announced capital-raising ventures. Loan volumes also began to tick up, giving rise to renewed optimism for 2017.

Notably, in the year ahead, market watchers say they anticipate modest growth, a shift in business models, consolidation, possible regulation and additional consumer-focused initiatives, among other things.

MARKETPLACE LENDERS REDEFINING THEMSELVES

Several industry participants expect to see marketplace lenders continue to refocus after a particularly rough 2016. Some had gone into other businesses, geographies and products that they thought would be profitable but didn’t turn out as expected. They got overextended and began getting back to their core in 2016. Others realized, the hard way, that having only one source of funding was a recipe for disaster.

“Business models are going to evolve quite substantially,” says Sam Graziano, chief executive officer and co-founder of Fundation Group, a New York-based company that makes online business loans through banks and other partners.

For instance, he predicts that marketplace lenders will move toward using their balance sheet or some kind of permanent capital to fund their loan originations. “I think that there will be a lot fewer pure play marketplace lenders,” he says.

Indeed, some marketplace lenders are starting to take note that it’s a bad idea to rely on a single source of financing and are shifting course. Some companies have set up 1940-Act funds for an ongoing capital source. Others have considered taking assets on balance sheet or securitizing assets.

“The trend will accelerate in 2017 as platforms and investors realize that it’s absolutely necessary for long-term viability,” says Glenn Goldman, chief executive of Credibly, an online lender that caters to small-and medium-sized businesses and is based in Troy, Michigan and New York.

BJ Lackland, chief executive of Lighter Capital, a Seattle-based alternative lender that provides revenue-based start-up funding for tech companies, believes that more online lenders will start to specialize in 2017. This will allow them to better understand and serve their customers, and it means they won’t have to rely so heavily on speed and volume—a combination that can lead to shady deals. “I don’t think that the big generalist online lenders will go away, just like payday lending is not going to go away. There’s still going to be a need, therefore there will be providers. But I think we’ll see the rise of online lending 2.0,” he says.

Despite the hiccups in 2016, Peter Renton, an avid P2P investor who founded Lend Academy to teach others about the sector, says he is expecting to see steady and predictable growth patterns from the major players in 2017. It won’t be the triple-digit growth of years past, but he predicts investors will set aside their concerns from 2016 and re-enter the market with renewed vigor. “I think 2017 we’ll go back to seeing more sustainable growth,” he says.

THE CONSOLIDATION EQUATION

Ron Suber, president of Prosper Marketplace, a privately held online lender in San Francisco, says victory will go to the platforms that were able to pivot in 2016 and make hard decisions about their businesses.

Prosper, for example, had a challenging year and has now started to refocus on hiring and growth in core areas. This rebound comes after the company said in May that it was trimming about a third of its workforce, and in October it closed down its secondary market for retail investors. Suber says business started to pick up again after a low point in July. “Business has grown in each of the subsequent months, so we are back to focused growth and quality loan production,” he says.

Not long after he said this, Prosper’s CEO, Aaron Vermut, stepped down. His father, Stephan Vermut, also relinquished his executive chairman post, a sign that attempts to recover have come at a cost.

Other platforms, meanwhile, that haven’t made necessary adjustments are likely to find that they don’t have enough equity and debt capital to support themselves, industry watchers say. This could lead to more firms consolidating or going out of business.

The industry has already seen some evidence of trouble brewing. For instance, online marketplace lender Vouch, a three-year-old company, said in June that it was permanently shuttering operations. In October, CircleBack Lending, a marketplace lending platform, disclosed that they were no longer originating loans and would transfer existing loans to another company if they couldn’t promptly find funding. And just before this story went to print, Peerform announced that they had been acquired by Versara Lending, a sign that consolidation in the industry has come.

The industry has already seen some evidence of trouble brewing. For instance, online marketplace lender Vouch, a three-year-old company, said in June that it was permanently shuttering operations. In October, CircleBack Lending, a marketplace lending platform, disclosed that they were no longer originating loans and would transfer existing loans to another company if they couldn’t promptly find funding. And just before this story went to print, Peerform announced that they had been acquired by Versara Lending, a sign that consolidation in the industry has come.

“I think you will see the real start of consolidation in the space in 2017,” says Stephen Sheinbaum, founder of New York-based Bizfi, an online marketplace. While some deals will be able to breathe life into troubled companies, others will merge to produce stronger, more nimble industry players, he says. “With good operations, one plus one should at least equal three because of the benefits of the economies of scale,” he says.

Market participants will also be paying close attention in 2017 to new online lending entrants such as Goldman Sachs’ with its lending platform Marcus. Ullman of Orchard Platform says he also expects to see more partnerships and licensing deals. “For smaller, regional and community banks and credit unions—organizations that tend not to have large IT or development budgets—these kinds of arrangements can make a lot of sense,” he says.

A BLEAKER MCA OUTLOOK

Meanwhile, MCA funders are ripe for a pullback, industry participants say. MCA companies are now a dime a dozen, according to industry veteran Chad Otar, managing partner of Excel Capital Management in New York, who believes new entrants won’t be able to make as much money as they think they will.

Paul A. Rianda, whose Irvine, California-based law firm focuses on MCA companies, likens the situation to the Internet boom and subsequent bust. “There’s a lot of money flying around and fin-tech is the hot thing this time around. Sooner or later it always ends.”

In particular, Rianda is concerned about rising levels of stacking in the industry. According to TransUnion data, stacked loans are four times more likely to be the result of fraudulent activity. Moreover, a 2015 study of fintech lenders found that stacked loans represented $39 million of $497 million in charge-offs.

Although Rianda does not see the situation having far-reaching implications as say the Internet bubble or the mortgage crisis, he does predict a gradual drop off in business among MCA players and a wave of consolidation for these companies.

“I do not believe that the current state of some MCA companies taking stacked positions where there are multiple cash advances on a single merchant is sustainable. Sooner or later the losses will catch up with them,” he says.

Rianda also predicts that the decrease of outside funding to related industries could have a spillover effect on MCA companies, causing some to cut back operations or go out of business. “Some companies have already seen decreased funding in the lending space and subsequent lay off of employees that likely will also occur in the merchant cash advance industry,” he says.

THE REGULATORY QUESTION MARK

One major unknown for the broader funding industry is what regulation will come down the pike and from which entity. The Office of the Comptroller of the Currency that regulates and supervises banks has raised the issue of fintech companies possibly getting a limited purpose charter for non-banks. The OCC also recently announced plans to set up a dedicated “fintech innovation office” early in 2017, with branches in New York, San Francisco and Washington.

There’s also a question of the CFPB’s future role in the alternative funding space. Some industry participants expect the regulator to continue bringing enforcement actions against companies. In September, for instance, it ordered San Francisco-based LendUp to pay $3.63 million for failing to deliver the promised benefits of its loan products. Ullman of Orchard Platform says he expects the agency to continue to play a role in the future of online lending, particularly for lenders targeting sub-prime borrowers.