New California Disclosure Rules Reduce Capital Available to Small Businesses

March 21, 2023In a poll conducted by a leading trade association, since new CA disclosure rules were implemented in December 2022, 40% of respondents were found to be “no longer lending” to prospective borrowers who fall within the regulations’ threshold of less than $500,000. The poll was conducted by The Secured Finance Network (SFNet), an 80-year-old nonprofit with members representing the $4T U.S. secured finance industry. The new law, requiring sweeping financial disclosures, introduced by CA State Senator Steven M. Glazer in 2018, faced four years of strong opposition before being rolled out in December of 2022.

According to the poll, commercial finance companies would rather not lend to small businesses than comply with what they believe are “misguided and un-compliable” requirements. Mark Hafner, president and CEO of Celtic Capital Corporation, based in Calabasas, CA, said, “Unfortunately, we must now shy away from smaller deals (under the $500k threshold) as the disclosure requirements are extremely complicated to figure out and would require getting our attorneys and CPAs involved to ensure compliance. It’s just not worth the costs involved to fund a small deal anymore. The statute is not user friendly and, frankly, not representative of the true costs as there are numerous assumptions that have to be made to calculate the APR based on the state’s requirements. I honestly don’t think it was designed to meet the stated goal of the statute.”

Robert Meyers, president of Republic Business Credit, which does business with many California-based businesses, explained, “While the fines and penalties are clear under the regulations, the state has been unwilling to confirm our compliance or anyone else’s compliance. That fear is what has stopped 40% of our non-banks from doing business in the state, thus reducing access to capital for small- and medium-sized businesses. I expect this number to increase as time goes on. If the goal of this law was to better inform, it is actually doing the opposite as APR just doesn’t apply to our products.”

SFNet reports that its member companies provide “tens of billions” of capital annually in California to small businesses for essential working capital that funds everything from inventory, to work in process to payroll.

“Forty percent of billions is a large number,” said SFNet CEO, Richard D. Gumbrecht. “In attempting to find a one-size-fits-all solution to financial transparency, the State has created a complex set of requirements that misrepresent the actual cost of borrowing. Lenders are saying it’s not worth the cost and risk of complying. If this sample of 50 lenders is indicative of what we can expect, clearly that was not the intent of the legislation. And considering the demise of Silicon Valley Bank, it’s more important than ever that capital is not restricted in California.” The trade association is working with State legislatures to revise the statute. “Other states have found a simpler and more accurate way to protect small borrowers, and given the unintended consequences we are seeing, we are hopeful California will be receptive to these alternative approaches.”

To demonstrate how vital small businesses are to the U.S. economy, and the importance of not curtailing funding, consider these statistics: According to the U.S. Small Business Association (SBA), small businesses of 500 employees or fewer make up 99.9% of all U.S. businesses and 99.7% of firms with paid employees. Of the new jobs created between 1995 and 2020, small businesses accounted for 62%—12.7 million compared to 7.9 million by large enterprises. A 2019 SBA report found that small businesses accounted for 44% of U.S. economic activity.

About Secured Finance Network

Founded in 1944, the Secured Finance Network (formerly Commercial Finance Association) is an international trade association connecting the interests of companies and professionals who deliver and enable secured financing to businesses. With more than 1,000 member organizations throughout the U.S., Europe, Canada and around the world, SFNet brings together the people, data, knowledge, tools and insights that put capital to work. For more information, please visit SFNet.com.

Media Contact:

Michele Ocejo, Director of Communications

Secured Finance Network

mocejo@sfnet.com, 551-999-5283

In The Funding Biz? Here’s What to Know

March 9, 2023Are you in the biz of funding small biz? Listen to these execs tell you how to make it work!

Effective Broker Training

Successful Digital Marketing With Zack Fiddle

Measuring the Impact of Technology on Your Funding Business With Adam Schwartz

Building a Successful Funding Brokerage With Frankie DiAntonio

Commercial Funding Partners promotes Bailey Turner to Senior Vice President of Market Strategies

March 8, 2023 Commercial Funding Partners (CFP) has announced the promotion of Bailey Turner to Senior Vice President of Market Strategies. In this new capacity Turner will be responsible for overseeing marketing strategies and efforts to improve the company’s market positions and achieve desired business goals.

Commercial Funding Partners (CFP) has announced the promotion of Bailey Turner to Senior Vice President of Market Strategies. In this new capacity Turner will be responsible for overseeing marketing strategies and efforts to improve the company’s market positions and achieve desired business goals.

Turner joined CFP in 2017 as Business Development Officer and was quickly promoted to Vice President and subsequently Partner in the firm. During his tenure, Bailey has been a tremendous asset to the growth of the company. “Bailey’s contribution to bottom line growth of CFP has been paramount. We are excited to use his years of experience and excellent leadership skills to continue to expand our sales revenues and innovate our client experience,” said Buddy Zarbock, President of CFP.

Commercial Funding Partners is a national lender that provides businesses with no-hassle asset financing and leasing. CFP’s industry leadership and a wide array of financing products have helped its customers prosper since 1987. Please visit their website at www.com-funding.com

“Aggressive” Funding

March 7, 2023 Sometimes it pays to be aggressive!

Sometimes it pays to be aggressive!

“I think [aggressive funding] is a good phrase, I think in particular in the ISO organization as you’re speaking to the merchant you have to present yourself that you’re going to take an aggressive position to help them,” said Steve Kietz, CEO at Reliant Funding, “to help them get the biggest MCA deal size that you can get them, the best pricing that you can get them, be aggressive in terms of speed to try to get money for that merchant.”

And once that deal is in a broker’s hands, they may turn around and expect their network of funding partnerships to make that happen. Some lenders and funders lean into this style of courtship and market themselves as being similarly aggressive with their approvals.

“The word aggressive, that’s like my favorite word in this industry, because I guess it’s supposed to turn brokers on,” said Amanda Kingsley, Director of Marketing and Development at Merchant Marketplace.

The level of aggressiveness may depend on the attractiveness of the deal itself. According to Joseph Vaknen, Head of Business Development at SuperFastCap, funders will get more aggressive with their offers when there’s a “hot deal” on the table and it will kick off something similar to an auction or a bidding war. That scenario could potentially lead to the best outcome for the merchant just as intended and the broker essentially proves their value.

One’s aggressiveness can also be used to describe an overall risk appetite in general. “If you are considered an aggressive funder in the sense that you are funding bad deals then more likely than not the rate is super high and the term is super short,” said Vaknen. In that case, it’s important that all involved understand what is meant by aggressive.

And on the contrary, plenty of funding providers distance themselves from any such connotations of aggressiveness and are happy to be branded the opposite, conservative in their ways. That too can provide its own attractiveness depending on the circumstances. Aggressiveness, as one is surely aware in the financial services industry, can carry a certain stigma attached to it anyway.

“I think it’s a word that does have a negative connotation, but – you know, the word that we’ll add is caveat emptor buyer beware — as long as the customer knows what he or she is doing, having an aggressive ISO can be a good thing for them,” said Kietz of Reliant.

Filling The Funding Gap for Canadian Borrowers

March 5, 2023 “Generally, capital availability is usually stronger in the U.S., but I would say Canadian businesses are definitely less serviced when it comes to options to be able to access capital,” said Cato Pastoll, Founder and CEO at Loop. “There’s just kind of less services or less products out there for companies so that definitely means that there’s going to be more demand for loan related products.”

“Generally, capital availability is usually stronger in the U.S., but I would say Canadian businesses are definitely less serviced when it comes to options to be able to access capital,” said Cato Pastoll, Founder and CEO at Loop. “There’s just kind of less services or less products out there for companies so that definitely means that there’s going to be more demand for loan related products.”

One of the lingering challenges in Canada is that the big banks tend to hoard the data that would be valuable to fintechs to service more borrowers, hence the recurring call for open banking.

“If you’re a fintech and you don’t have access to that information, you have to figure out a way to access it from the banks that do hold it,” said Tal Schwartz, Senior Product Manager at Nomis Solutions and Writer at Canadian Fintech. What’s happened as a result is that a whole cottage industry has formed to figure out ways to relay data without APIs.

Cato Pastoll’s company, Loop, is among those that have come up with clever solutions to service Canadian customers. For example, Loop can help Canadian-based companies obtain loans in U.S. dollars to help them grow while also offering other services like expense management tools and cross-border payments.

“A lot of businesses have a hard time getting financing from the bank,” Pastoll Said, “so there’s definitely a few players that do provide different products to help companies be able to access growth capital, working capital, and many of them have been around as long as we have for the last five to ten years or so.”

“So, things that can probably improve in Canada are all related to competition, law, and kind of creating a more equal playing ground between banks and fintechs,” said Schwartz. Although those initiatives seem to be trending in the right direction, it’s been a very a slow march forward.

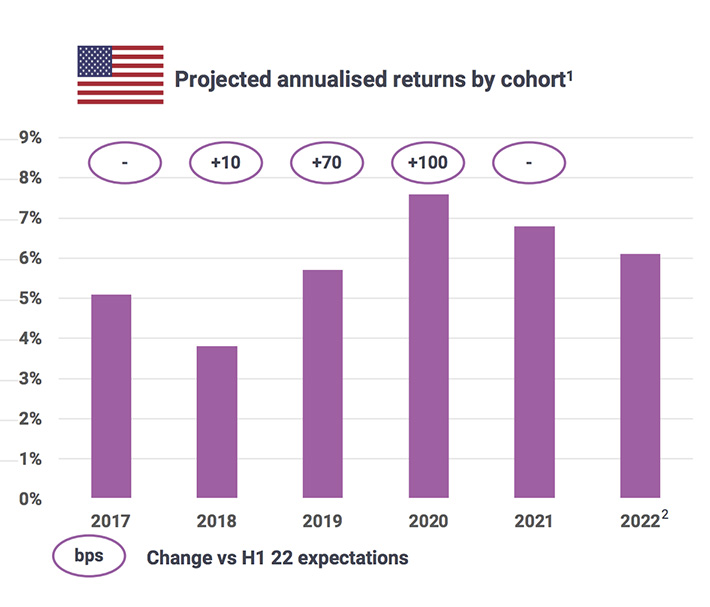

Funding Circle US Originates $393M in 2022

March 2, 2023The American arm of Funding Circle originated $393M in business loans in 2022, according to the company’s latest public financial statements, nearly quadruple the previous year.

The majority of Funding Circle’s loans are currently projecting annualized returns in the vicinity of US inflation levels. A graph of their loans by cohort is below:

Funding Circle US has a fairly diversified base of capital, having worked with eight forward flow funders in 2022, one of which was a credit union.

The UK still remains the overall company’s primary market. It originated £723M in business loans in 2022, not including those part of government support scheme programs.

Square Loans Completes Monster Funding Year

February 26, 2023 Square Loans rose to the top of AltFinanceDaily’s small business loan originations leaderboard last year after announcing $1.16B in originations in Q4. That brought the company, which is a subsidiary of Block (formerly Square), to over $4B funded for the year total, spread out across 461,000 loans.

Square Loans rose to the top of AltFinanceDaily’s small business loan originations leaderboard last year after announcing $1.16B in originations in Q4. That brought the company, which is a subsidiary of Block (formerly Square), to over $4B funded for the year total, spread out across 461,000 loans.

In its annual shareholder letter, Block said that “Square Loans achieved strong revenue and gross profit growth during the fourth quarter of 2022.” Demand for loans has been steady and loss rates have stayed consistently within historical ranges.

Square Loans typically approves merchants for less than 20% of a merchant’s expected annual Square gross payment volume, is repaid by withholding a percentage of credit card sales, and enjoys a borrower base that pays off its loans in less than 9 months on average.

Block’s business is so large and now has so many components that Square Loans did not even come up in Block’s Q4 earnings call. Overall, the company generated $5.7B in revenue in 2022.

The small business loans originations leaderboard contains a lot of blanks. That’s because several public companies have attempted to obscure their business lending figures or non-public ones have opted to not disclose their figures. If you want your company’s figures to be added, email info@debanked.com.

Shopify Capital Seeing “Incredibly Strong Renewals From Previous Borrowers”

February 16, 2023Shopify Capital originated $393.2M in MCAs and business loans in Q4, an increase of 21% YoY, the company revealed. The company also began funding small businesses in Australia last year, bringing the total countries it does business in to four.

“[Shopify] Capital has acted as a lifeline for merchants, especially through the pandemic and this tough macro environment, allowing them to conveniently access capital when they need it most,” said Shopify President Harley Finkelstein. “Capital is now available in four countries, and our machine-learning algorithms to underwrite merchants keeps getting better.”

Finkelstein also noted that the company is “seeing incredibly strong renewals from previous borrowers.”

The graphic below, illustrating the cumulative growth of Shopify Capital’s originations, was shown in the company’s Q4 earnings presentation: