From Sales to Founder: Craig J. Lewis Talks Gig Wage’s $7.5 Million Funding Round

November 27, 2020 Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Lewis made $10 million in payroll tech sales before going on to lead a firm that has seen 30% month-to-month growth this year, during a pandemic no less.

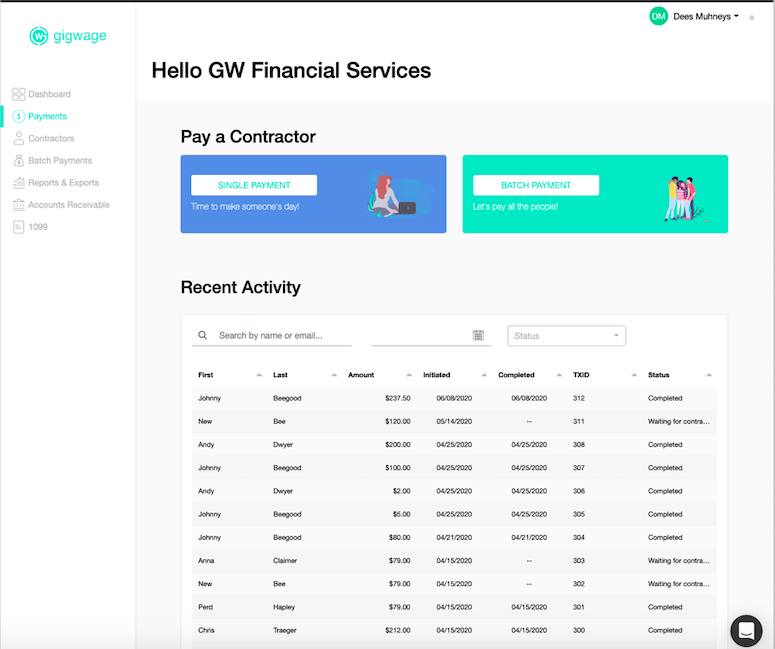

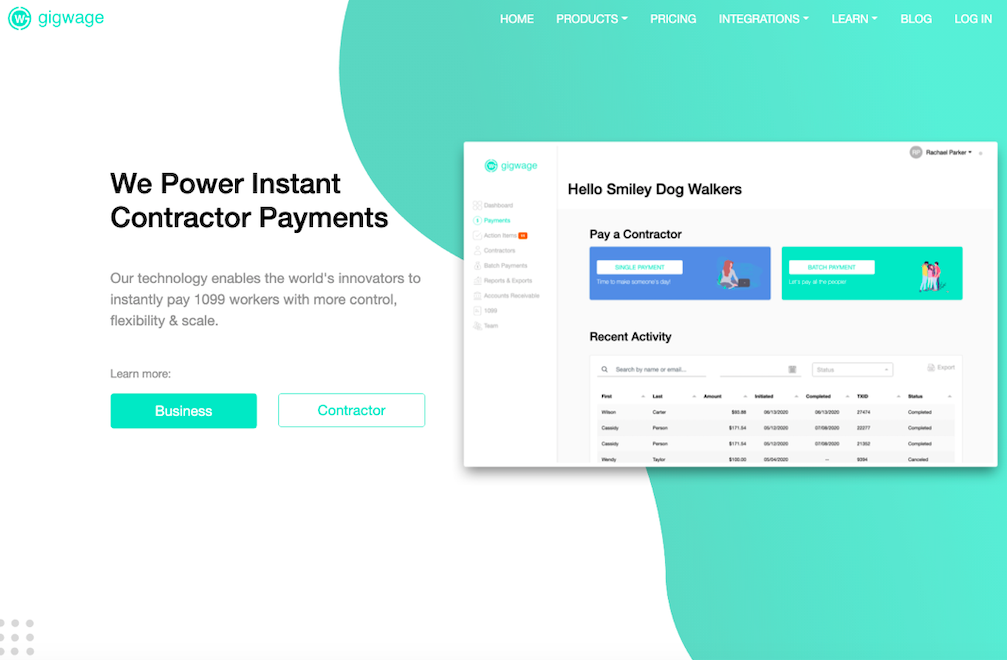

“We help businesses pay independent contractors, but because we’re so tech-centric, it’s evolved beyond just payroll,” Lewis said. “What we ended up building was financial infrastructure for the modern workforce. We help businesses get money from their customers to their contractors as fast and as flexibly as possible.”

The way Gig Wage does this, Lewis said, is by offering an online platform for the hybridization of payroll, payments, and banking from a single login. Businesses can manage their payroll needs for 1099 workers, then shift to payment needs quickly, through direct to debit, all major cards, bank transfers, and accounts receivables.

“One of the only- the only platform in the world actually that has embedded banking into payroll and payments, which is what kind of allows for this speed and flexibility that we offer,” Lewis said. “We’re like B to B to C: We help the businesses with technology and operational excellence, and because independent contractors are separate from the workplace, we provide tools for them.”

Lewis has years of experience in the payroll space- starting as a salesman for ADP small business payroll products back in 2008. Realizing he had a passion for payroll tech and getting customers the best services possible, Lewis went on to learn anything he could about the industry. Selling $10 million in software while moving across the country, Lewis landed in Silicon Valley, where he studied what it took to start a company.

“I was just awed how they thought about technology and products and company building,” Lewis said. “And I vowed to bring that to the payroll industry.”

Lews joined a startup, learned the Silicon Valley way of creating a company through an African American tech acceleration program. In 2014, Lewis founded Gig Wage to do something disruptive in the payroll space.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

“With the maturation of Uber, Lyft, Postmates, Doordash, Grubhub, Upwork, all of these kinds of gig economy freelancer companies, we had great growth going into 2020,” Lewis said. “In Q1, we were set up to raise our series A, and then March happened, and the terms got pulled off the table.”

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

“The gig economy was right there waiting on the workforce to provide opportunities to earn, and we were positioned perfectly to help people compete for that talent and pay people in a modern way,” Lewis said. “The pandemic has been a huge growth accelerant for us, and we think those tailwinds will only continue.”

Those winds of success came during a time of protest. Amplified in the pandemic’s backdrop, the country was waking up to the unequal disenfranchisement black people faced. Only 1% of black founder entrepreneurs ever receive VC funding, and Lewis said he is proud to have raised a significant round, given that unfair stat.

“With so much controversy and negative energy around black people in general,” Lewis said. “I think putting this positive story out there and showing this black excellence, black tech, I think it’s super important, and it’s been something that I’ve embraced. We’ve been able to be a part of putting something extremely powerful and positive into the market.”

America is finally waking up to realize something Lewis said was obvious, that black people matter, even though it can be controversial to say so. He hopes his success can help others but affirms the funding round was no charity drive.

“This is a great opportunity for us to be clear about the fact that like hey, we’ve been working on this, we’ve built a good business and a good technology,” Lewis said. “This is a big business opportunity for our investors and us. It wasn’t charity, right: This isn’t like, oh he’s black, give him some money.”

The successful funding round shows confidence in the Gig Wage platform from Green Dot, which will allow Gig Wage to offer bank accounts and debit services to independent contractors. Green Dot is one of the only fintechs with a national banking license, Lewis said, and Gig Wage is joining the Banking-as-a-Service direction that the fintech industry is headed.

Beyond payroll, Lewis can’t wait to offer other financial products to businesses as the company grows.

“When you think about the gig economy, it’s important that people get paid fast and flexibly: You’ve got to have the cash to be able to do that,” Lewis said. “We see some unique opportunities to get involved in the lending space down the line as well as we continue to build out our technologies.”

Pearl Capital Business Funding LLC Resumes Merchant Cash Advances After Processing $1.75 B in PPP Loans

November 5, 2020JERSEY CITY, N.J. – November 5, 2020 — Pearl Capital Business Funding, LLC, a leading provider of direct financing to small and midsize businesses, today announced that it will resume funding merchant cash advances for U.S. small businesses after suspending funding for a period of time due to the COVID-19 crisis. The move comes after a seven month hiatus during which the company utilized its technology platform to process over $1.75 Billion in SBA Paycheck Protection Program (PPP) Loans.

Pearl Capital provides innovative alternative financial solutions, specializing in the underbanked and subprime business sector. Their financing solutions are available throughout the U.S. to businesses of virtually any industry that are unable to access sufficient traditional financing from banks and non-bank lenders. Pearl’s solutions are not dependent on the business owner’s FICO score and present a compelling solution to underwriting credit even during the current COVID-19 crisis. With the relaunch, Pearl’s ISO Partners can expect lighter stipulation requirements with fewer requested documentation than before and updated pricing. Virtually all business types are eligible for funding from Pearl including high risk industries like auto sales, real estate, home-based businesses, and insurance.

“When the COVID-19 pandemic hit last March, we weren’t sure what our future looked like. With so much uncertainty of the economic climate, like many other funders, we temporarily ceased funding. We pivoted and partnered with Cross River Bank and were able to transition our fully-automated processing and anti-fraud technology to process SBA Paycheck Protection Program (PPP) Loans.” Chief Revenue Officer, Jake Lerner, says, “Using our technology platform, we were able to process over $1.75 Billion in PPP loans for businesses affected by COVID-19.”The Paycheck Protection Program (PPP) was a SBA loan program established under the CARES Act to help small businesses keep workers on their payrolls during the pandemic. The program ended on August 8, 2020 but is likely to resume.

“We’re thrilled to have the ability again to continue to provide financing for companies during an especially difficult time for businesses across the country and give much needed financial support to businesses” CEO, Sol Lax, says, “Pearl did not default on its senior credit line due to its superior underwriting and has added $250 Million in committed financing to expand its activities. If you are a small business and you have survived COVID, you shouldn’t have to shut your doors because you have limited access to capital. We are going to be there for small business both in further iterations of PPP as well as MCA.”

About Pearl Capital

Pearl Capital was founded in 2012 and acquired by private equity firm Capital Z Partners in 2015. Since then, they have become a leader in the fintech industry specializing in short term capital advance solutions for under-banked and credit-challenged businesses, in just about every industry. Over the years, they have provided over 23,000 MCA financings to small businesses across the country, by working with their network of ISOs. Their advanced online application technology platform and machine learning SMB credit score allows them to provide flexible terms and some of the fastest response times in the industry for deals up to one-million dollars. Most recently, Pearl Capital partnered with Cross River Bank to process over $1.75 Billion in Paycheck Protection Program (PPP) loans.

Contact:

Jake Lerner, Chief Revenue Officer

press@pearlcapital.com

+1 347-584-8653

Avant CEO: Colorado Decision Framework for Bank Fintech Partnerships

October 13, 2020 After three years of litigation, in August, the Colorado “true lender” case settled with an agreement between the fintech lenders, bank partners, and the state regulators. Along with lending restrictions above a 36% APR, the fintech lenders will have to maintain a state lending license and comply with other regulatory practices.

After three years of litigation, in August, the Colorado “true lender” case settled with an agreement between the fintech lenders, bank partners, and the state regulators. Along with lending restrictions above a 36% APR, the fintech lenders will have to maintain a state lending license and comply with other regulatory practices.

The decision has been called unfair regulation and a bad precedent for other similar regulatory disputes across the country.

But James Paris, the CEO of Avant, sees the decision as a victory for fintech lenders. Paris said the decision was an excellent framework for fintech/bank partnerships across the nation and a sign that regulators are finally taking the benefits of alternative finance seriously.

“For us, the case also involved being able to continue to provide these good credit products to deserving customers who maybe weren’t being served as well through some of the legacy providers,” Paris said.

Paris called back to the Madden vs. Midland Funding case in the US Court of Appeals Second Circuit decided in 2015. That case called into question if loans made in fintech bank partnerships in the state of New York were valid at the time of origination. Regulators charged that though national banks can create loans higher than state regulations allow, fintech partners buying those loans to take advantage of higher rates were skirting state regulations.

“The ruling was essentially that the loan would not continue to be valid,” Paris said. “Because the individual state in question, which was New York’s local usury law, would apply because it was no longer a national bank that held that loan after it had been sold.”

The decision called into question loans made in the fintech space. Paris said that the Colorado true lender Case was not about whether the banks were even making loans. Instead, fintech lenders were called the true originators and therefore didn’t have a license that allowed them to make loans at higher rates than the state allowed.

Paris said the decision showed confidence that fintech bank partnerships were not exporting rates, and that by limiting lending to under 36%, regulators were protecting bank fintech partnerships and consumers.

“All of the lending Avant does is under 36%, and that’s been the case for years,” Paris said. “In the space where we do play, from 9% to just under 35%, through our partnership with WebBank, we are confident in running a portfolio extremely focused on regulatory compliance.”

Colorado went from not allowing partnerships at all, to working with fintech companies to developing a set of terms that allowed partnerships to function, Paris said. He added that Avant’s products have always been to customers below nonprime credit, from 550 to 680 Fico scores, serviced by up to 36% APRs.

Paris said he does not know about customers outside of this range, or how they are affected by limiting APR to 36%, but he cited a study done by economist Dr. Michael Turner. Turner is the CEO and founder of the Policy and Economic Research Council (PERC), a non-profit research center.

The study compared lending after the Madden case in New York with how customers can be served after the Colorado true lender case. In the credit market Avant serves, Turner found that customers are better off with access to regulated fintech loans, as opposed to not having access at all.

The study looked at the average borrower credit score, APR, and loan size of Avant and WebBank borrowers, and found that if WebBank loans through Avant were prohibited, borrowers would be forced to access other means of credit, through much higher rates.

“Should WebBank loans be prohibited in Colorado, then we can reasonably expect that some non-trivial portion of the WebBank loan borrower population, as well as prospective future borrowers, will be forced to meet their credit needs with higher cost products,” Turner wrote. “This outcome is financially detrimental for this borrower population, most of whom have no access to more affordable mainstream alternatives.”

Given this data, Paris is happy to comply with the regulation. Without the framework Colorado has provided, Paris said borrowers would be worse off. Paris hopes that this decision will precede other state frameworks because what fintech bank partnerships need the most are consistent regulatory practices.

“I’m hopeful that to the extent there are ongoing concerns around bank models across other states, that this type of safe harbor model that Colorado helped develop is something that others could look to as a precedent or a model. Because I think the more that we can have consistency across the relevant jurisdictions, the better.”

CredoLab Lands $7M Funding, Bringing the “Gini” to US, Elsewhere

October 2, 2020

Chief Product Officer Michele Tucci said the platform uses 50,000 data points of mobile phone activity to predict a prospective borrower’s debt capabilities. CredoLab serves the 1.7 billion “credit-invisible” customers across the globe that may have some credit history, but not enough for a score, let alone a prime score.

“We do this in real-time: in less than a second a lender anywhere in the world, receives a credit score from Credolab,” Tucci said. “We don’t know the identity of the user; it’s only known to the bank or the lender, not to Credolab.”

CredoLab anonymously collects thousands of mobile data points, uses that data to create behavioral models, and then derives a credit score. The data can be anything- from the type of apps a user downloads, to the number of calendar events created- even the amount of texts the user sends. Is the user a gambler, a gamer, does the user use a work email during the week, and how many calendar events they schedule- all go into the predictive model.

“Some of these micro behavioral patterns could be the type of files being downloaded. Is it mostly music, or is it PDFs- or the percentage of photos taken in the week prior to the loan application that are selfies,” Tucci said. “So these are all indications that we collect and find a correlation we compare and analyze about 1.3 million micro behavioral patterns.”

Tucci said the CredoLab platform offers unmatched speed and predictability for customers’ future credit habits. He said Credolab helps lenders save money because they can better predict how their borrowers will act. Borrowers benefit by the program: Tucci argued that if lenders can better expect how they will be repaid, they tend to lend more.

The team built the platform for the world’s risk managers, whom Tucci knows constantly worry about the health of their transactions.

“Our CEO and founder Peter Bartek has more than 20 years of experience managing risk,” Tucci said. “So he feels the pain of the CROs out there, and our solution is built to address the very specific needs of chief risk officers.”

To explain the CredoLab platform’s accuracy, Tucci used a data metric called the Gini coefficient, a number between 0 and 1 that identifies to which category a request belongs. In this case, the GINI is used to classify borrowers as creditworthy or unworthy based on their mobile data.

“Zero is like flipping a coin; you have a 50/50 chance of getting the decision right. Basically no predictability,” Tucci said. “A GINI of one is like my wife; she’s always right. You know exactly what outcome to expect every single time.”

CredoLab’s platform has a predictive power of 0.6. Tucci cited World Bank economist David Mckenzie, who found for each decimal increase in GINI, there is a 1% cost savings from a risk point of view.

LendingPoint Partners with eBay to Fund Online Sellers

August 6, 2020 LendingPoint announced this week that it is partnering with the online marketplace eBay to provide funding to sellers on its platform. Titled eBay Seller Capital, the program will offer terms of up to 48 months, with no origination or early payback fees, and which will be capped at $25,000 during its pilot program.

LendingPoint announced this week that it is partnering with the online marketplace eBay to provide funding to sellers on its platform. Titled eBay Seller Capital, the program will offer terms of up to 48 months, with no origination or early payback fees, and which will be capped at $25,000 during its pilot program.

“We’re committed to empowering entrepreneurs to make their dreams a reality, and we are continuing to partner with our sellers to provide them with the tools they need to thrive, eBay’s VP of Global Payments Alyssa Cutright said in a statement. “We’re excited to make flexible financing options available that are integrated with our new payments experience. The program with LendingPoint will enable critical funding opportunities for eBay sellers, especially during this time of economic uncertainty.”

In its early stages now, eBay Seller Capital will only be available for selected sellers, with the plan being for it to be made available to all eligible sellers in the US later this year. Beyond the program, LendingPoint has made clear in its statement that it aims to “expand their offering to provide eBay sellers with more tools to help run their businesses,” however, when asked, CEO and Co-Founder Tom Burnside did not give details of these future plans.

“I don’t want to leave the proverbial cat out of the bag yet with that,” Burnside commented in a call, “but what I will tell you is that I think when we are done eBay will be able to offer best-of-class seller financing.”

Funding Circle US Lays Off 120 Employees

July 9, 2020Funding Circle US laid off 120 employees yesterday, according to a post shared by Ryan Metcalf, Head of U.S. Regulatory Affairs and Social Impact.

Reuters reported that the company will also centralize its technology development in the UK rather than have a separate US team going forward.

The US operation had largely been focusing on PPP lending and SBA 7(a) loans since the shutdowns occurred.

The announcement coincided with its UK business being approved to participate in the Bounce Back Loan Scheme.

Kabbage and Uber Partner for PPP

June 18, 2020 Two months after its first round, Kabbage and Uber have partnered to offer a streamlined PPP application process for the latter’s drivers. In a surprise move, the companies have come together to offer Uber drivers a fast-tracked and automated option to apply for the Payment Protection Program. According to a Kabbage press release, the specialized application will be sped up by prepopulating relevant information, outlining eligibility, and automated decision-making.

Two months after its first round, Kabbage and Uber have partnered to offer a streamlined PPP application process for the latter’s drivers. In a surprise move, the companies have come together to offer Uber drivers a fast-tracked and automated option to apply for the Payment Protection Program. According to a Kabbage press release, the specialized application will be sped up by prepopulating relevant information, outlining eligibility, and automated decision-making.

“They basically will go through a totally separate path that’s purpose-built for Uber drivers,” said Kabbage CEO Rob Frohwein in the statement. “With more than $100 billion left in the PPP, there is a meaningful opportunity for the self-employed to still apply and receive funding. With Uber, we aim to provide hundreds of thousands of more independent contractors access to federal funding.”

With Uber defining its drivers as independent contractors rather than employees, these drivers were initially ineligible for certain unemployment benefits. However the CARES Act expanded these benefits to include independent contractors from various industries.

This is not Uber’s first foray into providing some sort of assistance for its drivers. Following the signing of the CARES Act in March, the ride-hailing company released a detailed guide for its drivers explaining how to apply for these benefits. As well as this, in France the company has offered drivers emergency grants during the pandemic as well as a stipend to cover sterilizing and safety products.

For Kabbage, this marks a step away from the dark days of late March which saw the company close its offices in Bangalore, India; cut executives’ pay; and furlough an unspecified but “significant” amount of its previously 500-person United States staff, according to a company memo.

The PPP program, which ran out of money within two weeks of its first round, had more than $130 billion left to give to business owners by June 9, just three weeks before the SBA is scheduled to close the application process on June 30.

CFG Merchant Solutions Enhances Partnership with Arena Investors and its Affiliates to Serve SMEs

May 29, 2020NEW YORK, New York., May 29, 2020 — CFG Merchant Solutions (“CFGMS”), a leading financier of small and medium-sized enterprises (“SMEs”), announced today that the company is building upon its partnership with Arena Investors, LP (“Arena”), in conjunction with Ceteris Portfolio Services (“Ceteris), an Arena servicing affiliate, in servicing and providing liquidity to Platinum Rapid Funding’s (“PRF”) merchant portfolio. CFGMS has been a leading capital provider to SMEs and an originator of advances to growing merchants, providing in excess of $400 million merchant cash advances since 2015. Arena has been CFGMS’s primary capital partner since 2016.

CFGMS and Arena are determined to prioritize the needs of PRF’s existing customers in the wake of the COVID-19 crises and its resulting impact on small businesses across the country.

“Arena is pleased to continue its partnership with CFGMS and its senior management team consisting of CEO, Andrew Coon, Chief Legal Officer and General Counsel, Robert Martini, and President, William Gallagher. Together, we remain deeply committed to serving the needs of PRF’s existing customers, particularly for ongoing financing and liquidity needs in an environment when even much larger businesses struggle to attract capital,” said Victor Dupont, who leads Arena’s investments in the financing of the SME sector. “We welcome further involvement with PRF’s customers and their affiliated ISOs and are committed to working collaboratively with all throughout the COVID-19 crises and beyond”.

“Arena and its affiliates have built a reputation as a group that combines uniquely flexible capital with broad-based expertise in servicing, resolutions, and SME finance,” said Coon. “So, while we excel at sourcing, originations, and underwriting, we felt that they brought a critical level of IP and know-how that is uniquely suited to benefit all parties in today’s environment. Combining forces to offer a broader set of servicing solutions to the MCA market segment made complete sense.”

Jonathan Pike, CEO of Ceteris, added: “Ceteris is excited to work with CFGMS and Arena by offering best-in-class servicing strategies and assisting merchants in a difficult economic environment.”

The Small Business Association (“SBA”) estimates that traditional banks still reject approximately 90 percent of SME loan applications. Since 2015, CFGMS has emerged as a proven platform that leverages sales partner relationships, analytics, and proprietary underwriting to provide SMEs with a straightforward and streamlined access to critical funding. The company addresses the fundamental capital needs of SME owners across a broad credit spectrum and through every stage of a business’s life cycle.

SMEs across a wide variety of industries that include restaurants, retail stores, salons, spas, dry cleaners, auto body shops, and professional offices. All of these businesses, and more, rely on CFGMS to secure the necessary capital they need to grow.

For questions or funding solutions, please contact:

– William Gallagher

– (646) 880-3817

– WGallagher@CFGMS.com

– Ryan Banda

– (856) 545-8322

– rbanda@ceterisassetsolutions.com

About CFGMS

Headquartered in New York, NY, CFGMS specializes in providing financing to support the growth and development of underserved small-to-medium sized businesses that lack access to traditional bank funding. Founded in 2010, CFGMS’s affiliated company, CapFlow Funding Group, provides factoring, purchase order finance, and asset-based lending solutions. CFGMS and CapFlow have together provided over $1 billion in liquidity solutions to their SME clients. For more information please visit www.cfgmerchantsolutions.com

About Arena Investors, LP

Arena Investors is a privately held, SEC-registered, global alternative investment firm which combines mandate flexibility, proprietary sourcing and systems-plus-servicing to enable solutions for those seeking capital. The firm was founded in 2015 and is headquartered in NewYork with additional offices in Jacksonville, London, and San Francisco. For more information, please visit www.arenaco.com.

About Ceteris Portfolio Services

Ceteris is a nationally licensed servicing company providing debt recovery solutions and other related services for consumers and commercial businesses across a broad range of financial assets. Ceteris provides first- and third-party revenue cycle management, business process outsourcing and portfolio backup servicing to heavily regulated, high volume industries including banking, automotive finance, credit card, equipment leasing, medical, telecommunications, utilities, retail and other industries. For more information please visit www.ceterisholdco.com.