Funding E-Commerce Businesses Helped This Startup Get Acquired Right After They Launched

June 23, 2021 Less than eight months after Yardline announced their launch in the e-commerce financing space, they were acquired by Thrasio. The blazing fast progression from launching to selling the company suggests that Yardline’s niche presents a unique opportunity.

Less than eight months after Yardline announced their launch in the e-commerce financing space, they were acquired by Thrasio. The blazing fast progression from launching to selling the company suggests that Yardline’s niche presents a unique opportunity.

“There are many companies out there that look at e-commerce businesses in the space and say, ‘there’s no barrier for entry to operate in e-commerce, they’re all drop shippers, it’s a hobby, they have no skin in the game,'” said Seth Broman, Chief Revenue Officer of Yardline. “What Yardline does is really unique: One, we obviously have a lot more information and understanding of how they operate their business, and we can really break down on a deal by deal basis, what their margins look like, to get them a more customized offering that meets their needs.”

Yardline will fund Amazon sellers, for example.

Broman said that while most MCA funders know how to look at a merchant’s fixed costs like rent, payroll, taxes, and inventory to provide funding based on a gross revenue, those same funders don’t have a risk tolerance for e-commerce.

Yardline pulls data from digital marketplaces like Amazon and online storefront platforms like Shopify to make better credit decisions, Broman said, and this was a banner year for digital shopping.

“During COVID, you were seeing such an increase of demand for e-commerce goods; Amazon, Shopify, if you look at their stock price over the last 15 months, it’s incredible,” he said. “And the reason being retails closed, everybody’s shopping from home, and the demand for all my goods is through the roof.”

Before everyone was stuck inside, e-commerce already made up 20% of consumer commerce, Broman estimated. Then everything was online-only, and demand became nearly unlimited, he said. Amazon’s third-party sellers transact 60% of all products sold on the site, and Thrasio is one of the largest consolidators of those sellers in the world, Broman said.

Now, Yardline will have access to Thrasio’s international seller network.

Now, Yardline will have access to Thrasio’s international seller network.

“We’re confident in saying that untapped ecosystem can be very profitable for ISOs if they were to start focusing on e-commerce businesses,” Broman said. “There’s less demand for it, less competition, and now they have a home for where they can get these deals done.”

Broman said after the pandemic, typical brick and mortar stores were hit hard and required PPP to keep the doors open while e-commerce flourished.

“It’s not a matter if shopping online is the future; shopping online is the present. People will continue to shop at brick and mortar, people want to eat out, just look at New York City,” Broman said. “If you look at what Amazon offers, what Walmart’s doing, what Target’s doing, what these online marketplaces are doing to make commerce quicker and easier, there’s no doubt that it’s going to continue to grow.”

Thrasio Acquires Yardline to Offer E-Commerce Funding

June 16, 2021 Amazon merchant conglomerate Thrasio bought Yardline to incorporate e-commerce finance into the product offering. Thrasio has been active with Yardline since the firm’s initial backing of the company, and is now making Yardline a wholly owned subsidiary.

Amazon merchant conglomerate Thrasio bought Yardline to incorporate e-commerce finance into the product offering. Thrasio has been active with Yardline since the firm’s initial backing of the company, and is now making Yardline a wholly owned subsidiary.

Yardline Chief Revenue Officer Seth Broman said that historically, e-commerce has been risky with no barrier to entry like traditional brick and mortar shops. Broman added that online stores used to be for supplements, but through Amazon’s third-party marketplace and Shopify’s help, scaling a quality business has become possible.

“Through COVID, the script was flipped,” Broman wrote in a statement. “E-commerce businesses became less risky, and brick-and-mortar businesses suffered the most. It’s also a much smaller universe and harder to target than a brick-and-mortar business.”

Thrasio boasts it is the largest acquirer of Amazon brands globally, and co-founder and co-CEO Carlos Cashman said 40% of brands they approach end up selling. Now, they can help scale those brands.

“Yardline will be an asset in creating more opportunities for these entrepreneurs and offering more sophisticated avenues for growth,” Cashman said in a statement. “They’ve been doing something different in the space—their strategic approach to providing embedded capital across e-commerce marketplaces is unique—and we’re eager to have their technology and proficiency on our team.”

Tomo Matsuo, president of Yardline, will be joining Thrasio’s senior leadership team. “It’s conceivable that every eCommerce-related platform will have FinTech capabilities in the future,” he said in a statement. “And our acquisition by Thrasio demonstrates that.”

Funding Circle US Originated $800M in 2020, More than 90% of Borrowers Were Making Payments

March 26, 2021 Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle’s US loans generate low annual returns, its highest being a projected return of 4.1% to 4.9% for its 2016 cohort. Its 2020 cohort is projected to generate an annual return of between 1 – 3%.

Overall, Funding Circle reported a total net loss of £108.1M (approx $150M US) on just £103.7M in revenue, a massive loss that stemmed entirely from the first half of the year, attributed mostly to a write-down in “fair value.”

Funding Circle’s primary market is the UK. When comparing the market with the US, the company said that the US is in an earlier stage of development even though the market is 5x larger.

Over Half of Small Businesses Had Unmet Funding Needs

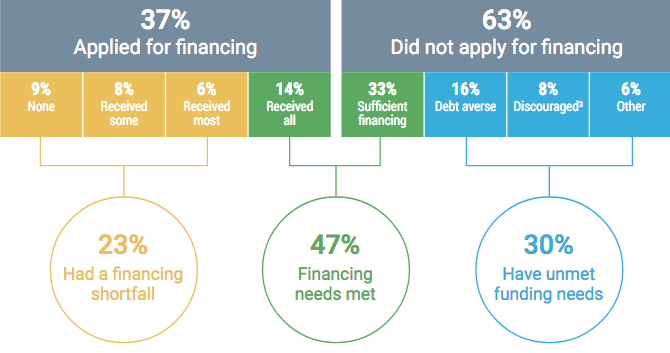

February 8, 2021The Federal Reserve’s analysis of overall funding efforts for all small businesses demonstrates a market of unmet financial needs. In 2020, a total of 47% of firms met their funding needs, while the other half (53%) still needed capital.

23% of firms saw a “financing shortfall.” They were partially approved but still needed more funds. The other 30% have unmet funding needs because they never applied according to the survey- they’re scared of debt, risk-averse, or don’t meet requirements.

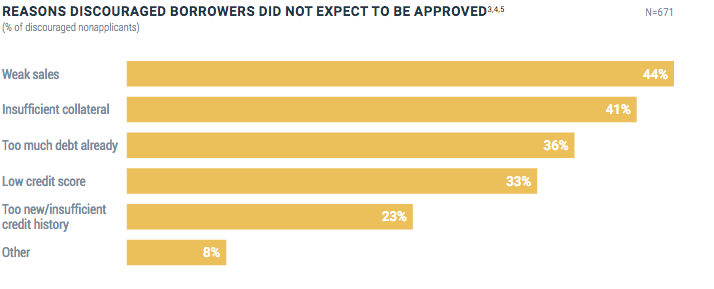

Those that did not apply for funds would have if they were not discouraged by weak sales (44%), insufficient collateral (41%), low credit (33%), and too much debt already (36%).

83% of companies used a bank or small bank as their primary financial service provider, while only 11% said an online lender or fintech was their primary.

Meanwhile, in the funding world, MCAs were only sought by 8% of all funding applicants last year, compared to 89% of firms applying for a loan or line of credit.

Most firms that went for an MCA went with a bank. 85% percent of firms that applied for a loan, credit, or cash advance used a large or small bank. In contrast, only 20% of firms applied to an online lender, falling from 33% since last year.

42% of firms that worked with online lenders or fintech companies were dissatisfied with support during the pandemic. Comparatively, firms that did receive some funding from an online lender were far happier: only 18% were dissatisfied.

Newest Round of PPP Funding Faces Some New Technical Issues

January 26, 2021New technical issues are plaguing the latest round of PPP funding, according to Rob Nichols, the President and CEO of the American Bankers Association. On Monday, Nichols wrote to the acting heads of the SBA and Treasury addressing them.

Though thousands of businesses are awaiting forgiveness, the SBA’s online portal is not allowing a second loan to be processed unless pending first-round forgiveness applications are marked as complete. This runs contrary to the official SBA rules that state a borrower can apply if they can prove they spent their first loan correctly by the time they get a second.

“We urge SBA to fix this technical error and permit a lender to upload a borrower’s second draw PPP loan application irrespective of the status of the borrower’s First Draw Loan forgiveness application,” Nichols wrote. “More broadly, lenders are receiving a high number of incorrect error messages when the lender attempts to submit PPP loan applications through the portal.”

Part of those errors come from confusion Nichols writes, between previous guidance handed out by the SBA and current stipulations. Funders are unclear as to why a $30,000 per employee loan cap exists or why some borrowers found that the documentation they prepared to prove a 25% reduction of revenue met requirements two weeks ago but don’t meet the criteria recently, Nichols wrote.

Lendio Starts Funding Engines, PPP is On The Way

December 30, 2020 President Trump officially signed the economic relief package Sunday night. While the House, President, and Senate can’t agree on the checks individual Americans will get from Uncle Sam, $284 billion for PPP is on the way.

President Trump officially signed the economic relief package Sunday night. While the House, President, and Senate can’t agree on the checks individual Americans will get from Uncle Sam, $284 billion for PPP is on the way.

In preparation, Lendio, an online loan marketplace that facilitated $8 billion in PPP funds over the summer, has already opened the application floodgates. But when is the bill landing?

“The SBA has ten days from the time it was signed into law, January sixth, when they have to give guidance,” Lendio CEO Brock Blake said. “Then, they have some time after that they’ll open it up, my guess is that it will likely go live somewhere between the 10th to 15th.”

Firms, start your funding engines; the money is coming in about two weeks. And Blake said that with the demand for capital this high—the funds would go quick.

“My guess is that it will be two to three weeks, maybe a little longer,” Blake said. “One of the reasons it will last a little bit longer is because they reduced the loan maximum size from ten million to two million. As a result, two to three weeks or more like, you know, three or four.”

Lawmakers initiated limits to the high end this time around to halt concerns that “small business” bailout money was going to larger sized firms. That isn’t the only change for what some say could be the final round of government stimulus.

“I like what they’ve done this time around, addressing some of the key issues, first of which allowing borrowers to have a second turn on PPP loans,” Blake said. “This pandemic has lasted longer than anyone expected, and there’s a lot of restrictions on these business owners.”

The first time around, the Fed handed out forgivable funds based on two and a half months of payroll, and that went real quick, Blake said. For a firm to meet the criteria for a second loan, they have to prove they have a 25% reduction in revenue from 2019 to 2020.

Blake said he was excited that the new aid is granting industries especially hard hit, like restaurants and hotels, to get larger loans “three and a half time instead of two and a half times.” Blake’s favorite part of the new program is incentivizing lenders to serve genuine smaller businesses, where last time they were not.

“Last time, so many of the smallest small businesses were at a disadvantage because we all know lenders prioritize the largest loan sizes first,” Blake said. “They left the smallest of small business out.”

Lendio and fintech lenders focused on this underserved market of small businesses last time, Blake said. After advocating on behalf of small borrowers, Blake said there are incentives for lenders to give to the underserved and actually make money.

“Thankfully, in this new PPP program, they created a new incentive package for loans smaller than $50,000,” Blake said. “That makes these smaller loans a priority, instead of put toward the back of the list.”

Immigrating From Cuba With “Nothing in my pockets,” to a CEO Funding $12 Million a Month

December 15, 2020 “Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

“Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

Ebanks started what would become Spartan Capital shortly after seeing an ad calling for startup investors in an industry Ebanks had never heard of, called Merchant Cash Advance.

It was around 2016. Ebanks was up late in the NYU university library, putting himself through an MBA while working as a reactor operator at the Indian Point nuclear power plant in Westchester.

Despite the job security Ebanks enjoyed, he said he wasn’t happy with his career, wasn’t getting the satisfaction he wanted. He had already made it a long way— starting before the millennium as a Cuban immigrant, immigrating to the Dominican Republic in 1998 and then Florida in 2002 with empty pockets. Shortly after arriving, Ebanks enlisted.

“I spent some time in the army; I wanted to put in some time,” Ebanks said. “I said: ‘I’m a new immigrant, what’s the best thing that I could do to reward these opportunities?’ To serve in the army, give the country a couple years, and payback in advance for this opportunity that I knew I was going to have.”

Ebanks said he learned early on to take every opportunity seriously. He served for two years and then became an engineer and contractor for the army, working on the Patriot Missile defense system. He went through college at NJIT, graduating in 2009, and following in his father’s footsteps to become an electrical engineer.

After working with South Jerseys PSE&G, Ebanks took the opportunity to work full time shifts at the the nuclear power plant, and by 2016 he was pursuing an MBA and looking for ways to grow what he called “my empire.” Used to investing in small businesses already, discovering MCA fit right within his world.

“I’ve always been active, throughout my professional career I had businesses in real estate, I owned several businesses such as laundromats, a lot of retail cell phone stores and things like that,” Ebanks said. “So at one or two am in the morning, I’m working on how to build my empire. I was on Craigslist looking for opportunities, seeing what’s out there, and somebody wanted an investment, to partner up and start a company in a new industry.”

He took a meeting and learned a ton. Although he did not end up going into business with that person, he was hooked on the concept.

“I looked at that ad, and $10,000 later, we had a company,” Ebanks said.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

“I did some research, opened an office in New Jersey, secured a manager to run the operation, and we started brokering deals and learning about syndication.”

He worked with SFS Capital, now called Kapitus. He fell in love with the immediate gratification feedback of making deals, seeing returns on account receivables, and watching renewals come in. The business grew, but things were not always a straight climb to success.

“There was a point where things were not going well and I had to start a new company, find new parters and investors with a funding direct-only focus, and moved into my basement- my wife was unhappy with that. I started hiring people, processors, underwriters, and ISO managers in my basement,” Ebanks said. “At one point, she said, ‘Okay, this is enough. Ten strangers are coming into my house every day, you’ve got to get an office,’ so we secured an office in New York. And that’s when things took off in 2017.”

At that point, Ebanks had shifted his business model from securing deals to funding them all his own, using capital he raised. Ebanks said that being a broker partnered with Kapitus was great, but he wanted to grow and run his business entirely. The best way to do that was through ISO management, Ebanks said. Ebanks let the direct sales team phase out and he hired ISO managers, learning the ISO business as he went.

“So fast forward now: We have over five ISO managers, and we’re funding about $12 million a month,” Ebanks said. “It’s been a phenomenal journey and the most rewarding thing I’ve ever done in my life; I’m not shy to share how exciting every day is to me, and how other than my family and my kids and God, this is the most important thing my life.”

For brokers looking to get started in the industry, Ebanks has this advice to share: Don’t settle.

“Don’t settle, look for growth, and invest your money,” Ebanks said. “I always invested everything I could, 95%, every penny on the business. It matters especially at the beginning, the more you invest, don’t let it sit.”

That investment should go toward your business, your staff, and hiring. Ebanks said the more you invest, the bigger the bag, the more your firm would grow, and your employees will grow with you. Helping employees will mean they will eventually leave, but in Ebanks’ experience treating employees right creates partners.

“Some of them now are partners, and the employee-employer relationship is always more partnership,” Ebanks said. “Some of them own their own companies now, and we help each other out. If they have a big deal, they say: ‘Frank do you want to take $50,000 out of this deal?’ I say yea I trust you. I’ve known you for years.”

Now that he’s on track to grow with recurring customers, seeing some merchants come back to renew twenty times since 2016, Ebanks sees a possible bright future for Spartan Capital: becoming a chartered online bank.

“It is an alternative lending space but to offer the best products to people,” Ebanks said. “I think at the end of the day, and we need all the resources we can get, the next chapter is to apply and secure an online bank charter, it’s the future of the fintech industry.

“Why do people like doing business with us versus a bank? Some of them can do business with banks, but they choose to use us because they have direct access to us after 6 pm, they could call us Saturday, they can call us on a Sunday,” Ebanks said. “A great relationship that they can never get from a bank. I want to bring what we do in MCA to the banking industry to serve people that want banking products, but I want to give them that MCA experience.”

Aspiria Co-Founder On Successful Funding in Mexican SME Space: Still Lots of Room to Grow

December 5, 2020 After 38 years, Guillermo Hernandez has seen the boom and busts of the Mexican financial markets, weathering seven recessions in all, he said. But until 2020, he had never led a company through a pandemic.

After 38 years, Guillermo Hernandez has seen the boom and busts of the Mexican financial markets, weathering seven recessions in all, he said. But until 2020, he had never led a company through a pandemic.

Aspria, Hernandez’s online lending firm, had planned on completing a Series A from international investor Oikocredit, but the deal went into the icebox as the cases came.

“In the beginning of the year, things were doing very well in Mexico, the whole economy was booming,” Hernandez said. “Out of nowhere, we got hit by the pandemic. And the transaction that we were supposed to be closing in March 2020, our investor said, ‘you guys are fantastic, but there are too many unknowns.'”

But due to Aspiria’s resilience and the fact that they went into 2020 with a rock-solid business, Hernandez said Oikocredit decided to complete the investment deal. Aspiria was growing and profitable, and though it was unclear if the markets were going to fall apart, Hernandez said he and his team put the nose to the grindstone and worked through it.

Oikocredit is a worldwide cooperative that provides loans and investments to promote financial inclusion while empowering people by improving livelihoods. That vision is what Aspiria aims to accomplish as an SME lender, Hernandez said, helping businesses access funds to grow.

The Mexican financial space has ample room for growth, and Hernandez said Aspiria is one of the first alternative business lending firms to capture the market.

Hernandez said the banking world in Mexico is twenty years or more behind the US, and he founded Aspiria to bring some change to the financing space.

Hernandez said the banking world in Mexico is twenty years or more behind the US, and he founded Aspiria to bring some change to the financing space.

“The whole financial services industry, I mean it’s light-years behind the US,” Hernandez said. “I saw that the way that people would do the underwriting, the way that people provided financing for small businesses was just so outdated; it was more of an old school market here. I decided there was this huge opportunity for the market.”

For example, Mexico has a third of the US population, but only 30 banks to the 7,000-10,000 the US has. That population is also a younger demographic than up north. In Mexico, the average age is 27 (It’s 38 in the US); Hernandez said: the Average Mexican is trying to establish themselves and reach the middle class, young, educated, and ready to start a business.

Hernandez has been working in finance all his life, starting in Mexico as a banker and consultant for new financial companies before leaving to get his MBA on an HSBC scholarship in Manchester, England. He worked for a time in financial services there before joining a payment startup in the US, where he found his love of startup tech culture.

Hernandez has been working in finance all his life, starting in Mexico as a banker and consultant for new financial companies before leaving to get his MBA on an HSBC scholarship in Manchester, England. He worked for a time in financial services there before joining a payment startup in the US, where he found his love of startup tech culture.

“It was my first exposure to technology, and I was completely amazed. I fell in love with it,” Hernandez said. “At that moment, I was actually thinking about changing careers. I was completely fed up with financial services because it’s boring sometimes. I thought it was not sexy anymore.”

Co-founding Aspiria, Hernandez went on to become the major funder in the space. He said there is so much demand for capital in a standard year that his firm can see 100% year-over-year growth. Even in a pandemic, his firm received a confident investment that will go directly toward building the shop, scaling up funding, hiring, and aiming toward a firm that will one day put it on par with the rest of North America’s leading alternative finance firms.